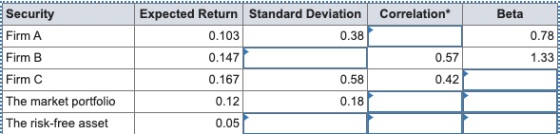

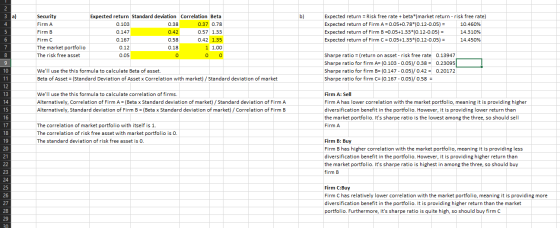

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset:

a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter 0 wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.)

b-2. What is your investment recommendation regarding Firm A for someone with a well-diversified portfolio? Sell or Buy

b-3. What is the expected return of Firm B? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.)

b-4. What is your investment recommendation regarding Firm B for someone with a well-diversified portfolio? Buy or Sell

b-5. What is the expected return of Firm C? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.)

b-6. What is your investment recommendation regarding Firm C for someone with a well-diversified portfolio? Sell or Buy

Homework Answers

Add Answer to:

You have been provided the following data about the securities

of three firms, the market portfolio,...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-fr...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset: a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter 0 wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Security Expected Return Standard Deviation Correlations Beta Firm A 0.101 0.40 0.76 Firm B 0.149 0.59 1.31 Firm C 0.169 0.56 0.44 The...

You have been provided the following data about the securities of three firms, the market portfolio,...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset a. Fill in the missing values in the table. (Leave no cells blank.be certain to enter 0 wherever required. Do not round Intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Correlation Security FA Expected Return Standard Deviation 0.102 033 0.1421 0.162 0.63 0.12 .191 0.08 0.37 Firm The market portfolio The risk tree ass * With...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset a. Fill in the missing values in the table. (Leave no cells blank.be certain to enter 0 wherever required. Do not round Intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Correlation Security FA Expected Return Standard Deviation 0.102 033 0.1421 0.162 0.63 0.12 .191 0.08 0.37 Firm The market portfolio The risk tree ass * With...

You have been provided the following data on the securities of three firms, the market portfolio,...

You have been provided the following data on the securities of three firms, the market portfolio, and the risk-free asset: a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter 0 wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Security Expected Return Standard Deviation Correlation* Beta Firm A .101 .40 .76 Firm B .149 .59 1.31 Firm C .169 .56 .44 The market...

a. Fill in the missing values in the table. (Leave no cells blank - be certain...

a. Fill in the missing values in the table. (Leave no cells

blank - be certain to enter 0 wherever required. Do not round

intermediate calculations and round your answers to 2 decimal

places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round

intermediate calculations and enter your answer as a percent

rounded to 2 decimal places, e.g., 32.16.)

b-2. What is your investment recommendation regarding Firm A for

someone with a well-diversified portfolio? Sell...

a. Fill in the missing values in the table. (Leave no cells

blank - be certain to enter 0 wherever required. Do not round

intermediate calculations and round your answers to 2 decimal

places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round

intermediate calculations and enter your answer as a percent

rounded to 2 decimal places, e.g., 32.16.)

b-2. What is your investment recommendation regarding Firm A for

someone with a well-diversified portfolio? Sell...

a. Fill in the missing values in the table. (Leave no cells blank - be certain...

a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter 0 wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Security Expected Return Standard Deviation Correlation* Beta Firm A .102 .39 .77 Firm B .148 .58 1.32 Firm C .168 .57 .43 The market portfolio .12 .20 The risk-free asset .05 *With the market portfolio. b-1. According to the CAPM, what is the expected...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset: a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter o wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Expected Return Standard Deviation Security Correlation* Beta Firm A 0.120 0.21 0.96 Firm B 0.40 0.130 1.51 Firm C The market portfolio 0.111 0.76...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset: a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter o wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Expected Return Standard Deviation Security Correlation* Beta Firm A 0.120 0.21 0.96 Firm B 0.40 0.130 1.51 Firm C The market portfolio 0.111 0.76...

The market portfolio has an expected return of 11.5 percent and a standard deviation of 21.5...

The market portfolio has an expected return of 11.5 percent and a standard deviation of 21.5 percent. The risk-free rate is 4.5 percent. a. What is the expected return on a well-diversified portfolio with a standard deviation of 8.5 percent? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places (e.g., 32.16).) Expected return % b. What is the standard deviation of a well-diversified portfolio with an expected return of 19.5...

The market portfolio has an expected return of 12.3 percent and a standard deviation of 22.3...

The market portfolio has an expected return of 12.3 percent and a standard deviation of 22.3 percent. The risk-free rate is 5.3 percent. a. What is the expected return on a well-diversified portfolio with a standard deviation of 9.3 percent? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b. What is the standard deviation of a well-diversified portfolio with an expected return of 20.3 percent? (Do not round intermediate...

The market portfolio has an expected return of 12.3 percent and a standard deviation of 22.3 percent. The risk-free rate is 5.3 percent. a. What is the expected return on a well-diversified portfolio with a standard deviation of 9.3 percent? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b. What is the standard deviation of a well-diversified portfolio with an expected return of 20.3 percent? (Do not round intermediate...

Consider the following information about three stocks: Rate of Return If State Occurs State of...

Consider the following information about three stocks: Rate of Return If State Occurs State of Probability of Economy State of Economy Stock A Stock B Stock C Boom .20 .28 .40 .56 Normal .45 .22 .20 .18 Bust .35 .00 −.20 −.48 a-1 If your portfolio is invested 30 percent each in A and B and 40 percent in C, what is the portfolio expected return? (Do not round intermediate calculations. Enter your answer as a percent rounded...

Consider the following information about three stocks: Rate of Return If State Occurs State of Probability...

Consider the following information about three stocks: Rate of Return If State Occurs State of Probability of State of Economy Economy Stock A .32 Stock C .56 Boom Normal Bust Stock B .44 11 -25 26 .50 24 .09 .04 -.45 a-3 a-1. If your portfolio is invested 40 percent each in A and B and 20 percent in C, what is the portfolio expected return? (Do not round intermediate calculations and enter your answer as a percent rounded to...

Consider the following information about three stocks: Rate of Return If State Occurs State of Probability of State of Economy Economy Stock A .32 Stock C .56 Boom Normal Bust Stock B .44 11 -25 26 .50 24 .09 .04 -.45 a-3 a-1. If your portfolio is invested 40 percent each in A and B and 20 percent in C, what is the portfolio expected return? (Do not round intermediate calculations and enter your answer as a percent rounded to...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset a. Fill in the missing values in the table. (Leave no cells blank.be certain to enter 0 wherever required. Do not round Intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Correlation Security FA Expected Return Standard Deviation 0.102 033 0.1421 0.162 0.63 0.12 .191 0.08 0.37 Firm The market portfolio The risk tree ass * With...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset a. Fill in the missing values in the table. (Leave no cells blank.be certain to enter 0 wherever required. Do not round Intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Correlation Security FA Expected Return Standard Deviation 0.102 033 0.1421 0.162 0.63 0.12 .191 0.08 0.37 Firm The market portfolio The risk tree ass * With...

a. Fill in the missing values in the table. (Leave no cells

blank - be certain to enter 0 wherever required. Do not round

intermediate calculations and round your answers to 2 decimal

places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round

intermediate calculations and enter your answer as a percent

rounded to 2 decimal places, e.g., 32.16.)

b-2. What is your investment recommendation regarding Firm A for

someone with a well-diversified portfolio? Sell...

a. Fill in the missing values in the table. (Leave no cells

blank - be certain to enter 0 wherever required. Do not round

intermediate calculations and round your answers to 2 decimal

places, e.g., 32.16.)

b-1. What is the expected return of Firm A? (Do not round

intermediate calculations and enter your answer as a percent

rounded to 2 decimal places, e.g., 32.16.)

b-2. What is your investment recommendation regarding Firm A for

someone with a well-diversified portfolio? Sell...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset: a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter o wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Expected Return Standard Deviation Security Correlation* Beta Firm A 0.120 0.21 0.96 Firm B 0.40 0.130 1.51 Firm C The market portfolio 0.111 0.76...

You have been provided the following data about the securities of three firms, the market portfolio, and the risk-free asset: a. Fill in the missing values in the table. (Leave no cells blank - be certain to enter o wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Expected Return Standard Deviation Security Correlation* Beta Firm A 0.120 0.21 0.96 Firm B 0.40 0.130 1.51 Firm C The market portfolio 0.111 0.76...

The market portfolio has an expected return of 12.3 percent and a standard deviation of 22.3 percent. The risk-free rate is 5.3 percent. a. What is the expected return on a well-diversified portfolio with a standard deviation of 9.3 percent? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b. What is the standard deviation of a well-diversified portfolio with an expected return of 20.3 percent? (Do not round intermediate...

The market portfolio has an expected return of 12.3 percent and a standard deviation of 22.3 percent. The risk-free rate is 5.3 percent. a. What is the expected return on a well-diversified portfolio with a standard deviation of 9.3 percent? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b. What is the standard deviation of a well-diversified portfolio with an expected return of 20.3 percent? (Do not round intermediate...

Consider the following information about three stocks: Rate of Return If State Occurs State of Probability of State of Economy Economy Stock A .32 Stock C .56 Boom Normal Bust Stock B .44 11 -25 26 .50 24 .09 .04 -.45 a-3 a-1. If your portfolio is invested 40 percent each in A and B and 20 percent in C, what is the portfolio expected return? (Do not round intermediate calculations and enter your answer as a percent rounded to...

Consider the following information about three stocks: Rate of Return If State Occurs State of Probability of State of Economy Economy Stock A .32 Stock C .56 Boom Normal Bust Stock B .44 11 -25 26 .50 24 .09 .04 -.45 a-3 a-1. If your portfolio is invested 40 percent each in A and B and 20 percent in C, what is the portfolio expected return? (Do not round intermediate calculations and enter your answer as a percent rounded to...

Most questions answered within 3 hours.

-

Computer Programming II CS141(Java)

Mention the appropriate relationship between following

classes:

HOD–StaffMember

Car–Ferrari

Student-Address

BankAccount–FixedAccount

House-Building...

asked 2 hours ago -

Assume one of your finals has 50 questions on it, and

lucky for you, it's all...

asked 3 hours ago -

Rice Products in Bangladesh

Business behavior is derived in large part from the basic cultural

environment...

asked 4 hours ago -

The following base sequence is found for a mRNA fragment from

wild-type E. coli: 5'- UAUCAGUAGAUAAUGUAACC-3'...

asked 5 hours ago -

For this exercise, round all regression parameters to three

decimal places.

One of the two tables...

asked 5 hours ago -

What is the 5% level of significance for mean = 3.60, standard

deviation = 0.94, and...

asked 5 hours ago -

Prior to beginning work on this discussion, please read the

article by Hayley Peterson, 15 Companies...

asked 6 hours ago -

Which pair of aqueous solutions, when mixed, will form a

precipitate?

A) NaNO3 and AgC2H3O2

B)...

asked 6 hours ago -

1-Write an algorithm to get two numbers from the user (as

inputs) and calculate the sum...

asked 9 hours ago -

Define white-collar crime. What is the difference between

offender and offense-based definitions of white-collar crime? What...

asked 10 hours ago -

Consider a reaction which is 1st order with respect to A and 1st

order with respect...

asked 10 hours ago -

c++

The length of the hypotenuse of a right-angled triangle is the

square root of the...

asked 10 hours ago