Homework Answers

Add Answer to:

The following are estimates for two stocks. Firm-Specific Standard Deviation Stock A B Expected Return 108...

The following are estimates for two stocks. Stock Expected Return Beta Firm-Specific Standard Deviation A 10...

The following are estimates for two stocks. Stock Expected Return Beta Firm-Specific Standard Deviation A 10 % 0.70 28 % B 18 1.25 42 The market index has a standard deviation of 22% and the risk-free rate is 7%. a. What are the standard deviations of stocks A and B? (Do not round intermediate calculations. Round your answers to 2 decimal places.) b. Suppose that we were to construct a portfolio with proportions: Stock A 0.35 Stock B 0.35 T-bills...

The following are estimates for two stocks. Stock Expected Return Beta Firm-Specific Standard Deviation A 15%...

The following are estimates for two stocks. Stock Expected Return Beta Firm-Specific Standard Deviation A 15% 0.60 26% B 23 1.15 38 The market index has a standard deviation of 21% and the risk-free rate is 9%. a. What are the standard deviations of stocks A and B? (Do not round intermediate calculations. Enter your responses as decimal numbers rounded to 2 decimal places). Stock A Stock B b. Suppose that we were...

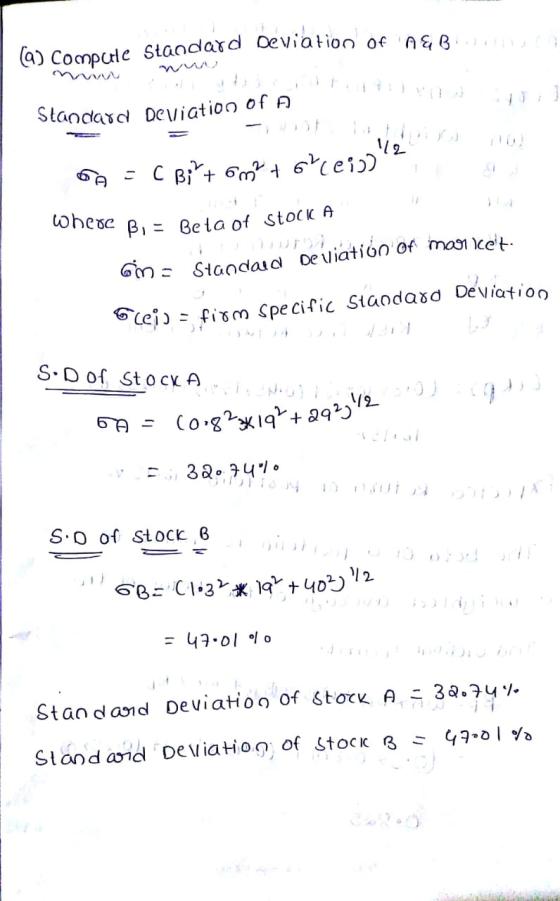

The following are estimates for two stocks. Firm-Specific Standard Deviation Expected Return 12% 18 Stock Beta...

The following are estimates for two stocks. Firm-Specific Standard Deviation Expected Return 12% 18 Stock Beta 0.85 1.40 The market index has a standard deviation of 22% and the risk-free rate is 11% a. What are the standard deviations of stocks A and B? (Do not round Intermediate calculations. Round your answers to 2 decimal places.) StockA Stock B b. Suppose that we were to construct a portfolio with proportions: Stock B Compute the expected return, standard deviation, beta, and...

The following are estimates for two stocks. Firm-Specific Standard Deviation Expected Return 12% 18 Stock Beta 0.85 1.40 The market index has a standard deviation of 22% and the risk-free rate is 11% a. What are the standard deviations of stocks A and B? (Do not round Intermediate calculations. Round your answers to 2 decimal places.) StockA Stock B b. Suppose that we were to construct a portfolio with proportions: Stock B Compute the expected return, standard deviation, beta, and...

Consider two stocks, Stock D, with an expected return of 20 percent and a standard deviation...

Consider two stocks, Stock D, with an expected return of 20 percent and a standard deviation of 36 percent, and Stock I, an international company, with an expected return of 6 percent and a standard deviation of 16 percent. The correlation between the two stocks is –0.01. What are the expected return and standard deviation of the minimum variance portfolio? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) Expected Return? Standard deviation?

4 Assume that you manage a risky portfolio with an expected rate of return of 20%...

4 Assume that you manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 42. The T-bill rate is 4% Your risky portfolio includes the following investments in the given proportions: points 268 Stock Stock Skipped Your client decides to invest in your risky portfolio a proportion (1) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected rate of...

4 Assume that you manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 42. The T-bill rate is 4% Your risky portfolio includes the following investments in the given proportions: points 268 Stock Stock Skipped Your client decides to invest in your risky portfolio a proportion (1) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected rate of...

Assume that you manage a risky portfolio with an expected rate of return of 17% and a standard deviation of 36%. The...

Assume that you manage a risky portfolio with an expected rate of return of 17% and a standard deviation of 36%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A 27 % Stock B 35 % Stock C 38 % Suppose that your client decides to invest in your portfolio a proportion y of the total investment budget so that the overall portfolio will have an expected rate...

here are two stocks in the market, Stock A and Stock B. The price of Stock...

here are two stocks in the market, Stock A and Stock B. The price of Stock A today is $78. The price of Stock A next year will be $67 if the economy is in a recession, $90 if the economy is normal, and $100 if the economy is expanding. The probabilities of recession, normal times, and expansion are .23, .57, and .20, respectively. Stock A pays no dividends and has a correlation of .73 with the market portfolio. Stock...

Check Assume that you manage a risky portfolio with an expected rate of return of 15%...

Check Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 31%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: 125 points Stock A Stock 8 Stock C Your client decides to invest in your risky portfolio a proportion of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected...

Check Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 31%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: 125 points Stock A Stock 8 Stock C Your client decides to invest in your risky portfolio a proportion of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected...

You manage a risky portfolio with an expected rate of return of 18% and a standard...

You manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 36%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock C 279 358 388 Suppose that your client decides to invest in your portfolio a proportion y of the total investment budget so that the overall portfolio will have an expected rate of return of 15%. a. What is the...

You manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 36%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock C 279 358 388 Suppose that your client decides to invest in your portfolio a proportion y of the total investment budget so that the overall portfolio will have an expected rate of return of 15%. a. What is the...

Assume that you manage a risky portfolio with an expected rate of return of 15% and...

Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 40%. The T-bill rate is 5%. Your risky portfolio includes the following investments in the given proportions: Stock A 24 % Stock B 33 Stock C 43 Your client decides to invest in your risky portfolio a proportion (y) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have...

The following are estimates for two stocks. Firm-Specific Standard Deviation Expected Return 12% 18 Stock Beta 0.85 1.40 The market index has a standard deviation of 22% and the risk-free rate is 11% a. What are the standard deviations of stocks A and B? (Do not round Intermediate calculations. Round your answers to 2 decimal places.) StockA Stock B b. Suppose that we were to construct a portfolio with proportions: Stock B Compute the expected return, standard deviation, beta, and...

The following are estimates for two stocks. Firm-Specific Standard Deviation Expected Return 12% 18 Stock Beta 0.85 1.40 The market index has a standard deviation of 22% and the risk-free rate is 11% a. What are the standard deviations of stocks A and B? (Do not round Intermediate calculations. Round your answers to 2 decimal places.) StockA Stock B b. Suppose that we were to construct a portfolio with proportions: Stock B Compute the expected return, standard deviation, beta, and...

4 Assume that you manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 42. The T-bill rate is 4% Your risky portfolio includes the following investments in the given proportions: points 268 Stock Stock Skipped Your client decides to invest in your risky portfolio a proportion (1) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected rate of...

4 Assume that you manage a risky portfolio with an expected rate of return of 20% and a standard deviation of 42. The T-bill rate is 4% Your risky portfolio includes the following investments in the given proportions: points 268 Stock Stock Skipped Your client decides to invest in your risky portfolio a proportion (1) of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected rate of...

Check Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 31%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: 125 points Stock A Stock 8 Stock C Your client decides to invest in your risky portfolio a proportion of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected...

Check Assume that you manage a risky portfolio with an expected rate of return of 15% and a standard deviation of 31%. The T-bill rate is 5% Your risky portfolio includes the following investments in the given proportions: 125 points Stock A Stock 8 Stock C Your client decides to invest in your risky portfolio a proportion of his total investment budget with the remainder in a T-bill money market fund so that his overall portfolio will have an expected...

You manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 36%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock C 279 358 388 Suppose that your client decides to invest in your portfolio a proportion y of the total investment budget so that the overall portfolio will have an expected rate of return of 15%. a. What is the...

You manage a risky portfolio with an expected rate of return of 18% and a standard deviation of 36%. The T-bill rate is 6%. Your risky portfolio includes the following investments in the given proportions: Stock A Stock B Stock C 279 358 388 Suppose that your client decides to invest in your portfolio a proportion y of the total investment budget so that the overall portfolio will have an expected rate of return of 15%. a. What is the...

Most questions answered within 3 hours.

-

A 8.15- g bullet from a 9-mm pistol has a velocity of 366.0 m/s.

It strikes...

asked 34 minutes ago -

The outstanding bonds of Alpha Extracts have a yield to maturity

of 7.4 percent and a...

asked 31 minutes ago -

The Problem: The Case of the Harmonizing Vacations

Your CEO is exploring partnering with a European...

asked 1 hour ago -

A chemical equation is balanced by adding coefficients in front

of some formulas so that the...

asked 1 hour ago -

From the literature (reference your sources): What are the

lattice parameters of calcite and aragonite? Why...

asked 2 hours ago -

Your system is rejecting the question am asking which is

preceded by a case study. It...

asked 2 hours ago -

3. On January 2, 2000, Larry creates a trust with himself as

trustee. Larry as trustee...

asked 2 hours ago -

A member of the volleyball team spikes the ball. During this

process, she changes the velocity...

asked 2 hours ago -

Are adult gamers less likely to use a gaming console (Xbox,

PlayStation, Wii, etc...) than teen...

asked 3 hours ago -

The University of

Texas recently reported that 43% of college students aged 18-24

would spend their...

asked 3 hours ago -

The length of stay at a specific emergency department in

Phoenix, Arizona, in 2009 had a...

asked 3 hours ago -

. Please give the mechanism for this type of problem. Step by

Step

The toxin that...

asked 3 hours ago