Homework Answers

Add Answer to:

1000 euro par value, 3% annual-coupon bond was issued 1.03.2015 and has 30 year maturity You...

Rackawieca Corp. has issued a 7% annual coupon bond with a par of $1,000 and with...

Rackawieca Corp. has issued a 7% annual coupon bond with a par of $1,000 and with 2 years to maturity. Find the value of this bond if the required rate of return is 7%. Say the price of this bond dropped by $50 later this afternoon. What is the YTM of this bond at the lower price? Calculate the duration and modified duration of this bond. Demonstrate that the modified duration is a reasonable measure of interest rate sensitivity of...

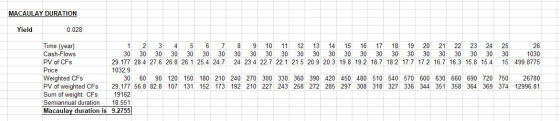

Bond Analysis Issue data Purchase date Maturity date Par value Coupon rate Frequency Market price October...

Bond Analysis Issue data Purchase date Maturity date Par value Coupon rate Frequency Market price October 12,2002 September 26,2012 November 24,2019 2279 1.5100% annually 94% All values must be rounded up to 2 decimals Characteristics Value 1 Yield to maturity <> 2 Macaulay duration <> 3 Modified duration <> 4 If the yield-to-maturity increases by 100 bps,the bond price will be changed by (calculate it precisely) <> 5 If the yield-to- maturity increases by 10 bps, the bond price will...

1. An investor purchases an annual coupon bond with a 6% coupon rate and exactly 20...

1. An investor purchases an annual coupon bond with a 6% coupon rate and exactly 20 years remaining until maturity at a price equal to par value. The investor’s investment horizon is eight years. The approximate modified duration of the bond is 11.470 years. What is the duration gap at the time of purchase? (Hint: use approximate Macaulay duration to calculate the duration gap) 2. An investor plans to retire in 10 years. As part of the retirement portfolio, the...

Bond Coupon Rate Maturity Year Par Value 1 7.5% 2032 1000 2 8.25% 2029 1000 3...

Bond Coupon Rate Maturity Year Par Value 1 7.5% 2032 1000 2 8.25% 2029 1000 3 6.0% 2023 1000 a.) Assuming that bonds pay annual coupon, estimate the market value of each bond at a discount rate of 7.4% b.) Assuming that bonds pay annual coupon, what will happen to the price of each bond if market rates suddenly decrease from 7.4% to 6.2%? Which of the three bonds will have the greatest percentage change in price? c.) Assuming that...

A bond face value is $1000, with a 6-year maturity. Its annual coupon rate is 7%...

A bond face value is $1000, with a 6-year maturity. Its annual coupon rate is 7% and issuer makes semi-annual coupon payments. The annual yield of maturity for the bond is 6%. The bond was issued on 7/1/2017. An investor bought it on 8/1/2019. Calculate its dirty price, accrued interests, and clean price.

A bond face value is $1000, with a 6-year maturity. Its annual coupon rate is 7% and issuer makes semi-annual coupon payments. The annual yield of maturity for the bond is 6%. The bond was issued on 7/1/2017. An investor bought it on 8/1/2019. Calculate its dirty price, accrued interests, and clean price.

a. An investor buys a 5 % annual coupon payment bond with three years to maturity....

a. An investor buys a 5 % annual coupon payment bond with three years to maturity. The bond has a yield-to-maturity of 9%. The par value is $1000. i. Determine the market price of the bond. (2 marks) ii. Calculate the bond's duration. (3 marks) b.A bond portfolio consists of the following three annual coupon payment bonds. Prices are per 100 of par value. Modified Duration Yield-to- Coupon (%) Bond Maturity Market (years) Price Maturity (%) (years) 5.23 7.98 Value...

a. An investor buys a 5 % annual coupon payment bond with three years to maturity. The bond has a yield-to-maturity of 9%. The par value is $1000. i. Determine the market price of the bond. (2 marks) ii. Calculate the bond's duration. (3 marks) b.A bond portfolio consists of the following three annual coupon payment bonds. Prices are per 100 of par value. Modified Duration Yield-to- Coupon (%) Bond Maturity Market (years) Price Maturity (%) (years) 5.23 7.98 Value...

Use the following information for problems 1, 2, 3, and 4: A non-callable $1,000 par- value...

Use the following information for problems 1, 2, 3, and 4: A non-callable $1,000 par- value bond matures in thirty years at par. The annual coupon rate is 5% with coupons payable annually. The bond was purchased at a price to yield an annual effective rate of 4%. 1. (1 point) Find the bond purchase price. 2. (1 point) Calculate the Macaulay duration and the modified duration for this bond. 3. (2 points) Suppose that the market interest rate increases...

Use the following information for problems 1, 2, 3, and 4: A non-callable $1,000 par- value bond matures in thirty years at par. The annual coupon rate is 5% with coupons payable annually. The bond was purchased at a price to yield an annual effective rate of 4%. 1. (1 point) Find the bond purchase price. 2. (1 point) Calculate the Macaulay duration and the modified duration for this bond. 3. (2 points) Suppose that the market interest rate increases...

An Apple annual coupon bond has a coupon rate of 5.1% face value of $1000, and...

An Apple annual coupon bond has a coupon rate of 5.1% face value of $1000, and 4 years to maturity. If its yield to maturity is 5.1%, what is its Macaulay duration? answer in years, rounded to three decimal places

4) Suppose there is a 3-year bond with a $1000 face value, 30% annual coupon payments...

4) Suppose there is a 3-year bond with a $1000 face value, 30% annual coupon payments and a 20% annual yield to maturity. a) Without any calculation, briefly explain whether this bond will be selling a premium or a discount b) Calculate the price of this bond. c Calculate the duration of this bond. d) Suppose the interest rates in the economy rise by 5 percentage points immediately after someone bought this bond. Show a calculation using duration for what...

4) Suppose there is a 3-year bond with a $1000 face value, 30% annual coupon payments and a 20% annual yield to maturity. a) Without any calculation, briefly explain whether this bond will be selling a premium or a discount b) Calculate the price of this bond. c Calculate the duration of this bond. d) Suppose the interest rates in the economy rise by 5 percentage points immediately after someone bought this bond. Show a calculation using duration for what...

4) Suppose there is a 3-year bond with a $1000 face value, 30% annual coupon payments...

4) Suppose there is a 3-year bond with a $1000 face value, 30% annual coupon payments and a 20% annual yield to maturity. a) Without any calculation, briefly explain whether this bond will be selling a premium or a discount. b) Calculate the price of this bond. c) Calculate the duration of this bond. d) Suppose the interest rates in the economy rise by 5 percentage points immediately after someone bought this bond. Show a calculation using duration for what...

A bond face value is $1000, with a 6-year maturity. Its annual coupon rate is 7% and issuer makes semi-annual coupon payments. The annual yield of maturity for the bond is 6%. The bond was issued on 7/1/2017. An investor bought it on 8/1/2019. Calculate its dirty price, accrued interests, and clean price.

A bond face value is $1000, with a 6-year maturity. Its annual coupon rate is 7% and issuer makes semi-annual coupon payments. The annual yield of maturity for the bond is 6%. The bond was issued on 7/1/2017. An investor bought it on 8/1/2019. Calculate its dirty price, accrued interests, and clean price.

a. An investor buys a 5 % annual coupon payment bond with three years to maturity. The bond has a yield-to-maturity of 9%. The par value is $1000. i. Determine the market price of the bond. (2 marks) ii. Calculate the bond's duration. (3 marks) b.A bond portfolio consists of the following three annual coupon payment bonds. Prices are per 100 of par value. Modified Duration Yield-to- Coupon (%) Bond Maturity Market (years) Price Maturity (%) (years) 5.23 7.98 Value...

a. An investor buys a 5 % annual coupon payment bond with three years to maturity. The bond has a yield-to-maturity of 9%. The par value is $1000. i. Determine the market price of the bond. (2 marks) ii. Calculate the bond's duration. (3 marks) b.A bond portfolio consists of the following three annual coupon payment bonds. Prices are per 100 of par value. Modified Duration Yield-to- Coupon (%) Bond Maturity Market (years) Price Maturity (%) (years) 5.23 7.98 Value...

Use the following information for problems 1, 2, 3, and 4: A non-callable $1,000 par- value bond matures in thirty years at par. The annual coupon rate is 5% with coupons payable annually. The bond was purchased at a price to yield an annual effective rate of 4%. 1. (1 point) Find the bond purchase price. 2. (1 point) Calculate the Macaulay duration and the modified duration for this bond. 3. (2 points) Suppose that the market interest rate increases...

Use the following information for problems 1, 2, 3, and 4: A non-callable $1,000 par- value bond matures in thirty years at par. The annual coupon rate is 5% with coupons payable annually. The bond was purchased at a price to yield an annual effective rate of 4%. 1. (1 point) Find the bond purchase price. 2. (1 point) Calculate the Macaulay duration and the modified duration for this bond. 3. (2 points) Suppose that the market interest rate increases...

4) Suppose there is a 3-year bond with a $1000 face value, 30% annual coupon payments and a 20% annual yield to maturity. a) Without any calculation, briefly explain whether this bond will be selling a premium or a discount b) Calculate the price of this bond. c Calculate the duration of this bond. d) Suppose the interest rates in the economy rise by 5 percentage points immediately after someone bought this bond. Show a calculation using duration for what...

4) Suppose there is a 3-year bond with a $1000 face value, 30% annual coupon payments and a 20% annual yield to maturity. a) Without any calculation, briefly explain whether this bond will be selling a premium or a discount b) Calculate the price of this bond. c Calculate the duration of this bond. d) Suppose the interest rates in the economy rise by 5 percentage points immediately after someone bought this bond. Show a calculation using duration for what...

Most questions answered within 3 hours.

-

3) What are the typical social structures in a global city?

asked 1 hour ago -

Luther Corporation

Consolidated Balance Sheet

December 31, 2019 and 2018 (in $ millions)

Assets

2019

2018...

asked 1 hour ago -

(Expected rate of return and risk) Carter Inc. is evaluating a

security. Calculate the investment’s expected...

asked 4 hours ago -

What specific indicators can point to lack of progress for

African Americans in American society?

asked 5 hours ago -

1-The Electrons in a beam are moving at 2.7×108 m/s in an

electric field of 15000...

asked 5 hours ago -

A gas tank is a vertical cylinder. It has a radius of 1m, a

height of...

asked 5 hours ago -

Accent Software faces the following conditions. All of these

support Accent’s use of a market-penetration pricing...

asked 6 hours ago -

A mathematically inclined friend emails you the following

instructions: "Meet me in the cafeteria the first...

asked 6 hours ago -

A monopoly sells in two countries . The demand curves in the two

countries are p1...

asked 7 hours ago -

A .15kg rubber ball is bounced off a wall. Before hitting the

wall, the ball moves...

asked 8 hours ago -

A manufacturing company preparing to build a new plant is

considering three potential locations for it....

asked 8 hours ago -

B. If compound Y has approximately the same values of solubility

in toluene as compound X,...

asked 9 hours ago