Homework Answers

2-21

1.

2. If 100 students attend, the total cost would be

Fixed Cost - $2000 (band) +$1200 (caterer) = $3200

Variable Cost - 100 students x $8 = $800. (Multiplying with $8 as the cost charged by caterer is 18$ and recovery from the students is 10$, so net 18-10=8)

Total Cost for 100 students = 3200+800 = $4000

Cost per attendee = 4000/100 = $40 per attendee

3. If 500 students attend, the total cost would be

Fixed Cost - $2000 (band) +$1200 (caterer) = $3200

Variable Cost - 500 students x $8 = $4000. (Multiplying with $8 as the cost charged by caterer is 18$ and recovery from the students is 10$, so net 18-10=8)

Total Cost for 100 students = 3200+4000 = $7200

Cost per attendee =7200/500 = $14.40 per attendee

4.

As the president of the student association, if the number of attendee are greater than 320, (total fixed cost / contribution per attendee) ($3200/$10), we would use cost per attendee as a base to recover the cost. However if the attendance is less than 320, we would not use the cost per attendee as the fixed costs itself would not be recovered.

3-34

1. First find out the Contribution margin of Small Trampoline (ST) and Large Trampoline(LT)

Contribution Margin = Sales price - Variable Cost

CM for ST = 200-120 = $80

CM for BT = 600-420 = $180

Given sales mix is 4 ST for 1 LT.

Let 4 ST along with 1 LT 1 unit of Sale. (Say Total Sale (TS))

So contribution from that 1 unit (TS) will be (4 x 80) + (1 x 180) = $500.

Given Fixed Cost is $ 1,250,000.

So number of units to be sold for break even will be Fixed Cost divided by Contribution from 1 TS.

1,250,000/500 = 2500 units of TS.

Break even in Units

This amounts to 2500 x 4 = 10,000 units of Small Trampoline

2500 x 1 = 2500 units of Large Trampoline.

Total units 12500 units.

Break even in Sales

10,000 units of ST x $ 200 = $2,000,000

2500 units of LT x $ 600 = $ 1,500,000

Total Break even Sales = 3,500,000.

2.

Increase in Fixed cost by 202,000. New Fixed cost to be recovered = 1,250,000+202,000 = 1,452,000.

Change in Contribution Margins

CM of ST = 200-(120-15) = $95

CM of LT = 600 - (420-45) = $225.

Given that the same sales mix will continue.

Given sales mix is 4 ST for 1 LT.

Let 4 ST along with 1 LT 1 unit of Sale. (Say Total Sale (TS))

So contribution from that 1 unit (TS) will be (4 x 95) + (1 x 225) = $605.

Given Fixed Cost is $ 1,452,000.

So number of units to be sold for break even will be Fixed Cost divided by Contribution from 1 TS.

1,452,000/605 = 2400 units of TS.

Break even in Units

This amounts to 2400 x 4 = 9,600 units of Small Trampoline

2400 x 1 = 2400 units of Large Trampoline.

Total units 12000 units

Break even in Sales

9600 units of ST x $ 200 = $1,920,000

2400 units of LT x $ 600 = $ 1,440,000

Total Break even Sales = 3,360,000.

3.

Indifference point is nothing but the point where choosing either of the 2 options will not impact out profitability

Contribution Margin - Fixed Cost should be the same for "T" number of units

500 x T - 1,250,000 = 605 x T - 1,452,000

105T = 202,000

T = 202000/105

= 1925 (rounded off to nearest 5 for easier calculation)

The indifference point of sales will be Break even point as per Option 1 + 1925 units

12500+1925 = 14425 units.

As 13000 units of sales lie below the indifference point of 14425 units. It would be favourable to use Option 2 that is it should buy the new equipment.

Add Answer to:

please solve 1-4 in detail

please solve 1-3 in only 3-34.

could you please tell why...

How to draw a graph for Revenue and Costs Total costs and unit costs. A student...

How to draw a graph for Revenue and Costs Total costs and unit costs. A student association has hired a band and a caterer for a graduation party. The band will charge a fixed fee of $1,000 for an evening of music, and the caterer will charge a fixed fee of $600 for the party setup and an additional S3 per person who attends. Snacks and soft drinks will be provided bythe caterer for the duration of the party. Students...

How to draw a graph for Revenue and Costs Total costs and unit costs. A student association has hired a band and a caterer for a graduation party. The band will charge a fixed fee of $1,000 for an evening of music, and the caterer will charge a fixed fee of $600 for the party setup and an additional S3 per person who attends. Snacks and soft drinks will be provided bythe caterer for the duration of the party. Students...

how do you find fixed costs? Requirement 3. Suppose 220,000 units are sold but only 22,000...

how

do you find fixed costs?

Requirement 3. Suppose 220,000 units are sold but only 22,000 of them are deluse. Compute the operating incomempute the breakeven point in units. Compare your answer with the answer to requirement 1. What is the major lesson of this problem? Compute the operating income il 220.000 units are sold but only 22,000 of them are deluxe Standard Carrier Deluxe Carrier Total 198000 22000 220000 Units sold Revenues a $20 and 537 per unit 3960000...

how

do you find fixed costs?

Requirement 3. Suppose 220,000 units are sold but only 22,000 of them are deluse. Compute the operating incomempute the breakeven point in units. Compare your answer with the answer to requirement 1. What is the major lesson of this problem? Compute the operating income il 220.000 units are sold but only 22,000 of them are deluxe Standard Carrier Deluxe Carrier Total 198000 22000 220000 Units sold Revenues a $20 and 537 per unit 3960000...

The StackpoleStackpole Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted...

The StackpoleStackpole Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: LOADING... (Click the icon to view the budgeted income statement.)Read the requirements LOADING... . Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 1 deluxe unit(s) sold, standard units are sold. Determine the formula used to calculate the...

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier....

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 1 deluxe unit(s) sold, 4 standard units are sold. Determine the formula used to calculate the breakeven...

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 1 deluxe unit(s) sold, 4 standard units are sold. Determine the formula used to calculate the breakeven...

Homework: Graded Homework Chapter 3 Save Score: 0.1 of 1 pt 5 of 5 (5 complete)...

Homework: Graded Homework Chapter 3 Save Score: 0.1 of 1 pt 5 of 5 (5 complete) HW Score: 29.57%, 1.48 of 5 pts P3-51 (similar to) e Question Help The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves...

Homework: Graded Homework Chapter 3 Save Score: 0.1 of 1 pt 5 of 5 (5 complete) HW Score: 29.57%, 1.48 of 5 pts P3-51 (similar to) e Question Help The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves...

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier....

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement.) Read the requirements Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 2 deluxe units) sold. standard units are sold. Data Table A Requirements Total Standard Carrier Deluxe Carrier...

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement.) Read the requirements Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 2 deluxe units) sold. standard units are sold. Data Table A Requirements Total Standard Carrier Deluxe Carrier...

The Ogden Company retails two products: a standard and a deluxe version of a luggage carrier....

The Ogden Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: E (Click the icon to view the budgeted income statement.) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 2 deluxe unit(s) sold, standard units are sold. * Requirements - X Data Table Total 200,000...

The Ogden Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: E (Click the icon to view the budgeted income statement.) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 2 deluxe unit(s) sold, standard units are sold. * Requirements - X Data Table Total 200,000...

The Coughlin Company retails two products: a standard and a deluxe version of a luggage carrier....

The Coughlin Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement.) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. i Requirements Begin by determining the sales mix. For every 1 deluxe unit(s) sold, standard units are sold. 1. Compute the breakeven point in units,...

The Coughlin Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement.) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. i Requirements Begin by determining the sales mix. For every 1 deluxe unit(s) sold, standard units are sold. 1. Compute the breakeven point in units,...

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier....

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement) Read the requirements Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 1 deluxe unit(s) sold, 4 standard units are sold. Determine the formula used to calculate the breakeven...

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement) Read the requirements Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 1 deluxe unit(s) sold, 4 standard units are sold. Determine the formula used to calculate the breakeven...

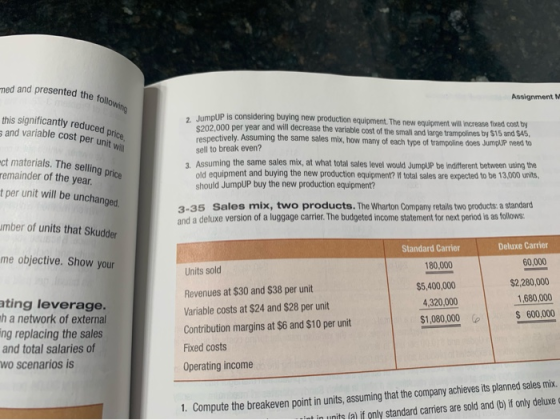

The Wharton Company retails two products: a standard and a deluxe version of a luggage carrier....

The Wharton Company retails two products: a standard and a

deluxe version of a luggage carrier. The budgeted income statement

for next period is as follows

0 Data Table Total 180,000 6,336,000 4,320,000 Standard Carrier Deluxe Carrier Units sold 108,000 72,000 Revenues at $30 and $43 per unit 3,240,000 $ 3,096,000 $ Variable costs at $22 and $27 per unit 2,376,000 1,944,000 Contribution margins at $8 and 916 per unit $_ 864,000 $ 1,152,000 Fixed costs Operating income $ 2,016,000...

The Wharton Company retails two products: a standard and a

deluxe version of a luggage carrier. The budgeted income statement

for next period is as follows

0 Data Table Total 180,000 6,336,000 4,320,000 Standard Carrier Deluxe Carrier Units sold 108,000 72,000 Revenues at $30 and $43 per unit 3,240,000 $ 3,096,000 $ Variable costs at $22 and $27 per unit 2,376,000 1,944,000 Contribution margins at $8 and 916 per unit $_ 864,000 $ 1,152,000 Fixed costs Operating income $ 2,016,000...

How to draw a graph for Revenue and Costs Total costs and unit costs. A student association has hired a band and a caterer for a graduation party. The band will charge a fixed fee of $1,000 for an evening of music, and the caterer will charge a fixed fee of $600 for the party setup and an additional S3 per person who attends. Snacks and soft drinks will be provided bythe caterer for the duration of the party. Students...

How to draw a graph for Revenue and Costs Total costs and unit costs. A student association has hired a band and a caterer for a graduation party. The band will charge a fixed fee of $1,000 for an evening of music, and the caterer will charge a fixed fee of $600 for the party setup and an additional S3 per person who attends. Snacks and soft drinks will be provided bythe caterer for the duration of the party. Students...

how

do you find fixed costs?

Requirement 3. Suppose 220,000 units are sold but only 22,000 of them are deluse. Compute the operating incomempute the breakeven point in units. Compare your answer with the answer to requirement 1. What is the major lesson of this problem? Compute the operating income il 220.000 units are sold but only 22,000 of them are deluxe Standard Carrier Deluxe Carrier Total 198000 22000 220000 Units sold Revenues a $20 and 537 per unit 3960000...

how

do you find fixed costs?

Requirement 3. Suppose 220,000 units are sold but only 22,000 of them are deluse. Compute the operating incomempute the breakeven point in units. Compare your answer with the answer to requirement 1. What is the major lesson of this problem? Compute the operating income il 220.000 units are sold but only 22,000 of them are deluxe Standard Carrier Deluxe Carrier Total 198000 22000 220000 Units sold Revenues a $20 and 537 per unit 3960000...

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 1 deluxe unit(s) sold, 4 standard units are sold. Determine the formula used to calculate the breakeven...

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 1 deluxe unit(s) sold, 4 standard units are sold. Determine the formula used to calculate the breakeven...

Homework: Graded Homework Chapter 3 Save Score: 0.1 of 1 pt 5 of 5 (5 complete) HW Score: 29.57%, 1.48 of 5 pts P3-51 (similar to) e Question Help The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves...

Homework: Graded Homework Chapter 3 Save Score: 0.1 of 1 pt 5 of 5 (5 complete) HW Score: 29.57%, 1.48 of 5 pts P3-51 (similar to) e Question Help The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves...

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement.) Read the requirements Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 2 deluxe units) sold. standard units are sold. Data Table A Requirements Total Standard Carrier Deluxe Carrier...

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement.) Read the requirements Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 2 deluxe units) sold. standard units are sold. Data Table A Requirements Total Standard Carrier Deluxe Carrier...

The Ogden Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: E (Click the icon to view the budgeted income statement.) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 2 deluxe unit(s) sold, standard units are sold. * Requirements - X Data Table Total 200,000...

The Ogden Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: E (Click the icon to view the budgeted income statement.) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 2 deluxe unit(s) sold, standard units are sold. * Requirements - X Data Table Total 200,000...

The Coughlin Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement.) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. i Requirements Begin by determining the sales mix. For every 1 deluxe unit(s) sold, standard units are sold. 1. Compute the breakeven point in units,...

The Coughlin Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement.) Read the requirements. Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. i Requirements Begin by determining the sales mix. For every 1 deluxe unit(s) sold, standard units are sold. 1. Compute the breakeven point in units,...

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement) Read the requirements Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 1 deluxe unit(s) sold, 4 standard units are sold. Determine the formula used to calculate the breakeven...

The Alves Company retails two products: a standard and a deluxe version of a luggage carrier. The budgeted income statement for next period is as follows: (Click the icon to view the budgeted income statement) Read the requirements Requirement 1. Compute the breakeven point in units, assuming that the company achieves its planned sales mix. Begin by determining the sales mix. For every 1 deluxe unit(s) sold, 4 standard units are sold. Determine the formula used to calculate the breakeven...

The Wharton Company retails two products: a standard and a

deluxe version of a luggage carrier. The budgeted income statement

for next period is as follows

0 Data Table Total 180,000 6,336,000 4,320,000 Standard Carrier Deluxe Carrier Units sold 108,000 72,000 Revenues at $30 and $43 per unit 3,240,000 $ 3,096,000 $ Variable costs at $22 and $27 per unit 2,376,000 1,944,000 Contribution margins at $8 and 916 per unit $_ 864,000 $ 1,152,000 Fixed costs Operating income $ 2,016,000...

The Wharton Company retails two products: a standard and a

deluxe version of a luggage carrier. The budgeted income statement

for next period is as follows

0 Data Table Total 180,000 6,336,000 4,320,000 Standard Carrier Deluxe Carrier Units sold 108,000 72,000 Revenues at $30 and $43 per unit 3,240,000 $ 3,096,000 $ Variable costs at $22 and $27 per unit 2,376,000 1,944,000 Contribution margins at $8 and 916 per unit $_ 864,000 $ 1,152,000 Fixed costs Operating income $ 2,016,000...

Most questions answered within 3 hours.

-

Your system is rejecting the question am asking which is

preceded by a case study. It...

asked 4 seconds from now -

A member of the volleyball team spikes the ball. During this

process, she changes the velocity...

asked 4 minutes ago -

Are adult gamers less likely to use a gaming console (Xbox,

PlayStation, Wii, etc...) than teen...

asked 57 minutes ago -

The University of

Texas recently reported that 43% of college students aged 18-24

would spend their...

asked 1 hour ago -

The length of stay at a specific emergency department in

Phoenix, Arizona, in 2009 had a...

asked 24 minutes ago -

. Please give the mechanism for this type of problem. Step by

Step

The toxin that...

asked 27 minutes ago -

If you have a 1M stock solution and you want to dilute 1 :10

with water,...

asked 29 minutes ago -

In a load instruction, the effective address is obtained by

A) Retriving the address from a...

asked 29 minutes ago -

Use the following information to answer this question.

Windswept, Inc. 2017 Income Statement ($ in millions)...

asked 30 minutes ago -

A mutual fund salesperson has arranged to call on four people

tomorrow. Based on past experience...

asked 1 hour ago -

Let the RV Y has the pdf

f ( y ) = 6 y ( 1...

asked 1 hour ago -

Question 12

Where should a copy of a private key should be placed so it is...

asked 32 minutes ago