Assume a market index represents the common factor and all stocks in the economy have a...

Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 43%.

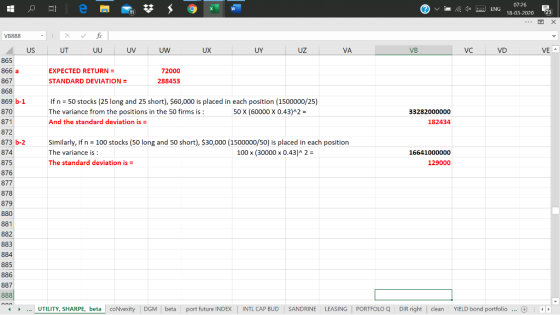

Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 2.4%, and one-half have an alpha of –2.4%. The analyst then buys $1.5 million of an equally weighted portfolio of the positive-alpha stocks and sells short $1.5 million of an equally weighted portfolio of the negative-alpha stocks.

a. What is the expected return (in dollars),

and what is the standard deviation of the analyst’s profit?

(Enter your answers in dollars not in millions.

Do not round intermediate calculations. Round your answers

to the nearest dollar amount.)

| Expected return | $ |

| Standard deviation | $ |

b-1. How does your answer change if the analyst examines 50 stocks instead of 20? (Enter your answer in dollars not in millions. Do not round intermediate calculations. Round your answer to the nearest dollar amount.)

Standard deviation $

b-2. How does your answer change if the analyst examines 100 stocks instead of 20? (Enter your answer in dollars not in millions.)

Standard deviation $

Homework Answers

SEE THE IMAGE. ANY DOUBTS, FEEL FREE TO ASK. THUMBS UP

PLEASE

Add Answer to:

Assume a market index represents the common factor and all

stocks in the economy have a...

Assume the return on a market index represents the common factor and all stocks in the...

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 47%. Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 4.5%, and one-half have an alpha of –4.5%. The analyst then buys $1.5 million of an equally weighted portfolio of the positive-alpha stocks and sells short $1.5 million of an equally weighted portfolio of the...

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-sp...

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 47%. Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 4.5%, and one-half have an alpha of –4.5%. The analyst then buys $1.5 million of an equally weighted portfolio of the positive-alpha stocks and sells short $1.5 million of an equally weighted portfolio of the...

Assume the return on a market index represents the common factor and all stocks in the...

Assume the return on a market index represents the common factor

and all stocks in the economy have a beta of 1. Firm-specific

returns all have a standard deviation of 50%.

Suppose an analyst studies 20 stocks and finds that one-half have

an alpha of 4.6%, and one-half have an alpha of –4.6%. The analyst

then buys $1.2 million of an equally weighted portfolio of the

positive-alpha stocks and sells short $1.2 million of an equally

weighted portfolio of the...

Assume the return on a market index represents the common factor

and all stocks in the economy have a beta of 1. Firm-specific

returns all have a standard deviation of 50%.

Suppose an analyst studies 20 stocks and finds that one-half have

an alpha of 4.6%, and one-half have an alpha of –4.6%. The analyst

then buys $1.2 million of an equally weighted portfolio of the

positive-alpha stocks and sells short $1.2 million of an equally

weighted portfolio of the...

Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 31%. Suppose an analyst studies 20 stocks and...

Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 31%. Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 2.0%, and one-half have an alpha of –2.0%. The analyst then buys $1.1 million of an equally weighted portfolio of the positive-alpha stocks and sells short $1.1 million of an equally weighted portfolio of the negative-alpha stocks. a....

Assume that stock market returns have the market index as a common factor, and that all...

Assume that stock market returns have the market index as a common factor, and that all stocks in the economy have a beta of 1.0 on the market index. Firm-specific returns all have a standard deviation of 22%. Suppose that an analyst studies 20 stocks and finds that one-half of them have an alpha of +1.5%, and the other half have an alpha of -1.5%. Suppose the analyst invests $1.0 million in an equally weighted portfolio of the positive alpha...

Assume that stock market returns have the market index as a common factor, and that all stocks in the economy have a beta of 1.0 on the market index. Firm-specific returns all have a standard deviation of 22%. Suppose that an analyst studies 20 stocks and finds that one-half of them have an alpha of +1.5%, and the other half have an alpha of -1.5%. Suppose the analyst invests $1.0 million in an equally weighted portfolio of the positive alpha...

Need a help with both parts pelase. I need help with b1 and b2. Thank you....

Need a help with both parts pelase.

I

need help with b1 and b2. Thank you.

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 47 % Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 45 %, and one-half have an alpha of-4.5 %. The analyst then buys $1.5 million of an equally...

Need a help with both parts pelase.

I

need help with b1 and b2. Thank you.

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 47 % Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 45 %, and one-half have an alpha of-4.5 %. The analyst then buys $1.5 million of an equally...

Instructions I help < Question 8 (of 10) Save & Ext Submit 10.00 points Assume a...

Instructions I help < Question 8 (of 10) Save & Ext Submit 10.00 points Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 38% Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 4.2%, and one-half have an alpha of -4,2%. The analyst then buys $10 million of an equally weighted portfolio of the positive-alpha stocks and...

Instructions I help < Question 8 (of 10) Save & Ext Submit 10.00 points Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 38% Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 4.2%, and one-half have an alpha of -4,2%. The analyst then buys $10 million of an equally weighted portfolio of the positive-alpha stocks and...

Q1. You are allocating money equally among 400 stocks. You believe: i. All stocks have the same...

Q1. You are allocating money equally among 400 stocks. You believe: i. All stocks have the same levels of standard deviation at 40%; ii. All stocks have the same pair-wise correlation a. What is the standard deviation of a portfolio of 400 equally weighted stocks if the correlation is 0.0? (1 point) b. What is the standard deviation of a portfolio of 400 equally weighted stocks if the correlation is 0.8? (1 point) c. If you observe from the option market that the implied volatility...

The following is part of the computer output from a regression of monthly returns on Waterworks...

The following is part of the computer output from a regression of monthly returns on Waterworks stock against the S&P 500 index. A hedge fund manager believes that Waterworks is underpriced, with an alpha of 2.3% over the coming month. Beta R-square Standard Deviation of Residuals 0.9 0.65 0.09 (i.e., 9% monthly) a. Suppose you hold an equally weighted portfolio of 100 stocks with the same alpha, beta, and residual standard deviation as Waterworks. Assume the residual returns on each...

In addition to price-weighted and value-weighted indexes, an equally weighted index is one in which the...

In addition to price-weighted and value-weighted indexes, an equally weighted index is one in which the index value is computed from the average rate of return of the stocks comprising the index. Equally weighted indexes are frequently used by financial researchers to measure portfolio performance. The following three defense stocks are to be combined into a stock index in January 2016 (perhaps a portfolio manager believes these stocks are an appropriate benchmark for his or her performance): Price Shares (millions)...

Assume the return on a market index represents the common factor

and all stocks in the economy have a beta of 1. Firm-specific

returns all have a standard deviation of 50%.

Suppose an analyst studies 20 stocks and finds that one-half have

an alpha of 4.6%, and one-half have an alpha of –4.6%. The analyst

then buys $1.2 million of an equally weighted portfolio of the

positive-alpha stocks and sells short $1.2 million of an equally

weighted portfolio of the...

Assume the return on a market index represents the common factor

and all stocks in the economy have a beta of 1. Firm-specific

returns all have a standard deviation of 50%.

Suppose an analyst studies 20 stocks and finds that one-half have

an alpha of 4.6%, and one-half have an alpha of –4.6%. The analyst

then buys $1.2 million of an equally weighted portfolio of the

positive-alpha stocks and sells short $1.2 million of an equally

weighted portfolio of the...

Assume that stock market returns have the market index as a common factor, and that all stocks in the economy have a beta of 1.0 on the market index. Firm-specific returns all have a standard deviation of 22%. Suppose that an analyst studies 20 stocks and finds that one-half of them have an alpha of +1.5%, and the other half have an alpha of -1.5%. Suppose the analyst invests $1.0 million in an equally weighted portfolio of the positive alpha...

Assume that stock market returns have the market index as a common factor, and that all stocks in the economy have a beta of 1.0 on the market index. Firm-specific returns all have a standard deviation of 22%. Suppose that an analyst studies 20 stocks and finds that one-half of them have an alpha of +1.5%, and the other half have an alpha of -1.5%. Suppose the analyst invests $1.0 million in an equally weighted portfolio of the positive alpha...

Need a help with both parts pelase.

I

need help with b1 and b2. Thank you.

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 47 % Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 45 %, and one-half have an alpha of-4.5 %. The analyst then buys $1.5 million of an equally...

Need a help with both parts pelase.

I

need help with b1 and b2. Thank you.

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 47 % Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 45 %, and one-half have an alpha of-4.5 %. The analyst then buys $1.5 million of an equally...

Instructions I help < Question 8 (of 10) Save & Ext Submit 10.00 points Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 38% Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 4.2%, and one-half have an alpha of -4,2%. The analyst then buys $10 million of an equally weighted portfolio of the positive-alpha stocks and...

Instructions I help < Question 8 (of 10) Save & Ext Submit 10.00 points Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 38% Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 4.2%, and one-half have an alpha of -4,2%. The analyst then buys $10 million of an equally weighted portfolio of the positive-alpha stocks and...

Most questions answered within 3 hours.

-

Using C++ :

A Pascals triangle row is constructed by looking at the previous

row and...

asked 8 seconds from now -

With what speed will the fastest photoelectrons be emitted from

a surface whose threshold wavelength is...

asked 26 seconds from now -

The following slope distances and differences in elevations

between the tape ends were recorded for a...

asked 1 minute ago -

1. Assuming random walk markets and normally distributed

returns, if a one day VaR on an...

asked 10 minutes ago -

(a) With a variable life insurance policy, the rate of return on

the investment (the death...

asked 20 minutes ago -

By applying what you know about Grignard reagents and the

mechanism by which benzoic acid is...

asked 44 minutes ago -

For thermoplastics, explain the effects of increasing of each of

the following properties on a polymer’s...

asked 45 minutes ago -

Make a menu for the user to use in python 3 that can search and

replace...

asked 36 minutes ago -

1) An aqueous solution contains 0.280 M

NaHS and 0.128 M

H2S.

The pH of this...

asked 51 minutes ago -

Situational Leadership

is based on interplay of all of the following except:

The amount of guidance...

asked 51 minutes ago -

Consider the following problem: given n positive integers,

separate them into two groups such that adding...

asked 55 minutes ago -

Briefly discuss the following statements:

2.1 A partner never has the right to claim compensation for...

asked 58 minutes ago