Homework Answers

Add Answer to:

1. Consider the following unobserved effects regression model: Suppose that the idiosyncratic error u, t 1,..,T...

1.Idiosyncratic error is the error that occurs due to _____. a. unobserved factors that affect the...

1.Idiosyncratic error is the error that occurs due to _____. a. unobserved factors that affect the dependent variable and change over time b. unobserved factors that affect the dependent variable and do not change over time c. incorrect measurement of an economic variable d. correlation between the independent variables 2.Which of the following is a reason for using independently pooled cross sections? a. To increase the sample size b. To select a sample based on the dependent variable c. To...

which of the following is correct, when we have pure serial correlation in a regression? 12...

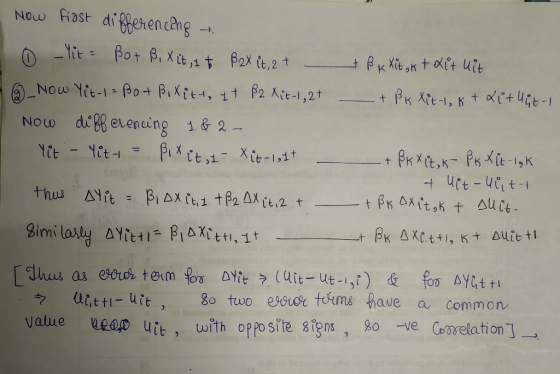

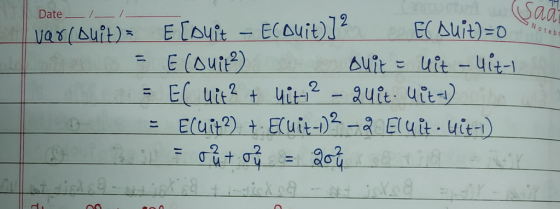

which of the following is correct, when we have pure serial correlation in a regression? 12 Multiple Choice ) we can use first differencing model only if the serial correlation is first order. 0 the error terms of the first differnced model are not serially correlated. ) if the first differenced method is applied correctly, the coefficients of the regression are unbiased and efficient O All of the above choices are correct

which of the following is correct, when we have pure serial correlation in a regression? 12 Multiple Choice ) we can use first differencing model only if the serial correlation is first order. 0 the error terms of the first differnced model are not serially correlated. ) if the first differenced method is applied correctly, the coefficients of the regression are unbiased and efficient O All of the above choices are correct

Q3. [10 points [Serial Correlation Consider a simple linear regression model with time series dat...

Q3. [10 points [Serial Correlation Consider a simple linear regression model with time series data: Suppose the error ut is strictly exogenous. That is Moreover, the error term follows an AR(1) serial correlation model. That where et are uncorrelated, and have a zero mean and constant variance a. 2 points Will the OLS estimator of P be unbiased? Why or why not? b. [3 points Will the conventional estimator of the variance of the OLS estimator be unbiased? Why or...

Q3. [10 points [Serial Correlation Consider a simple linear regression model with time series data: Suppose the error ut is strictly exogenous. That is Moreover, the error term follows an AR(1) serial correlation model. That where et are uncorrelated, and have a zero mean and constant variance a. 2 points Will the OLS estimator of P be unbiased? Why or why not? b. [3 points Will the conventional estimator of the variance of the OLS estimator be unbiased? Why or...

Simple linear regression model Assumptions: AI E[u] 0 for all i, i1, .., n On average,...

Simple linear regression model Assumptions: AI E[u] 0 for all i, i1, .., n On average, random component is zero Model runs through expected values of Yand Y A2 E[uaij]-0 for all i and j where i /j COV(IIİlh)- Unobserved component not related across observations E[14"]= for all i All observations have random component dravn from a distribution with the same variance σ2 , f(0,02) A3 var(11i)-σ (Homoskedasticitv) A4 E[Alli] = 0 for all i Random component and covariate not...

Simple linear regression model Assumptions: AI E[u] 0 for all i, i1, .., n On average, random component is zero Model runs through expected values of Yand Y A2 E[uaij]-0 for all i and j where i /j COV(IIİlh)- Unobserved component not related across observations E[14"]= for all i All observations have random component dravn from a distribution with the same variance σ2 , f(0,02) A3 var(11i)-σ (Homoskedasticitv) A4 E[Alli] = 0 for all i Random component and covariate not...

Consider the following regression: uneme = Bo + B infe + Bzinft-1 + Bsyear + u...

Consider the following regression: uneme = Bo + B infe + Bzinft-1 + Bsyear + u where unem is the civilian unemployment rate and inf is the CPI inflation rate. Assume ut = put,itet with p70. Answer the following questions. 1. What is serial correlation? Explain. 2. Write the transformed model that is estimated by GLS. 3. Outline the intuition behind the BG test for serial correlation. 4. If = P19-1 + P2U-2+ et, the GLS model described in class...

Consider the following regression: uneme = Bo + B infe + Bzinft-1 + Bsyear + u where unem is the civilian unemployment rate and inf is the CPI inflation rate. Assume ut = put,itet with p70. Answer the following questions. 1. What is serial correlation? Explain. 2. Write the transformed model that is estimated by GLS. 3. Outline the intuition behind the BG test for serial correlation. 4. If = P19-1 + P2U-2+ et, the GLS model described in class...

Suppose the true regression model is 1 of 3 Now, consider the following advice: "When the...

Suppose the true regression model is 1 of 3 Now, consider the following advice: "When the explanatory variables X2 and X, are correlated, the variance of b, is larger than it would be if X, and X, were uncorrelated. Thus, if you are interested in ß2, it is best to leave X, out of the regression if it is correlated with X." What do you think of this advice?

Suppose the true regression model is 1 of 3 Now, consider the following advice: "When the explanatory variables X2 and X, are correlated, the variance of b, is larger than it would be if X, and X, were uncorrelated. Thus, if you are interested in ß2, it is best to leave X, out of the regression if it is correlated with X." What do you think of this advice?

Consider the following simple regression model: a. Suppose that OLS assumptions 1 to 4 hold true. We know that homoskedasticity assumption is statedas: Var[UjIx] = σ2 for all i Now, suppose that...

Consider the following simple regression model: a. Suppose that OLS assumptions 1 to 4 hold true. We know that homoskedasticity assumption is statedas: Var[UjIx] = σ2 for all i Now, suppose that homoskedasticity does not hold. Mathematically, this is expressed as In other words, the subscript i in σ12 means that the conditional variance of errors for each individual i is different. Under heteroskedasticity, we can derive the expression for the variance of Var(B) as SST Where SSTx is the...

Consider the following simple regression model: a. Suppose that OLS assumptions 1 to 4 hold true. We know that homoskedasticity assumption is statedas: Var[UjIx] = σ2 for all i Now, suppose that homoskedasticity does not hold. Mathematically, this is expressed as In other words, the subscript i in σ12 means that the conditional variance of errors for each individual i is different. Under heteroskedasticity, we can derive the expression for the variance of Var(B) as SST Where SSTx is the...

1. Consider the following simple regression model: y = β0 + β1x1 + u (1) and...

1. Consider the following simple regression model: y = β0 + β1x1 + u (1) and the following multiple regression model: y = β0 + β1x1 + β2x2 + u (2), where x1 is the variable of primary interest to explain y. Which of the following statements is correct? a. When drawing ceteris paribus conclusions about how x1 affects y, with model (1), we must assume that x2, and all other factors contained in u, are uncorrelated with x1. b....

1. In the simple regression model y = + β1x + u, suppose that E (u)...

1. In the simple regression model y = + β1x + u, suppose that E (u) 0. Letting oo-E(u), show that the model can always be rewrit ten with the same slope, but a new intercept and error, where the new error has a zero expected value 2. The data set BWGHT contains data on births to women in the United States. Two variables of interest are the dependent variable, nfan birth weight in ounces (bught), and an explanatory variable,...

1. In the simple regression model y = + β1x + u, suppose that E (u) 0. Letting oo-E(u), show that the model can always be rewrit ten with the same slope, but a new intercept and error, where the new error has a zero expected value 2. The data set BWGHT contains data on births to women in the United States. Two variables of interest are the dependent variable, nfan birth weight in ounces (bught), and an explanatory variable,...

which of the following is correct, when we have pure serial correlation in a regression? 12 Multiple Choice ) we can use first differencing model only if the serial correlation is first order. 0 the error terms of the first differnced model are not serially correlated. ) if the first differenced method is applied correctly, the coefficients of the regression are unbiased and efficient O All of the above choices are correct

which of the following is correct, when we have pure serial correlation in a regression? 12 Multiple Choice ) we can use first differencing model only if the serial correlation is first order. 0 the error terms of the first differnced model are not serially correlated. ) if the first differenced method is applied correctly, the coefficients of the regression are unbiased and efficient O All of the above choices are correct

Q3. [10 points [Serial Correlation Consider a simple linear regression model with time series data: Suppose the error ut is strictly exogenous. That is Moreover, the error term follows an AR(1) serial correlation model. That where et are uncorrelated, and have a zero mean and constant variance a. 2 points Will the OLS estimator of P be unbiased? Why or why not? b. [3 points Will the conventional estimator of the variance of the OLS estimator be unbiased? Why or...

Q3. [10 points [Serial Correlation Consider a simple linear regression model with time series data: Suppose the error ut is strictly exogenous. That is Moreover, the error term follows an AR(1) serial correlation model. That where et are uncorrelated, and have a zero mean and constant variance a. 2 points Will the OLS estimator of P be unbiased? Why or why not? b. [3 points Will the conventional estimator of the variance of the OLS estimator be unbiased? Why or...

Simple linear regression model Assumptions: AI E[u] 0 for all i, i1, .., n On average, random component is zero Model runs through expected values of Yand Y A2 E[uaij]-0 for all i and j where i /j COV(IIİlh)- Unobserved component not related across observations E[14"]= for all i All observations have random component dravn from a distribution with the same variance σ2 , f(0,02) A3 var(11i)-σ (Homoskedasticitv) A4 E[Alli] = 0 for all i Random component and covariate not...

Simple linear regression model Assumptions: AI E[u] 0 for all i, i1, .., n On average, random component is zero Model runs through expected values of Yand Y A2 E[uaij]-0 for all i and j where i /j COV(IIİlh)- Unobserved component not related across observations E[14"]= for all i All observations have random component dravn from a distribution with the same variance σ2 , f(0,02) A3 var(11i)-σ (Homoskedasticitv) A4 E[Alli] = 0 for all i Random component and covariate not...

Consider the following regression: uneme = Bo + B infe + Bzinft-1 + Bsyear + u where unem is the civilian unemployment rate and inf is the CPI inflation rate. Assume ut = put,itet with p70. Answer the following questions. 1. What is serial correlation? Explain. 2. Write the transformed model that is estimated by GLS. 3. Outline the intuition behind the BG test for serial correlation. 4. If = P19-1 + P2U-2+ et, the GLS model described in class...

Consider the following regression: uneme = Bo + B infe + Bzinft-1 + Bsyear + u where unem is the civilian unemployment rate and inf is the CPI inflation rate. Assume ut = put,itet with p70. Answer the following questions. 1. What is serial correlation? Explain. 2. Write the transformed model that is estimated by GLS. 3. Outline the intuition behind the BG test for serial correlation. 4. If = P19-1 + P2U-2+ et, the GLS model described in class...

Suppose the true regression model is 1 of 3 Now, consider the following advice: "When the explanatory variables X2 and X, are correlated, the variance of b, is larger than it would be if X, and X, were uncorrelated. Thus, if you are interested in ß2, it is best to leave X, out of the regression if it is correlated with X." What do you think of this advice?

Suppose the true regression model is 1 of 3 Now, consider the following advice: "When the explanatory variables X2 and X, are correlated, the variance of b, is larger than it would be if X, and X, were uncorrelated. Thus, if you are interested in ß2, it is best to leave X, out of the regression if it is correlated with X." What do you think of this advice?

Consider the following simple regression model: a. Suppose that OLS assumptions 1 to 4 hold true. We know that homoskedasticity assumption is statedas: Var[UjIx] = σ2 for all i Now, suppose that homoskedasticity does not hold. Mathematically, this is expressed as In other words, the subscript i in σ12 means that the conditional variance of errors for each individual i is different. Under heteroskedasticity, we can derive the expression for the variance of Var(B) as SST Where SSTx is the...

Consider the following simple regression model: a. Suppose that OLS assumptions 1 to 4 hold true. We know that homoskedasticity assumption is statedas: Var[UjIx] = σ2 for all i Now, suppose that homoskedasticity does not hold. Mathematically, this is expressed as In other words, the subscript i in σ12 means that the conditional variance of errors for each individual i is different. Under heteroskedasticity, we can derive the expression for the variance of Var(B) as SST Where SSTx is the...

1. In the simple regression model y = + β1x + u, suppose that E (u) 0. Letting oo-E(u), show that the model can always be rewrit ten with the same slope, but a new intercept and error, where the new error has a zero expected value 2. The data set BWGHT contains data on births to women in the United States. Two variables of interest are the dependent variable, nfan birth weight in ounces (bught), and an explanatory variable,...

1. In the simple regression model y = + β1x + u, suppose that E (u) 0. Letting oo-E(u), show that the model can always be rewrit ten with the same slope, but a new intercept and error, where the new error has a zero expected value 2. The data set BWGHT contains data on births to women in the United States. Two variables of interest are the dependent variable, nfan birth weight in ounces (bught), and an explanatory variable,...

Most questions answered within 3 hours.

-

An MNE is this kind of industry when competition in one country

is essentially independent of...

asked 53 minutes ago -

. For this set of questions, determine what

proportion of a normal distribution is located betweeneach...

asked 1 hour ago -

A college student is employed as a door-to-door newspaper

salesman. Historical data suggests that the student...

asked 2 hours ago -

MATLAB HW 11 problem using Switch Case and Input commands

Write a script file that calculates...

asked 2 hours ago -

Considering gravitational time dilation, calculate the time that

passes in Earth’s surface while 1 hour passes...

asked 2 hours ago -

Minitab Problem: Take the Lake Hume June rainfall data and find

use the processes outlined in...

asked 3 hours ago -

X Company is trying to decide whether to continue using old

equipment to make Product A...

asked 3 hours ago -

IN PYTHON ONLY !! Program 2: Re-work

program #5 (WeeklyHours) from the previous assignment such that...

asked 4 hours ago -

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 5 hours ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 7 hours ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 7 hours ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 7 hours ago