Homework Answers

Please find the solution in the below images

Add Answer to:

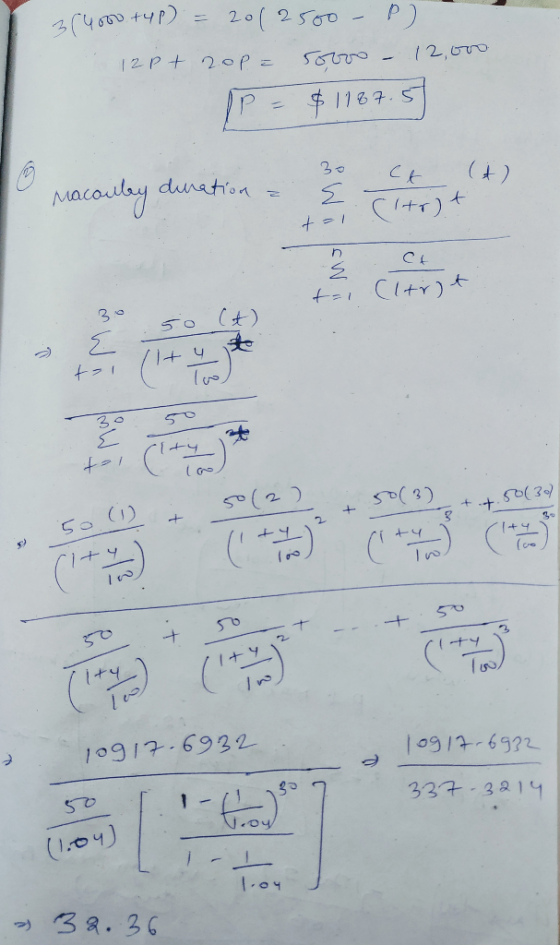

Use the following information for problems 1, 2, 3, and 4: A non-callable $1,000 par- value...

possible answers are 0.5%, 1%, 1.5%,2%,2.5% 25. A 15-year bond with annual coupons sold at par...

possible answers are 0.5%, 1%, 1.5%,2%,2.5%

25. A 15-year bond with annual coupons sold at par of 1,000 has a Macaulay duration of 9.0101. If the annual effective yield rate of the bond decreases by x, the price of the bond approximated using the first-order Macaulay approximation is 1,233.72. Calculate x.

possible answers are 0.5%, 1%, 1.5%,2%,2.5%

25. A 15-year bond with annual coupons sold at par of 1,000 has a Macaulay duration of 9.0101. If the annual effective yield rate of the bond decreases by x, the price of the bond approximated using the first-order Macaulay approximation is 1,233.72. Calculate x.

Sue buys a 10 year 1000 bond at par. The Macaulay duration is 8.329 years using...

Sue buys a 10 year 1000 bond at par. The Macaulay duration is 8.329 years using an annual effective interest rate of 6.8%. a. Calculate the estimated price of the bond, using the first-order modified approximation if the interest rate rises to 7%.

Sue buys a 10 year 1000 bond at par. The Macaulay duration is 8.329 years using an annual effective interest rate of 6.8%. a. Calculate the estimated price of the bond, using the first-order modified approximation if the interest rate rises to 7%.

1000 euro par value, 3% annual-coupon bond was issued 1.03.2015 and has 30 year maturity You...

1000 euro par value, 3% annual-coupon bond was issued 1.03.2015 and has 30 year maturity You purchased the bond on 20.10.2018 Market interest rate for similar securities is 2,8% Calculate following: a. Clean price b. Acrrued interest c. Full price d. Macaulay duration e. Modified duration If interest rate in the market declines by 50 bps g. Calculate new price with duration

1000 euro par value, 3% annual-coupon bond was issued 1.03.2015 and has 30 year maturity You purchased the bond on 20.10.2018 Market interest rate for similar securities is 2,8% Calculate following: a. Clean price b. Acrrued interest c. Full price d. Macaulay duration e. Modified duration If interest rate in the market declines by 50 bps g. Calculate new price with duration

1. Nov, 2005 #2. Calculate the Macaulay duration of an eight-year 100 par value bond with...

1. Nov, 2005 #2. Calculate the Macaulay duration of an eight-year 100 par value bond with 10% annual coupons and an effective rate of interest equal to 8%. (A) 4 (B) 5 (C) 6 (D) 7 (E) 8

1. Nov, 2005 #2. Calculate the Macaulay duration of an eight-year 100 par value bond with 10% annual coupons and an effective rate of interest equal to 8%. (A) 4 (B) 5 (C) 6 (D) 7 (E) 8

please answer the questions according to the marks appointed per question and sub question. this is...

please answer the questions according to the marks appointed per

question and sub question. this is a banking and finance question

so please answer it accordingly.

8. (a) Explain the concept of Macaulay duration and explain the relationship between Macaulay duration and: (i) bond maturity (ii) interest rates (iii) bond coupon rate (7 marks) (b) Calculate the price and Macaulay duration of a five-year 5% coupon bond where the market interest rate is 5%. Assume the par value of the...

please answer the questions according to the marks appointed per

question and sub question. this is a banking and finance question

so please answer it accordingly.

8. (a) Explain the concept of Macaulay duration and explain the relationship between Macaulay duration and: (i) bond maturity (ii) interest rates (iii) bond coupon rate (7 marks) (b) Calculate the price and Macaulay duration of a five-year 5% coupon bond where the market interest rate is 5%. Assume the par value of the...

Bond Analysis Issue data Purchase date Maturity date Par value Coupon rate Frequency Market price October...

Bond Analysis Issue data Purchase date Maturity date Par value Coupon rate Frequency Market price October 12,2002 September 26,2012 November 24,2019 2279 1.5100% annually 94% All values must be rounded up to 2 decimals Characteristics Value 1 Yield to maturity <> 2 Macaulay duration <> 3 Modified duration <> 4 If the yield-to-maturity increases by 100 bps,the bond price will be changed by (calculate it precisely) <> 5 If the yield-to- maturity increases by 10 bps, the bond price will...

Graph (show the cash flows) of the following bond: a. A $20,000 par value bond with...

Graph (show the cash flows) of the following bond: a. A $20,000 par value bond with a coupon of 4.0% paid semi-annually, maturing in 6 years. b. Find the current price of the Bond if you use 4.0% as the discount rate. c. Is this bond priced at a discount or a premium? Macaulay Duration: a. Calculate the price of a bond with a Face Value of $1,000, with an ANNUAL coupon of 10% (not paid semi-annually, but once a...

A $1,000 par value bond pays an annual coupon of 10.0% and matures in 4 years....

A $1,000 par value bond pays an annual coupon of 10.0% and matures in 4 years. If the bond sells to yield 7%, what is the modified duration of this bond? a) The regular duration is: b) The modified duration is:

Calculate the Macaulay duration of a 10%, $1,000 par bond that matures in three years if...

Calculate the Macaulay duration of a 10%, $1,000 par bond that

matures in three years if the bond's YTM is 12% and interest is

paid semiannually.

Calculate this bond's modified duration (years). Do not round

intermediate calculations. Round your answer to two decimal

places.

Assuming the bond's YTM goes from 12% to 10.5%, calculate an

estimate of the price change. Do not round intermediate

calculations. Round your answer to three decimal places (in %). Use

a minus sign to enter...

Calculate the Macaulay duration of a 10%, $1,000 par bond that

matures in three years if the bond's YTM is 12% and interest is

paid semiannually.

Calculate this bond's modified duration (years). Do not round

intermediate calculations. Round your answer to two decimal

places.

Assuming the bond's YTM goes from 12% to 10.5%, calculate an

estimate of the price change. Do not round intermediate

calculations. Round your answer to three decimal places (in %). Use

a minus sign to enter...

4) A 20 year, 4%, $1000 face value bond paying annual coupons is callable at par...

4) A 20 year, 4%, $1000 face value bond paying annual coupons is callable at par at the end of any year from 15 on. a) How much should an investor pay if they want to earn at least 6% until the bond is called (or matures). b) How much should an investor pay if they want to earn at least 3% until the bond is called (or matures).

possible answers are 0.5%, 1%, 1.5%,2%,2.5%

25. A 15-year bond with annual coupons sold at par of 1,000 has a Macaulay duration of 9.0101. If the annual effective yield rate of the bond decreases by x, the price of the bond approximated using the first-order Macaulay approximation is 1,233.72. Calculate x.

possible answers are 0.5%, 1%, 1.5%,2%,2.5%

25. A 15-year bond with annual coupons sold at par of 1,000 has a Macaulay duration of 9.0101. If the annual effective yield rate of the bond decreases by x, the price of the bond approximated using the first-order Macaulay approximation is 1,233.72. Calculate x.

Sue buys a 10 year 1000 bond at par. The Macaulay duration is 8.329 years using an annual effective interest rate of 6.8%. a. Calculate the estimated price of the bond, using the first-order modified approximation if the interest rate rises to 7%.

Sue buys a 10 year 1000 bond at par. The Macaulay duration is 8.329 years using an annual effective interest rate of 6.8%. a. Calculate the estimated price of the bond, using the first-order modified approximation if the interest rate rises to 7%.

1000 euro par value, 3% annual-coupon bond was issued 1.03.2015 and has 30 year maturity You purchased the bond on 20.10.2018 Market interest rate for similar securities is 2,8% Calculate following: a. Clean price b. Acrrued interest c. Full price d. Macaulay duration e. Modified duration If interest rate in the market declines by 50 bps g. Calculate new price with duration

1000 euro par value, 3% annual-coupon bond was issued 1.03.2015 and has 30 year maturity You purchased the bond on 20.10.2018 Market interest rate for similar securities is 2,8% Calculate following: a. Clean price b. Acrrued interest c. Full price d. Macaulay duration e. Modified duration If interest rate in the market declines by 50 bps g. Calculate new price with duration

1. Nov, 2005 #2. Calculate the Macaulay duration of an eight-year 100 par value bond with 10% annual coupons and an effective rate of interest equal to 8%. (A) 4 (B) 5 (C) 6 (D) 7 (E) 8

1. Nov, 2005 #2. Calculate the Macaulay duration of an eight-year 100 par value bond with 10% annual coupons and an effective rate of interest equal to 8%. (A) 4 (B) 5 (C) 6 (D) 7 (E) 8

please answer the questions according to the marks appointed per

question and sub question. this is a banking and finance question

so please answer it accordingly.

8. (a) Explain the concept of Macaulay duration and explain the relationship between Macaulay duration and: (i) bond maturity (ii) interest rates (iii) bond coupon rate (7 marks) (b) Calculate the price and Macaulay duration of a five-year 5% coupon bond where the market interest rate is 5%. Assume the par value of the...

please answer the questions according to the marks appointed per

question and sub question. this is a banking and finance question

so please answer it accordingly.

8. (a) Explain the concept of Macaulay duration and explain the relationship between Macaulay duration and: (i) bond maturity (ii) interest rates (iii) bond coupon rate (7 marks) (b) Calculate the price and Macaulay duration of a five-year 5% coupon bond where the market interest rate is 5%. Assume the par value of the...

Calculate the Macaulay duration of a 10%, $1,000 par bond that

matures in three years if the bond's YTM is 12% and interest is

paid semiannually.

Calculate this bond's modified duration (years). Do not round

intermediate calculations. Round your answer to two decimal

places.

Assuming the bond's YTM goes from 12% to 10.5%, calculate an

estimate of the price change. Do not round intermediate

calculations. Round your answer to three decimal places (in %). Use

a minus sign to enter...

Calculate the Macaulay duration of a 10%, $1,000 par bond that

matures in three years if the bond's YTM is 12% and interest is

paid semiannually.

Calculate this bond's modified duration (years). Do not round

intermediate calculations. Round your answer to two decimal

places.

Assuming the bond's YTM goes from 12% to 10.5%, calculate an

estimate of the price change. Do not round intermediate

calculations. Round your answer to three decimal places (in %). Use

a minus sign to enter...

Most questions answered within 3 hours.

-

Construction Cost Analysis and Estimating:

A project requires 17,000 allowed hours. Location of the work is...

asked 7 minutes ago -

1: In 802.11b, Access Point (AP) delivers a nonce to the Station

(STA). This nonce is...

asked 8 minutes ago -

calculate change in entropy and change in enthalpy for freezing

1 mol of water at -10C...

asked 14 minutes ago -

In your opinion, did anyone "win" the Cold War? If no, why? If

yes, who won...

asked 18 minutes ago -

a) Determine the saturation dissolved oxygen concentration at

sea-level at 1 atm and 20° C in...

asked 15 minutes ago -

Please complete the implementation of the four functions IN

C.

//************************************************************************************/

//

// countNumberofOnes

//

//...

asked 18 minutes ago -

Shown below are the budgeted sales for ABC Company for

the next six months:

Sales...

asked 22 minutes ago -

A balance sheet shows exactly where a business stands at any

given point in time. It...

asked 23 minutes ago -

For the reaction between ethylene and chlorine, the equilibrium

constant is 2.00x10^6. If the initial concentrations...

asked 31 minutes ago -

What is the energy released in this β+ nuclear reaction

23/12Mg→23/11Na+0/1e (The atomic mass of 23Mg...

asked 45 minutes ago -

Choose one:

Periodic Inventory Accounting is less expensive to maintain

than Perpetual Inventory Accounting

Periodic Inventory...

asked 43 minutes ago -

4. Describe the role played by glutamine in the transport of

nitrogen.

asked 41 minutes ago