Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $357,000 of manufacturing overhead for an estimated allocation base of 1,020 direct labor-hours. The following transactions took place during the year:

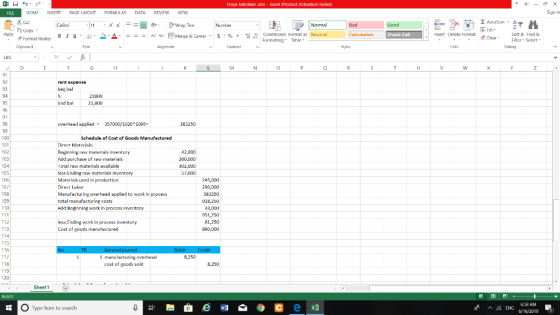

- Raw materials purchased on account, $260,000.

- Raw materials used in production (all direct materials), $245,000.

- Utility bills incurred on account, $71,000 (80% related to factory operations, and the remainder related to selling and administrative activities).

- Accrued salary and wage costs:

| Direct labor (1,095 hours) | $ | 290,000 |

| Indirect labor | $ | 102,000 |

| Selling and administrative salaries | $ |

170,000 |

- Maintenance costs incurred on account in the factory, $66,000

- Advertising costs incurred on account, $148,000.

- Depreciation was recorded for the year, $84,000 (75% related to factory equipment, and the remainder related to selling and administrative equipment).

- Rental cost incurred on account, $109,000 (80% related to factory facilities, and the remainder related to selling and administrative facilities).

- Manufacturing overhead cost was applied to jobs, $ ? .

- Cost of goods manufactured for the year, $890,000.

- Sales for the year (all on account) totaled $1,800,000. These goods cost $920,000 according to their job cost sheets.

The balances in the inventory accounts at the beginning of the year were:

| Raw Materials | $ | 42,000 |

| Work in Process | $ | 33,000 |

| Finished Goods | $ | 72,000 |

Required:

1. Prepare journal entries to record the preceding transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the beginning inventory balances above.) Determine the ending balances in the inventory accounts and in the Manufacturing Overhead account.

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Journal Entry Worksheet

-

1

The raw materials were purchased for use in production, $260,000 on account.

-

2

The raw materials used in production (all direct materials), $245,000.

-

3

The utility bills were incurred, $71,000 (80% related to factory operations, and the remainder related to selling and administrative activities).

-

4

The salary and wage costs incurred were $290,000 (Direct labor), $102,000 (Indirect labor), $170,000 (Selling and administrative salaries).

-

5

The maintenance costs were incurred in the factory, $66,000.

-

6

The advertising costs were incurred, $148,000.

-

7

The depreciation was recorded for the year, $84,000 (75% related to factory equipment, and the remainder related to selling and administrative equipment).

-

8

The entry for rental cost incurred on account, $109,000 (80% related to factory facilities, and the remainder related to selling and administrative facilities).

-

9

The entry for manufacturing overhead cost applied to jobs.

-

10

The cost of goods manufactured for the year, $890,000.

-

11

The sales for the year (all on account) totaled $1,800,000.

-

12

The goods cost $920,000 according to their job cost sheets.

Homework Answers

Add Answer to:

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $357,000 of manufacturing overhead for an estimated allocation base of 1,020 direct labor-hours. The following transactions took place during the year. a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $357,000 of manufacturing overhead for an estimated allocation base of 1,020 direct labor-hours. The following transactions took place during the year. a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $380,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $388,800 of manufacturing overhead for an estimated allocation base of 810 direct labor-hours. The following transactions took place during the year. a. Raw materials purchased on...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $388,800 of manufacturing overhead for an estimated allocation base of 810 direct labor-hours. The following transactions took place during the year. a. Raw materials purchased on...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $373,700 of manufacturing overhead for an estimated allocation base of 1,010 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $357,000 of manufacturing overhead for an estimated allocation base of 1,020 direct labor-hours. The following transactions took place during the year. a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $357,000 of manufacturing overhead for an estimated allocation base of 1,020 direct labor-hours. The following transactions took place during the year. a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $388,800 of manufacturing overhead for an estimated allocation base of 810 direct labor-hours. The following transactions took place during the year. a. Raw materials purchased on...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $388,800 of manufacturing overhead for an estimated allocation base of 810 direct labor-hours. The following transactions took place during the year. a. Raw materials purchased on...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Most questions answered within 3 hours.

-

Calculate the following: ***SHOW ALL WORK!!!! Or

NO CREDIT*** Circle your answers. 8pts

each

In the...

asked 57 minutes ago -

Bank Z is currently advertising interest rates on its checking

account. They claim to pay an...

asked 21 minutes ago -

List two ways of transformation on the response variable that

can be used to deal with...

asked 1 hour ago -

If a 2000 ohm resistor has a -3.90 mA current going through it.

What is the...

asked 1 hour ago -

Please comment on the sentences.

Some types of jobs require more training than others. Some

companies...

asked 2 hours ago -

The )G01 for the hydrolysis of phosphorarginine

reaction depicted below is –32 kJ mol-1.

Phosphoarginine ...

asked 3 hours ago -

Cross a heterozygous blue-eyed goat with a homozygous brown-eyed

goat. Be sure to indicate which kids...

asked 3 hours ago -

Use the following information to answer the next two

questions.

Please refer to question 9-90. A...

asked 3 hours ago -

A solution containing 0.050 g of an unknown electrolyte in 2.50

g of cyclohexane was found...

asked 3 hours ago -

Question 1

a) Hydraulic conductivity of soils is an important parameter for

the design of engineering...

asked 3 hours ago -

Suppose your credit card balance is

$15,000

The minimum payment is

$313

and the annual percentage...

asked 3 hours ago -

Professor plays basketball and makes 75% of free

throws she shoots. If professor shot 5 free...

asked 3 hours ago