Homework Answers

Add Answer to:

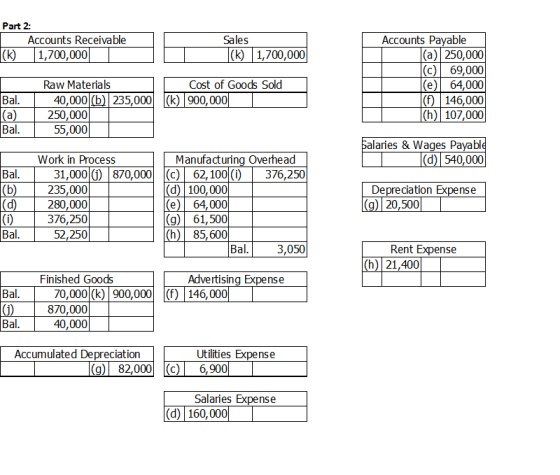

cant get number # 2 to come out right and number 4a and #5.

please help...thank...

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is...

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is a wall company that manufactures specially heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours predetermined overhead rate was based on a cost formula that estimated $350.000 of manufacturing overhead for an estimated location base of 1,000 direct labor-hours. The following transactions took place...

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is a wall company that manufactures specially heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours predetermined overhead rate was based on a cost formula that estimated $350.000 of manufacturing overhead for an estimated location base of 1,000 direct labor-hours. The following transactions took place...

4a 4b and 5 not answered... thank you signment Print View Page 1 Award: 5.00 points...

4a

4b and 5 not answered... thank you

signment Print View Page 1 Award: 5.00 points Froya Faber A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours its predeterm Overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of...

4a

4b and 5 not answered... thank you

signment Print View Page 1 Award: 5.00 points Froya Faber A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours its predeterm Overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $357,000 of manufacturing overhead for an estimated allocation base of 1,020 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Managerial Accounting Chapter 3 Homework Question 2

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $351,500 of manufacturing overhead for an estimated allocation base of 950 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account, $215,000.Raw...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen,...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following...

The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the...

The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $342,000 of manufacturing overhead for an estimated allocation base of 950 direct labor-hours. The following transactions took place during the year: 1. Raw materials purchased on account, $210,000. 2. Raw materials used in production (all direct materials), $195,000. 3. Utility bills incurred on account, $61,000 (95% related to...

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is a wall company that manufactures specially heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours predetermined overhead rate was based on a cost formula that estimated $350.000 of manufacturing overhead for an estimated location base of 1,000 direct labor-hours. The following transactions took place...

nment Print View Page 1 of Award: 5.00 points Froya Fabrikker AS of Bergen, Norwey is a wall company that manufactures specially heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours predetermined overhead rate was based on a cost formula that estimated $350.000 of manufacturing overhead for an estimated location base of 1,000 direct labor-hours. The following transactions took place...

4a

4b and 5 not answered... thank you

signment Print View Page 1 Award: 5.00 points Froya Faber A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours its predeterm Overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of...

4a

4b and 5 not answered... thank you

signment Print View Page 1 Award: 5.00 points Froya Faber A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours its predeterm Overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Most questions answered within 3 hours.

-

Question Three

Suppose you as project manager are using the Waterfall

development methodology on a large...

asked 39 minutes ago -

Which statement is not true about welfare in Canada?

A.Benefits typically vary based on one's ability...

asked 1 hour ago -

Please help me with FLOWCHART and UML diagram for class,

thank you!

#include <iostream>

#include <fstream>...

asked 1 hour ago -

3. Describe the “logic circuit” of the Lac operon. Which

proteins are bound or not to...

asked 1 hour ago -

Ayesha’s adjusted gross income is $60,000 in 2019. She donated a

piece of artwork with a...

asked 2 hours ago -

For Dijkstra’s shortest path algorithm:

a. Give the Big-O time for Dijkstra’s shortest path algorithm

and...

asked 2 hours ago -

Phosphorus violates the 'octet rule' in biological molecules,

forming more covalent bonds than expected based on...

asked 2 hours ago -

A 1.3 eV electron has a 10-4 probability of tunneling

through a 2.4 eV potential barrier....

asked 2 hours ago -

What is the one ingredient that is common to being successful

with all stakeholders?

profit

trust...

asked 2 hours ago -

Write an assembly language 32 bit program that reads in lines of

text by a .txt...

asked 2 hours ago -

what is the density ( in g/L) of hydrogen gas at 29 degrees C and a...

asked 2 hours ago -

5-6. You are considering three investment alternatives for some

spare cash: Old Reliable Corporation stock (A1),...

asked 2 hours ago