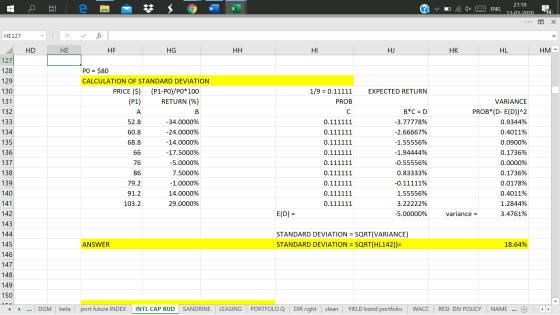

Suppose a U.S. investor wishes to invest in a British firm currently selling for £40 per...

Suppose a U.S. investor wishes to invest in a British firm currently selling for £40 per share. The investor has $20,000 to invest, and the current exchange rate is $2/£. Consider three possible prices per share at £33, £38, and £43 after 1 year. Also, consider three possible exchange rates at $1.6/£, $2/£, and $2.4/£ after 1 year. Calculate the standard deviation of both the pound- and dollar-denominated rates of return if each of the nine outcomes (three possible prices per share in pounds times three possible exchange rates) is equally likely. (Do not round intermediate calculations. Round your answers to 2 decimal places.)

Homework Answers

SEE THE IMAGE. ANY DOUBTS,

FEEL FREE TO ASK. THUMBS UP PLEASE

Add Answer to:

Suppose a U.S. investor wishes to invest in a British firm

currently selling for £40 per...

Suppose a U.S. investor wishes to invest in a British firm currently selling for £80 per...

Suppose a U.S. investor wishes to invest in a British firm currently selling for £80 per share. The investor has $16,000 to invest, and the current exchange rate is $2/S. Consider three possible prices per share at £77, £82, and £87 after 1 year. Also, consider three possible exchange rates at $1.6/6, $2/ , and $2.4/E after 1 year. Calculate the standard deviation of both the pound- and dollar-denominated rates of return if each of the nine outcomes (three possible...

Suppose a U.S. investor wishes to invest in a British firm currently selling for £80 per share. The investor has $16,000 to invest, and the current exchange rate is $2/S. Consider three possible prices per share at £77, £82, and £87 after 1 year. Also, consider three possible exchange rates at $1.6/6, $2/ , and $2.4/E after 1 year. Calculate the standard deviation of both the pound- and dollar-denominated rates of return if each of the nine outcomes (three possible...

Suppose a U.S. investor wishes to invest in a British firm currently selling for £25 per...

Suppose a U.S. investor wishes to invest in a British firm currently selling for £25 per share. The investor has $14,400 to invest, and the current exchange rate is $2/£. Consider three possible prices per share at £21, £26, and £31 after 1 year. Also, consider three possible exchange rates at $1.7/£, $2/£, and $2.3/£ after 1 year. Calculate the standard deviation of both the pound- and dollar-denominated rates of return if each of the nine outcomes (three possible prices...

Suppose a U.S. investor wishes to invest in a British firm currently selling for £25 per share. The investor has $14,400 to invest, and the current exchange rate is $2/£. Consider three possible prices per share at £21, £26, and £31 after 1 year. Also, consider three possible exchange rates at $1.7/£, $2/£, and $2.3/£ after 1 year. Calculate the standard deviation of both the pound- and dollar-denominated rates of return if each of the nine outcomes (three possible prices...

Standard deviation of pound- and dollar-denominated rates of return

I have this homework question: "Suppose a U.S. investor wishes to invest in a British firm currently selling for £90 per share. The investor has $36,000 to invest, and the current exchange rate is $2/£. Consider three possible prices per share at £88, £93, and £98 after 1 year. Also, consider three possible exchange rates at $1.8/£, $2/£, and $2.2/£ after 1 year. Calculate the standard deviation of both the pound- and dollar-denominated rates of return if each of the...

Suppose a U.S. Investor wishes to invest in a British firm currently selling for £30 per...

Suppose a U.S. Investor wishes to invest in a British firm currently selling for £30 per share. The investor has $14,400 to invest, and the current exchange rate is $2/£. Suppose now the investor also sells forward £7,200 at a forward exchange rate of $2.05/£. Calculate the dollar-denominated returns for each scenario. (Round your answers to 2 decimal places. Negative amounts should be indicated by a minus sign.) Price per Share ) Rate of Return (%) at Given Exchange Rate...

Suppose a U.S. Investor wishes to invest in a British firm currently selling for £30 per share. The investor has $14,400 to invest, and the current exchange rate is $2/£. Suppose now the investor also sells forward £7,200 at a forward exchange rate of $2.05/£. Calculate the dollar-denominated returns for each scenario. (Round your answers to 2 decimal places. Negative amounts should be indicated by a minus sign.) Price per Share ) Rate of Return (%) at Given Exchange Rate...

Suppose a US investor wishes to invest in a British firm currently selling for £20 per...

Suppose a US investor wishes to invest in a British firm currently selling for £20 per share. The investor has $13,600 to invest, and the current exchange rate is $2/£. Suppose now the investor also sells forward $6,800 at a forward exchange rate of $1.90/ Calculate the dollar-denominated returns for each scenario. (Round your answers to 2 decimal places. Negative amounts should be indicated by a minus sign.) Price per Share (C) Exchange Rate: Rate of Return (%) at Given...

Suppose a US investor wishes to invest in a British firm currently selling for £20 per share. The investor has $13,600 to invest, and the current exchange rate is $2/£. Suppose now the investor also sells forward $6,800 at a forward exchange rate of $1.90/ Calculate the dollar-denominated returns for each scenario. (Round your answers to 2 decimal places. Negative amounts should be indicated by a minus sign.) Price per Share (C) Exchange Rate: Rate of Return (%) at Given...

Problem 25-5 Suppose a US investor wishes to invest in a British firm currently selling for...

Problem 25-5 Suppose a US investor wishes to invest in a British firm currently selling for £33 per share. The investor has $66,000 to invest, and the current exchange rate is $2/. Suppose now the investor also sells forward $33,000 at a forward exchange rate of $205/5 Calculate the dollar-denominated returns for each scenario (Round your answers to 2 decimal places. Negative amounts should be indicated by a minus sign.) Price per Share (E) Rate of Return (%) at Given...

Problem 25-5 Suppose a US investor wishes to invest in a British firm currently selling for £33 per share. The investor has $66,000 to invest, and the current exchange rate is $2/. Suppose now the investor also sells forward $33,000 at a forward exchange rate of $205/5 Calculate the dollar-denominated returns for each scenario (Round your answers to 2 decimal places. Negative amounts should be indicated by a minus sign.) Price per Share (E) Rate of Return (%) at Given...

Consider a Spanish investor with 5,000 euros to place in a bank deposit in either Spain...

Consider a Spanish investor with 5,000 euros to place in a bank deposit in either Spain or Great Britain. The (one-year) interest rate on bank deposits is 3% in Britain and 4.5% in Spain. The (one-year) forward euro-pound exchange rate is 1.7 euros per pound and the spot rate is 1.6 euros per pound. Answer the following questions! a) What is the euro-denominated return (i.e. the total amount of Euros) on Spanish deposits for this investor? b) What is the...

Consider a Spanish investor with 5,000 euros to place in a bank deposit in either Spain or Great Britain. The (one-year) interest rate on bank deposits is 3% in Britain and 4.5% in Spain. The (one-year) forward euro-pound exchange rate is 1.7 euros per pound and the spot rate is 1.6 euros per pound. Answer the following questions! a) What is the euro-denominated return (i.e. the total amount of Euros) on Spanish deposits for this investor? b) What is the...

Grant, Inc., is a well-known U.S. firm that needs to borrow 10 million British pounds to support a new business in the U...

Grant, Inc., is a well-known U.S. firm that needs to borrow 10 million British pounds to support a new business in the United Kingdom. However, it cannot obtain financing from British banks because it is not yet established within the United Kingdom. It decides to issue dollar-denominated debt (at par value) in the U.S., for which it will pay an annual coupon rate of 10%. It then will convert the dollar proceeds from the debt issue into British pounds at...

A French firm is considering selling its line of laundry machines in the U.K. The business...

A French firm is considering selling its line of laundry machines in the U.K. The business risk will be identical to the firm's existing line of business in the euro zone, the cost of capital in the euro zone is i€ = 10%. The expected inflation rate over the next two years in the U.K. is 3% per year and 2% per year in the euro zone. The spot exchange rates are $1.80 = £1.00 and $1.15 = €1.00. The...

After all foreign and U.S. taxes, a U.S. corporation expects to receive 2 pounds of dividends...

After all foreign and U.S. taxes, a U.S. corporation expects to receive 2 pounds of dividends per share from a British subsidiary this year. The exchange rate at the end of the year is expected to be $2.03 per pound, and the pound is expected to depreciate 7% against the dollar each year for an indefinite period. The dividend (in pounds) is expected to grow at 9% a year indefinitely. The parent U.S. corporation owns 7 million shares of the...

Suppose a U.S. investor wishes to invest in a British firm currently selling for £80 per share. The investor has $16,000 to invest, and the current exchange rate is $2/S. Consider three possible prices per share at £77, £82, and £87 after 1 year. Also, consider three possible exchange rates at $1.6/6, $2/ , and $2.4/E after 1 year. Calculate the standard deviation of both the pound- and dollar-denominated rates of return if each of the nine outcomes (three possible...

Suppose a U.S. investor wishes to invest in a British firm currently selling for £80 per share. The investor has $16,000 to invest, and the current exchange rate is $2/S. Consider three possible prices per share at £77, £82, and £87 after 1 year. Also, consider three possible exchange rates at $1.6/6, $2/ , and $2.4/E after 1 year. Calculate the standard deviation of both the pound- and dollar-denominated rates of return if each of the nine outcomes (three possible...

Suppose a U.S. investor wishes to invest in a British firm currently selling for £25 per share. The investor has $14,400 to invest, and the current exchange rate is $2/£. Consider three possible prices per share at £21, £26, and £31 after 1 year. Also, consider three possible exchange rates at $1.7/£, $2/£, and $2.3/£ after 1 year. Calculate the standard deviation of both the pound- and dollar-denominated rates of return if each of the nine outcomes (three possible prices...

Suppose a U.S. investor wishes to invest in a British firm currently selling for £25 per share. The investor has $14,400 to invest, and the current exchange rate is $2/£. Consider three possible prices per share at £21, £26, and £31 after 1 year. Also, consider three possible exchange rates at $1.7/£, $2/£, and $2.3/£ after 1 year. Calculate the standard deviation of both the pound- and dollar-denominated rates of return if each of the nine outcomes (three possible prices...

Suppose a U.S. Investor wishes to invest in a British firm currently selling for £30 per share. The investor has $14,400 to invest, and the current exchange rate is $2/£. Suppose now the investor also sells forward £7,200 at a forward exchange rate of $2.05/£. Calculate the dollar-denominated returns for each scenario. (Round your answers to 2 decimal places. Negative amounts should be indicated by a minus sign.) Price per Share ) Rate of Return (%) at Given Exchange Rate...

Suppose a U.S. Investor wishes to invest in a British firm currently selling for £30 per share. The investor has $14,400 to invest, and the current exchange rate is $2/£. Suppose now the investor also sells forward £7,200 at a forward exchange rate of $2.05/£. Calculate the dollar-denominated returns for each scenario. (Round your answers to 2 decimal places. Negative amounts should be indicated by a minus sign.) Price per Share ) Rate of Return (%) at Given Exchange Rate...

Suppose a US investor wishes to invest in a British firm currently selling for £20 per share. The investor has $13,600 to invest, and the current exchange rate is $2/£. Suppose now the investor also sells forward $6,800 at a forward exchange rate of $1.90/ Calculate the dollar-denominated returns for each scenario. (Round your answers to 2 decimal places. Negative amounts should be indicated by a minus sign.) Price per Share (C) Exchange Rate: Rate of Return (%) at Given...

Suppose a US investor wishes to invest in a British firm currently selling for £20 per share. The investor has $13,600 to invest, and the current exchange rate is $2/£. Suppose now the investor also sells forward $6,800 at a forward exchange rate of $1.90/ Calculate the dollar-denominated returns for each scenario. (Round your answers to 2 decimal places. Negative amounts should be indicated by a minus sign.) Price per Share (C) Exchange Rate: Rate of Return (%) at Given...

Problem 25-5 Suppose a US investor wishes to invest in a British firm currently selling for £33 per share. The investor has $66,000 to invest, and the current exchange rate is $2/. Suppose now the investor also sells forward $33,000 at a forward exchange rate of $205/5 Calculate the dollar-denominated returns for each scenario (Round your answers to 2 decimal places. Negative amounts should be indicated by a minus sign.) Price per Share (E) Rate of Return (%) at Given...

Problem 25-5 Suppose a US investor wishes to invest in a British firm currently selling for £33 per share. The investor has $66,000 to invest, and the current exchange rate is $2/. Suppose now the investor also sells forward $33,000 at a forward exchange rate of $205/5 Calculate the dollar-denominated returns for each scenario (Round your answers to 2 decimal places. Negative amounts should be indicated by a minus sign.) Price per Share (E) Rate of Return (%) at Given...

Consider a Spanish investor with 5,000 euros to place in a bank deposit in either Spain or Great Britain. The (one-year) interest rate on bank deposits is 3% in Britain and 4.5% in Spain. The (one-year) forward euro-pound exchange rate is 1.7 euros per pound and the spot rate is 1.6 euros per pound. Answer the following questions! a) What is the euro-denominated return (i.e. the total amount of Euros) on Spanish deposits for this investor? b) What is the...

Consider a Spanish investor with 5,000 euros to place in a bank deposit in either Spain or Great Britain. The (one-year) interest rate on bank deposits is 3% in Britain and 4.5% in Spain. The (one-year) forward euro-pound exchange rate is 1.7 euros per pound and the spot rate is 1.6 euros per pound. Answer the following questions! a) What is the euro-denominated return (i.e. the total amount of Euros) on Spanish deposits for this investor? b) What is the...

Most questions answered within 3 hours.

-

(Expected rate of return and risk) Carter Inc. is evaluating a

security. Calculate the investment’s expected...

asked 1 hour ago -

What specific indicators can point to lack of progress for

African Americans in American society?

asked 2 hours ago -

1-The Electrons in a beam are moving at 2.7×108 m/s in an

electric field of 15000...

asked 2 hours ago -

A gas tank is a vertical cylinder. It has a radius of 1m, a

height of...

asked 3 hours ago -

Accent Software faces the following conditions. All of these

support Accent’s use of a market-penetration pricing...

asked 4 hours ago -

A mathematically inclined friend emails you the following

instructions: "Meet me in the cafeteria the first...

asked 4 hours ago -

A monopoly sells in two countries . The demand curves in the two

countries are p1...

asked 5 hours ago -

A .15kg rubber ball is bounced off a wall. Before hitting the

wall, the ball moves...

asked 5 hours ago -

A manufacturing company preparing to build a new plant is

considering three potential locations for it....

asked 5 hours ago -

B. If compound Y has approximately the same values of solubility

in toluene as compound X,...

asked 6 hours ago -

Oscar Inc. has inventory in Japan valued at 39,051,000 Yen one

year ago. One year ago...

asked 6 hours ago -

If Canada suffered from "fundamental disequilibrium," and its

government choose not to devalue its currency, a...

asked 6 hours ago