Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $374,000 of manufacturing overhead for an estimated allocation base of 1,100 direct labor-hours. The following transactions took place during the year:

- Raw materials purchased on account, $235,000.

- Raw materials used in production (all direct materials), $220,000.

- Utility bills incurred on account, $66,000 (90% related to factory operations, and the remainder related to selling and administrative activities).

- Accrued salary and wage costs:

| Direct labor (1,175 hours) | $ | 265,000 |

| Indirect labor | $ | 97,000 |

| Selling and administrative salaries | $ |

145,000 |

- Maintenance costs incurred on account in the factory, $61,000

- Advertising costs incurred on account, $143,000.

- Depreciation was recorded for the year, $91,000 (80% related to factory equipment, and the remainder related to selling and administrative equipment).

- Rental cost incurred on account, $116,000 (85% related to factory facilities, and the remainder related to selling and administrative facilities).

- Manufacturing overhead cost was applied to jobs, $ ? .

- Cost of goods manufactured for the year, $840,000.

- Sales for the year (all on account) totaled $1,550,000. These goods cost $870,000 according to their job cost sheets.

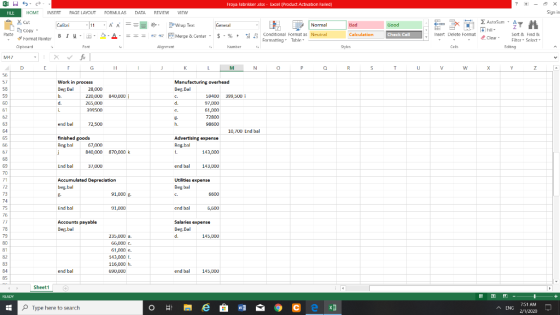

The balances in the inventory accounts at the beginning of the year were:

| Raw Materials | $ | 37,000 |

| Work in Process | $ | 28,000 |

| Finished Goods | $ | 67,000 |

Required:

1. Prepare journal entries to record the preceding transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the beginning inventory balances above.)

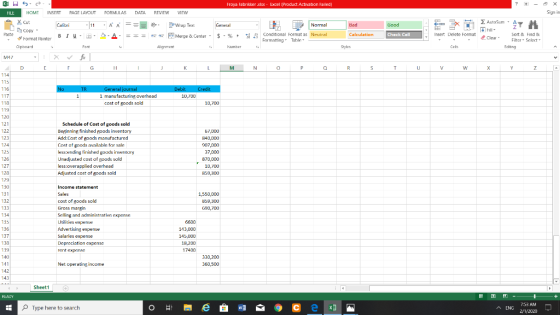

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Homework Answers

Add Answer to:

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $357,000 of manufacturing overhead for an estimated allocation base of 1,020 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $388,800 of manufacturing overhead for an estimated allocation base of 810 direct labor-hours. The following transactions took place during the year. a. Raw materials purchased on...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $388,800 of manufacturing overhead for an estimated allocation base of 810 direct labor-hours. The following transactions took place during the year. a. Raw materials purchased on...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $372,000 of manufacturing overhead for an estimated allocation base of 1,200 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $380,000 of manufacturing overhead for an estimated allocation base of 1,000 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $372,000 of manufacturing overhead for an estimated allocation base of 1,200 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $373,700 of manufacturing overhead for an estimated allocation base of 1,010 direct labor-hours. The following transactions took place during the year: Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that

manufactures specialty heavy equipment for use in North Sea oil

fields. The company uses a job-order costing system that applies

manufacturing overhead cost to jobs on the basis of direct

labor-hours. Its predetermined overhead rate was based on a cost

formula that estimated $350,000 of manufacturing overhead for an

estimated allocation base of 1,000 direct labor-hours. The

following transactions took place during the year:

Raw materials purchased on account,...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The following transactions took place during the year a. Raw materials purchased...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $388,800 of manufacturing overhead for an estimated allocation base of 810 direct labor-hours. The following transactions took place during the year. a. Raw materials purchased on...

Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $388,800 of manufacturing overhead for an estimated allocation base of 810 direct labor-hours. The following transactions took place during the year. a. Raw materials purchased on...

Most questions answered within 3 hours.

-

Water emerges straight down from a faucet with a 1.55-cm

diameter at a speed of 0.515...

asked 20 minutes ago -

Consider the diamond cubic crystal structure of silicon (Si).

The Si–Si distance within this structure is...

asked 38 minutes ago -

The highway speeds of 100 cars are summarized in the frequency

distribution below. Find the mean...

asked 59 minutes ago -

(USING THE PROGRAM MARS) Using the MemoryAccess program we wrote

in class as a starting point,...

asked 43 minutes ago -

a

mixture of na2so4 and nacl weighing 1.2559 grams is dissolved in 50

ML of water,...

asked 46 minutes ago -

Please graph and show all steps for solution.

Billie travels 3.2 km due east in 0.1...

asked 58 minutes ago -

The market demand for medical checkups per day is QF = 25(198 +

nC /20,000 -...

asked 1 hour ago -

Which complement cascade and end products might attack a

Streptococcus invasion of the bloodstream in a...

asked 1 hour ago -

Give the following code segment:

public class Human {

private int age;

....

}

public class...

asked 1 hour ago -

You own a bond portfolio and decide to hedge using futures on 10

year Treasury notes....

asked 1 hour ago -

Discuss the pros and cons of immigration for the Canadian labour

force and for the economy...

asked 1 hour ago -

Q6: Subnet the Class C IP Address 195.1.1.0 So that you

have 10 subnets each with...

asked 1 hour ago