|

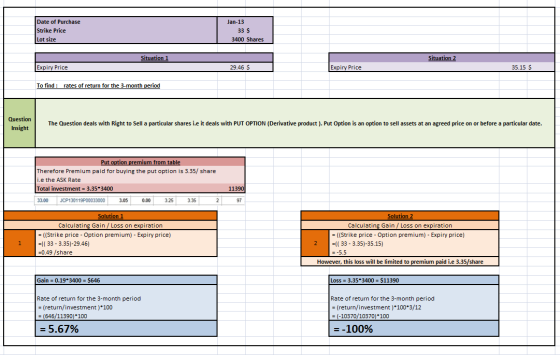

Assume you purchased the right to sell 3,400 shares of JC Penney stock in January 2013 at a strike price of $33 per share. Suppose the stock sells for $29.46 per share immediately before your options’ expiration. What is the rate of return on your investment? What is your rate of return if the stock sells for $35.15 per share? (Enter the rates of return for the 3-month period.) (Negative values should be indicated by a minus sign. Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) |

| Return on investment at $29.46 | % |

| Return on investment at $35.15 | % |

Homework Answers

Add Answer to:

Assume you purchased the right to sell 3,400 shares of JC Penney

stock in January 2013...

Use the following quotes for JCPenney stock options: Assume you purchased the right to sell 3,700...

Use the following quotes for JCPenney stock options:

Assume you purchased the right to sell 3,700 shares of JCPenney

stock in November 2015 at a strike price of $7.00 per share.

Suppose the stock sells for $6.50 per share immediately before your

options’ expiration. What is the rate of return on your investment?

What is your rate of return if the stock sells for $8.00 per share?

Assume your holding period for this investment is exactly three

months. (A negative...

Use the following quotes for JCPenney stock options:

Assume you purchased the right to sell 3,700 shares of JCPenney

stock in November 2015 at a strike price of $7.00 per share.

Suppose the stock sells for $6.50 per share immediately before your

options’ expiration. What is the rate of return on your investment?

What is your rate of return if the stock sells for $8.00 per share?

Assume your holding period for this investment is exactly three

months. (A negative...

I screenshot everything and put them in order, please complete every little boxes. the others are...

I screenshot everything and put them in order, please complete

every little boxes. the others are the info provided for it.

Problems: Nondirection Dependent Strategies -- Straddles and Strangles Straddles and Strangles can be profitable regardless of which way the underlying moves -- profitability is not dependent on the direction of the underlying. Depending on whether you are long or short the position, profitability may not depend upon a move at all. This does not by any means make them...

I screenshot everything and put them in order, please complete

every little boxes. the others are the info provided for it.

Problems: Nondirection Dependent Strategies -- Straddles and Strangles Straddles and Strangles can be profitable regardless of which way the underlying moves -- profitability is not dependent on the direction of the underlying. Depending on whether you are long or short the position, profitability may not depend upon a move at all. This does not by any means make them...

Use the following quotes for JCPenney stock options:

Assume you purchased the right to sell 3,700 shares of JCPenney

stock in November 2015 at a strike price of $7.00 per share.

Suppose the stock sells for $6.50 per share immediately before your

options’ expiration. What is the rate of return on your investment?

What is your rate of return if the stock sells for $8.00 per share?

Assume your holding period for this investment is exactly three

months. (A negative...

Use the following quotes for JCPenney stock options:

Assume you purchased the right to sell 3,700 shares of JCPenney

stock in November 2015 at a strike price of $7.00 per share.

Suppose the stock sells for $6.50 per share immediately before your

options’ expiration. What is the rate of return on your investment?

What is your rate of return if the stock sells for $8.00 per share?

Assume your holding period for this investment is exactly three

months. (A negative...

I screenshot everything and put them in order, please complete

every little boxes. the others are the info provided for it.

Problems: Nondirection Dependent Strategies -- Straddles and Strangles Straddles and Strangles can be profitable regardless of which way the underlying moves -- profitability is not dependent on the direction of the underlying. Depending on whether you are long or short the position, profitability may not depend upon a move at all. This does not by any means make them...

I screenshot everything and put them in order, please complete

every little boxes. the others are the info provided for it.

Problems: Nondirection Dependent Strategies -- Straddles and Strangles Straddles and Strangles can be profitable regardless of which way the underlying moves -- profitability is not dependent on the direction of the underlying. Depending on whether you are long or short the position, profitability may not depend upon a move at all. This does not by any means make them...

Most questions answered within 3 hours.

-

The manager at a car assembly plant believes that the mean

assembly time for a car...

asked 10 minutes ago -

Which of the following is true of electron capture?

A) It decreases the nuclide's mass number...

asked 1 hour ago -

Assuming an efficiency of 43.10%, calculate the actual yield of

magnesium nitrate formed from 114.9 g...

asked 2 hours ago -

The highly pathogenic bacterium Clostridium

perfringens causes gangrene, a disease that results in the

destruction of...

asked 4 hours ago -

In the context of situation analysis, which of the following is

a category for analysis in...

asked 4 hours ago -

In a study of the gas phase decomposition of sulfuryl chloride

at 600 K SO2Cl2(g)SO2(g) +...

asked 4 hours ago -

75 g of 2-propanol (C3H8O) and 25 g of pentane are mixed in a

200 mL...

asked 4 hours ago -

The 2800-turn coil in a dc motor has an area per turn of 1.1 ×

10-2...

asked 4 hours ago -

Draw a combinational logic circuit diagram with a symbol inside

the box for two I/P of...

asked 4 hours ago -

The cliché we use quite a lot in finance is: there is a need to

maximize...

asked 4 hours ago -

In class we discussed the addition of HCl to alpha pinene. Would

you expect one or...

asked 4 hours ago -

I'm trying to explain to my daughter to help her please help

me

I tagged the...

asked 4 hours ago