Homework Answers

For graph, we should look at two characteristics to identify the correct answer - first, price of bond C is higher than price of bond Z when years to maturity is 4. And second, when the bond matures, both bonds have $1000 as price, which implies the bond prices should coincide in graph.

So, these characteristics match with graph A

Add Answer to:

X Module 4 Homework An investor has two bonds in her portfolo, Bond C and Bond...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.3%. Bond C pays a 11.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.3% over the next 4 years, calculate the price of the bonds at each of the following years to maturity....

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.3%. Bond C pays a 11.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.3% over the next 4 years, calculate the price of the bonds at each of the following years to maturity....

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.8%. Bond C pays a 10% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.8% over the next 4 years, calculate the price of the bonds at each of the following years to maturity....

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.8%. Bond C pays a 10% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.8% over the next 4 years, calculate the price of the bonds at each of the following years to maturity....

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 9.1%. Bond C pays a 11.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 9.1% over the next 4 years, calculate the price of the bonds at each of the following years to maturity....

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 9.1%. Bond C pays a 11.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 9.1% over the next 4 years, calculate the price of the bonds at each of the following years to maturity....

BOND VALUATION An investor has two bonds in her portfolio, Bond C and Bond Z. Each...

BOND VALUATION An investor has two bonds in her portfolio, Bond

C and Bond Z. Each

bond matures in 4 years, has a face value of $1,000, and has a

yield to maturity of 9 6%.

Bond C pays a 10% annual coupon, while Bond Z is a zero coupon

bond.

a. Assuming that the yield to maturity of each bond remains at 9 6%

over the next 4

years, calculate the price of the bonds at each of the...

BOND VALUATION An investor has two bonds in her portfolio, Bond

C and Bond Z. Each

bond matures in 4 years, has a face value of $1,000, and has a

yield to maturity of 9 6%.

Bond C pays a 10% annual coupon, while Bond Z is a zero coupon

bond.

a. Assuming that the yield to maturity of each bond remains at 9 6%

over the next 4

years, calculate the price of the bonds at each of the...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 9.4%. Bond C pays a 10% annual coupon, while Bond Z is a zero coupon bond. Assuming that the yield to maturity of each bond remains at 9.4% over the next 4 years, calculate the price of the bonds at each of the following years to maturity. Round...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.2%. Bond C pays a 12% annual coupon, while Bond Z is a zero coupon bond. Assuming that the yield to maturity of each bond remains at 8.2% over the next 4 years, calculate the price of the bonds at each of the following years to maturity. Round...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 9.5%. Bond C pays a 12.5% annual coupon, while Bond Z is a zero coupon bond. Assuming that the yield to maturity of each bond remains at 9.5% over the next 4 years, calculate the price of the bonds at each of the following years to maturity. Round...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 9.2%. Bond C pays a 11.5% annual coupon, while Bond Z is a zero coupon bond. Assuming that the yield to maturity of each bond remains at 9.2% over the next 4 years, calculate the price of the bonds at each of the following years to maturity. Round...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures...

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.4%. Bond C pays a 10.5% annual coupon, while Bond Z is a zero coupon bond. Assuming that the yield to maturity of each bond remains at 8.4% over the next 4 years, calculate the price of the bonds at each of the following years to maturity. Round...

q 5 An investor has two bonds in her portfolio, Bond C and Bond Z. Each...

q 5

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.1%. Bond C pays a 10.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.1% over the next 4 years, calculate the price of the bonds at each of the following years...

q 5

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.1%. Bond C pays a 10.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.1% over the next 4 years, calculate the price of the bonds at each of the following years...

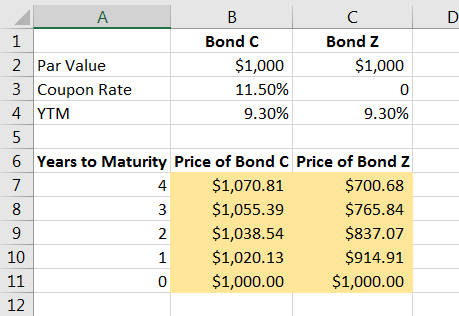

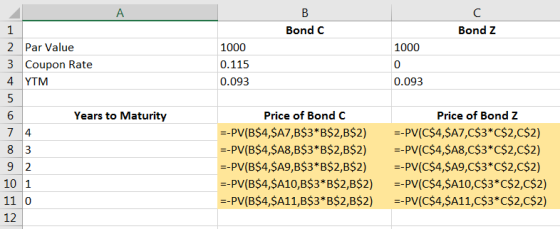

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.3%. Bond C pays a 11.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.3% over the next 4 years, calculate the price of the bonds at each of the following years to maturity....

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.3%. Bond C pays a 11.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.3% over the next 4 years, calculate the price of the bonds at each of the following years to maturity....

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.8%. Bond C pays a 10% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.8% over the next 4 years, calculate the price of the bonds at each of the following years to maturity....

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.8%. Bond C pays a 10% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.8% over the next 4 years, calculate the price of the bonds at each of the following years to maturity....

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 9.1%. Bond C pays a 11.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 9.1% over the next 4 years, calculate the price of the bonds at each of the following years to maturity....

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 9.1%. Bond C pays a 11.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 9.1% over the next 4 years, calculate the price of the bonds at each of the following years to maturity....

BOND VALUATION An investor has two bonds in her portfolio, Bond

C and Bond Z. Each

bond matures in 4 years, has a face value of $1,000, and has a

yield to maturity of 9 6%.

Bond C pays a 10% annual coupon, while Bond Z is a zero coupon

bond.

a. Assuming that the yield to maturity of each bond remains at 9 6%

over the next 4

years, calculate the price of the bonds at each of the...

BOND VALUATION An investor has two bonds in her portfolio, Bond

C and Bond Z. Each

bond matures in 4 years, has a face value of $1,000, and has a

yield to maturity of 9 6%.

Bond C pays a 10% annual coupon, while Bond Z is a zero coupon

bond.

a. Assuming that the yield to maturity of each bond remains at 9 6%

over the next 4

years, calculate the price of the bonds at each of the...

q 5

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.1%. Bond C pays a 10.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.1% over the next 4 years, calculate the price of the bonds at each of the following years...

q 5

An investor has two bonds in her portfolio, Bond C and Bond Z. Each bond matures in 4 years, has a face value of $1,000, and has a yield to maturity of 8.1%. Bond C pays a 10.5% annual coupon, while Bond Z is a zero coupon bond. a. Assuming that the yield to maturity of each bond remains at 8.1% over the next 4 years, calculate the price of the bonds at each of the following years...

Most questions answered within 3 hours.

-

MATLAB HW 11 problem using Switch Case and Input commands

Write a script file that calculates...

asked 24 seconds from now -

A college student is employed as a door-to-door newspaper

salesman. Historical data suggests that the student...

asked 14 minutes ago -

Considering gravitational time dilation, calculate the time that

passes in Earth’s surface while 1 hour passes...

asked 38 minutes ago -

Minitab Problem: Take the Lake Hume June rainfall data and find

use the processes outlined in...

asked 1 hour ago -

X Company is trying to decide whether to continue using old

equipment to make Product A...

asked 1 hour ago -

IN PYTHON ONLY !! Program 2: Re-work

program #5 (WeeklyHours) from the previous assignment such that...

asked 2 hours ago -

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 3 hours ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 5 hours ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 4 hours ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 5 hours ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 5 hours ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 5 hours ago