Homework Answers

Please refer to below spreadsheet for calculation and answer. Cell reference also provided.

Cell reference -

Hope this will help, please do comment if you need any further explanation. Your feedback would be highly appreciated.

Add Answer to:

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

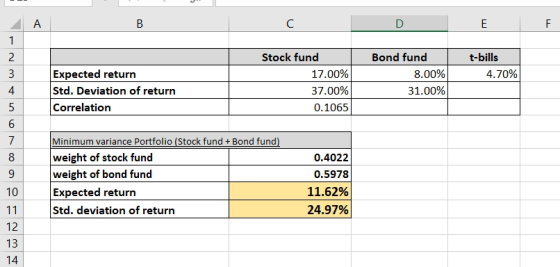

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.7%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 17% 37% Bond fund (B) 8% 31% The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that vields a sure rate of 4.7%. The probability distributions of the risky funds are: Expected Return 170 Stock fund (S) Bond fund (B) Standard Deviation 370 313 The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that vields a sure rate of 4.7%. The probability distributions of the risky funds are: Expected Return 170 Stock fund (S) Bond fund (B) Standard Deviation 370 313 The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Standard Deviation Stock fund (5) Bond fund (B) Expected Return 15% 9% The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Standard Deviation Stock fund (5) Bond fund (B) Expected Return 15% 9% The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 15% 9% Standard Deviation 32% 23% The correlation between the fund returns is .15. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 15% 9% Standard Deviation 32% 23% The correlation between the fund returns is .15. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.2%. The probability distributions of the risky funds are: Expected Return 13% 6% Standard Deviation 42% 36% Stock fund (S) Bond fund (B) The correlation between the fund returns is .0222. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.2%. The probability distributions of the risky funds are: Expected Return 13% 6% Standard Deviation 42% 36% Stock fund (S) Bond fund (B) The correlation between the fund returns is .0222. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.6%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 17% 46% Bond fund (B) 8% 40% The correlation between the fund returns is 0.0600. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.4%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 14% 34% Bond fund (B) 5% 28% The correlation between the fund returns is 0.0214. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 3.0%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 12% 41% Bond fund (B) 5% 30% The correlation between the fund returns is 0.0667. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.4%. The probability distributions of the risky funds are: Expected Return Std. Deviation Stock fund (S) 15% 44% Bond fund (B) 8% 38% The correlation between the fund returns is .0684. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.4%. The probability distributions of the risky funds are: Standard Deviation Expected Return 14% - 5% Stock fund (S) Bond fund (B) 34% 28% The correlation between the fund returns is 0.0214. What is the expected return and standard deviation...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.4%. The probability distributions of the risky funds are: Standard Deviation Expected Return 14% - 5% Stock fund (S) Bond fund (B) 34% 28% The correlation between the fund returns is 0.0214. What is the expected return and standard deviation...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that vields a sure rate of 4.7%. The probability distributions of the risky funds are: Expected Return 170 Stock fund (S) Bond fund (B) Standard Deviation 370 313 The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that vields a sure rate of 4.7%. The probability distributions of the risky funds are: Expected Return 170 Stock fund (S) Bond fund (B) Standard Deviation 370 313 The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Standard Deviation Stock fund (5) Bond fund (B) Expected Return 15% 9% The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Standard Deviation Stock fund (5) Bond fund (B) Expected Return 15% 9% The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 15% 9% Standard Deviation 32% 23% The correlation between the fund returns is .15. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 15% 9% Standard Deviation 32% 23% The correlation between the fund returns is .15. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.2%. The probability distributions of the risky funds are: Expected Return 13% 6% Standard Deviation 42% 36% Stock fund (S) Bond fund (B) The correlation between the fund returns is .0222. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.2%. The probability distributions of the risky funds are: Expected Return 13% 6% Standard Deviation 42% 36% Stock fund (S) Bond fund (B) The correlation between the fund returns is .0222. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.4%. The probability distributions of the risky funds are: Standard Deviation Expected Return 14% - 5% Stock fund (S) Bond fund (B) 34% 28% The correlation between the fund returns is 0.0214. What is the expected return and standard deviation...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.4%. The probability distributions of the risky funds are: Standard Deviation Expected Return 14% - 5% Stock fund (S) Bond fund (B) 34% 28% The correlation between the fund returns is 0.0214. What is the expected return and standard deviation...

Most questions answered within 3 hours.

-

(Expected rate of return and risk) Carter Inc. is evaluating a

security. Calculate the investment’s expected...

asked 2 hours ago -

What specific indicators can point to lack of progress for

African Americans in American society?

asked 3 hours ago -

1-The Electrons in a beam are moving at 2.7×108 m/s in an

electric field of 15000...

asked 3 hours ago -

A gas tank is a vertical cylinder. It has a radius of 1m, a

height of...

asked 4 hours ago -

Accent Software faces the following conditions. All of these

support Accent’s use of a market-penetration pricing...

asked 5 hours ago -

A mathematically inclined friend emails you the following

instructions: "Meet me in the cafeteria the first...

asked 5 hours ago -

A monopoly sells in two countries . The demand curves in the two

countries are p1...

asked 6 hours ago -

A .15kg rubber ball is bounced off a wall. Before hitting the

wall, the ball moves...

asked 6 hours ago -

A manufacturing company preparing to build a new plant is

considering three potential locations for it....

asked 6 hours ago -

B. If compound Y has approximately the same values of solubility

in toluene as compound X,...

asked 7 hours ago -

Oscar Inc. has inventory in Japan valued at 39,051,000 Yen one

year ago. One year ago...

asked 7 hours ago -

If Canada suffered from "fundamental disequilibrium," and its

government choose not to devalue its currency, a...

asked 7 hours ago