Assume the return on a market index represents the common factor

and all stocks in the economy have a beta of 1. Firm-specific

returns all have a standard deviation of 50%.

Suppose an analyst studies 20 stocks and finds that one-half have

an alpha of 4.6%, and one-half have an alpha of –4.6%. The analyst

then buys $1.2 million of an equally weighted portfolio of the

positive-alpha stocks and sells short $1.2 million of an equally

weighted portfolio of the negative-alpha stocks.

a. What is the expected return (in dollars), and

what is the standard deviation of the analyst’s profit?

(Enter your answers in dollars not in millions.

Do not round intermediate calculations. Round your answers

to the nearest dollar amount.)

Expected return:

Standard deviation:

b-1. How does your answer for standard deviation

change if the analyst examines 50 stocks instead of 20?

(Enter your answer in dollars not in millions. Do not round

intermediate calculations. Round your answer to the nearest dollar

amount.)

Standard deviation:

b-2. How does your answer for standard deviation

change if the analyst examines 100 stocks instead of 20?

(Enter your answer in dollars not in

millions.)

Standard deviation:

Homework Answers

SEE THE IMAGE. ANY DOUBTS, FEEL FREE TO ASK. THUMBS UP

PLEASE

Add Answer to:

Assume the return on a market index represents the common factor

and all stocks in the...

Assume the return on a market index represents the common factor and all stocks in the...

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 47%. Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 4.5%, and one-half have an alpha of –4.5%. The analyst then buys $1.5 million of an equally weighted portfolio of the positive-alpha stocks and sells short $1.5 million of an equally weighted portfolio of the...

Assume a market index represents the common factor and all stocks in the economy have a...

Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 43%. Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 2.4%, and one-half have an alpha of –2.4%. The analyst then buys $1.5 million of an equally weighted portfolio of the positive-alpha stocks and sells short $1.5 million of an equally weighted portfolio of the negative-alpha stocks. a....

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-sp...

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 47%. Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 4.5%, and one-half have an alpha of –4.5%. The analyst then buys $1.5 million of an equally weighted portfolio of the positive-alpha stocks and sells short $1.5 million of an equally weighted portfolio of the...

Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 31%. Suppose an analyst studies 20 stocks and...

Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 31%. Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 2.0%, and one-half have an alpha of –2.0%. The analyst then buys $1.1 million of an equally weighted portfolio of the positive-alpha stocks and sells short $1.1 million of an equally weighted portfolio of the negative-alpha stocks. a....

Assume that stock market returns have the market index as a common factor, and that all...

Assume that stock market returns have the market index as a common factor, and that all stocks in the economy have a beta of 1.0 on the market index. Firm-specific returns all have a standard deviation of 22%. Suppose that an analyst studies 20 stocks and finds that one-half of them have an alpha of +1.5%, and the other half have an alpha of -1.5%. Suppose the analyst invests $1.0 million in an equally weighted portfolio of the positive alpha...

Assume that stock market returns have the market index as a common factor, and that all stocks in the economy have a beta of 1.0 on the market index. Firm-specific returns all have a standard deviation of 22%. Suppose that an analyst studies 20 stocks and finds that one-half of them have an alpha of +1.5%, and the other half have an alpha of -1.5%. Suppose the analyst invests $1.0 million in an equally weighted portfolio of the positive alpha...

Need a help with both parts pelase. I need help with b1 and b2. Thank you....

Need a help with both parts pelase.

I

need help with b1 and b2. Thank you.

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 47 % Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 45 %, and one-half have an alpha of-4.5 %. The analyst then buys $1.5 million of an equally...

Need a help with both parts pelase.

I

need help with b1 and b2. Thank you.

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 47 % Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 45 %, and one-half have an alpha of-4.5 %. The analyst then buys $1.5 million of an equally...

Instructions I help < Question 8 (of 10) Save & Ext Submit 10.00 points Assume a...

Instructions I help < Question 8 (of 10) Save & Ext Submit 10.00 points Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 38% Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 4.2%, and one-half have an alpha of -4,2%. The analyst then buys $10 million of an equally weighted portfolio of the positive-alpha stocks and...

Instructions I help < Question 8 (of 10) Save & Ext Submit 10.00 points Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 38% Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 4.2%, and one-half have an alpha of -4,2%. The analyst then buys $10 million of an equally weighted portfolio of the positive-alpha stocks and...

Consider two stocks, Stock D, with an expected return of 20 percent and a standard deviation...

Consider two stocks, Stock D, with an expected return of 20 percent and a standard deviation of 36 percent, and Stock I, an international company, with an expected return of 6 percent and a standard deviation of 16 percent. The correlation between the two stocks is –0.01. What are the expected return and standard deviation of the minimum variance portfolio? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) Expected Return? Standard deviation?

Suppose that the index model for stocks A and B is estimated from excess returns with...

Suppose that the index model for stocks A and B is

estimated from excess returns with the following results:

RA = 2.5% + 0.95RM + eA

RB = –1.8% + 1.10RM + eB

σM = 27%; R-squareA = 0.23; R-squareB = 0.11

Assume you create a portfolio Q, with investment proportions of

0.50 in a risky portfolio P, 0.30 in the market index, and 0.20 in

T-bill. Portfolio P is composed of 60% Stock A and 40% Stock B.

a....

Suppose that the index model for stocks A and B is

estimated from excess returns with the following results:

RA = 2.5% + 0.95RM + eA

RB = –1.8% + 1.10RM + eB

σM = 27%; R-squareA = 0.23; R-squareB = 0.11

Assume you create a portfolio Q, with investment proportions of

0.50 in a risky portfolio P, 0.30 in the market index, and 0.20 in

T-bill. Portfolio P is composed of 60% Stock A and 40% Stock B.

a....

A.) Calculate the expected return for the two stocks (Do not round intermediate calculations; enter your...

A.) Calculate the expected

return for the two stocks (Do not round intermediate calculations;

enter your answers as a percent rounded to 2 decimal places).

B.) Calculate the standard deviation for the two stocks (Do not

round intermediate calculations; enter your answers as a percent

rounded to 2 decimal places).

Consider the following information: Probability of Rate of Return if State Occurs State of Economy Stock A Stock B .030 -.39 .59 110 .17 .280 .52 Economy Recession Normal Boom...

A.) Calculate the expected

return for the two stocks (Do not round intermediate calculations;

enter your answers as a percent rounded to 2 decimal places).

B.) Calculate the standard deviation for the two stocks (Do not

round intermediate calculations; enter your answers as a percent

rounded to 2 decimal places).

Consider the following information: Probability of Rate of Return if State Occurs State of Economy Stock A Stock B .030 -.39 .59 110 .17 .280 .52 Economy Recession Normal Boom...

Assume that stock market returns have the market index as a common factor, and that all stocks in the economy have a beta of 1.0 on the market index. Firm-specific returns all have a standard deviation of 22%. Suppose that an analyst studies 20 stocks and finds that one-half of them have an alpha of +1.5%, and the other half have an alpha of -1.5%. Suppose the analyst invests $1.0 million in an equally weighted portfolio of the positive alpha...

Assume that stock market returns have the market index as a common factor, and that all stocks in the economy have a beta of 1.0 on the market index. Firm-specific returns all have a standard deviation of 22%. Suppose that an analyst studies 20 stocks and finds that one-half of them have an alpha of +1.5%, and the other half have an alpha of -1.5%. Suppose the analyst invests $1.0 million in an equally weighted portfolio of the positive alpha...

Need a help with both parts pelase.

I

need help with b1 and b2. Thank you.

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 47 % Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 45 %, and one-half have an alpha of-4.5 %. The analyst then buys $1.5 million of an equally...

Need a help with both parts pelase.

I

need help with b1 and b2. Thank you.

Assume the return on a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 47 % Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 45 %, and one-half have an alpha of-4.5 %. The analyst then buys $1.5 million of an equally...

Instructions I help < Question 8 (of 10) Save & Ext Submit 10.00 points Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 38% Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 4.2%, and one-half have an alpha of -4,2%. The analyst then buys $10 million of an equally weighted portfolio of the positive-alpha stocks and...

Instructions I help < Question 8 (of 10) Save & Ext Submit 10.00 points Assume a market index represents the common factor and all stocks in the economy have a beta of 1. Firm-specific returns all have a standard deviation of 38% Suppose an analyst studies 20 stocks and finds that one-half have an alpha of 4.2%, and one-half have an alpha of -4,2%. The analyst then buys $10 million of an equally weighted portfolio of the positive-alpha stocks and...

Suppose that the index model for stocks A and B is

estimated from excess returns with the following results:

RA = 2.5% + 0.95RM + eA

RB = –1.8% + 1.10RM + eB

σM = 27%; R-squareA = 0.23; R-squareB = 0.11

Assume you create a portfolio Q, with investment proportions of

0.50 in a risky portfolio P, 0.30 in the market index, and 0.20 in

T-bill. Portfolio P is composed of 60% Stock A and 40% Stock B.

a....

Suppose that the index model for stocks A and B is

estimated from excess returns with the following results:

RA = 2.5% + 0.95RM + eA

RB = –1.8% + 1.10RM + eB

σM = 27%; R-squareA = 0.23; R-squareB = 0.11

Assume you create a portfolio Q, with investment proportions of

0.50 in a risky portfolio P, 0.30 in the market index, and 0.20 in

T-bill. Portfolio P is composed of 60% Stock A and 40% Stock B.

a....

A.) Calculate the expected

return for the two stocks (Do not round intermediate calculations;

enter your answers as a percent rounded to 2 decimal places).

B.) Calculate the standard deviation for the two stocks (Do not

round intermediate calculations; enter your answers as a percent

rounded to 2 decimal places).

Consider the following information: Probability of Rate of Return if State Occurs State of Economy Stock A Stock B .030 -.39 .59 110 .17 .280 .52 Economy Recession Normal Boom...

A.) Calculate the expected

return for the two stocks (Do not round intermediate calculations;

enter your answers as a percent rounded to 2 decimal places).

B.) Calculate the standard deviation for the two stocks (Do not

round intermediate calculations; enter your answers as a percent

rounded to 2 decimal places).

Consider the following information: Probability of Rate of Return if State Occurs State of Economy Stock A Stock B .030 -.39 .59 110 .17 .280 .52 Economy Recession Normal Boom...

Most questions answered within 3 hours.

-

Consider the following problem: given n positive integers,

separate them into two groups such that adding...

asked 14 seconds ago -

Briefly discuss the following statements:

2.1 A partner never has the right to claim compensation for...

asked 2 minutes ago -

If a bond has an annual probability of default of 6%, 10% and

12% in years...

asked 11 minutes ago -

Let X be normally distributed with mean μ = 10 and standard

deviation σ = 6....

asked 16 minutes ago -

You're examining some of the tiny printing on one of the newer

twenty-dollar bills. A 1.5...

asked 20 minutes ago -

Discuss several common sources of secondary data coming from

government sources.

asked 23 minutes ago -

This is a basic java program where you convert units using only

loops, control statements and...

asked 23 minutes ago -

A sample survey at a supermarket showed that 204 of 300 shoppers

regularly use cents-off coupons....

asked 1 hour ago -

1. Find the area under the standard normal curve that lies

outside the interval between z=...

asked 40 minutes ago -

In ________ mode, the interpreter reads the contents of a file

that contains Python statements and...

asked 56 minutes ago -

1.

The second-order rate constant for self-reaction of hydroxyl

radicals

2 OH → H2O + O...

asked 46 minutes ago -

What is the most important factor leading to improved resource

efficiency over the long run?

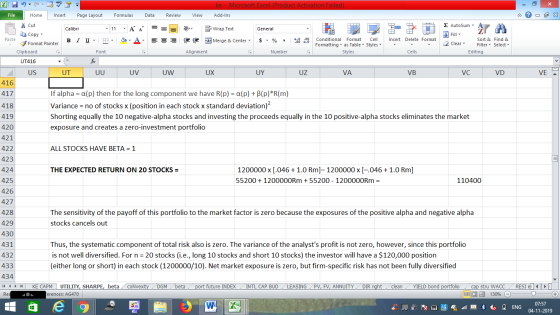

asked 42 minutes ago