Homework Answers

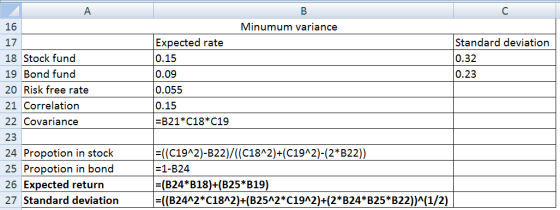

Calculate the minimum variance portfolio as follows:

Formulas:

Add Answer to:

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Standard Deviation Stock fund (5) Bond fund (B) Expected Return 15% 9% The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Standard Deviation Stock fund (5) Bond fund (B) Expected Return 15% 9% The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum...

Poforlio and fund management Question A pension fund manager is considering three mutual funds. The first...

Poforlio and fund management

Question A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return|Standard Deviation Stock fund (S) 15% 32% Bond fund (B) 23 9 The correlation between the fund returns is .15. Tabulate and draw the investment...

Poforlio and fund management

Question A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return|Standard Deviation Stock fund (S) 15% 32% Bond fund (B) 23 9 The correlation between the fund returns is .15. Tabulate and draw the investment...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.4%. The probability distributions of the risky funds are: Expected Return Std. Deviation Stock fund (S) 15% 44% Bond fund (B) 8% 38% The correlation between the fund returns is .0684. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long- term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return 15% Stock fund (5) Bond fund (B) Standard Deviation 32% 23% 9% The correlation between the fund returns is 0.15. a. What would be the investment proportions of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long- term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return 15% Stock fund (5) Bond fund (B) Standard Deviation 32% 23% 9% The correlation between the fund returns is 0.15. a. What would be the investment proportions of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 47%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund 373 (5) Bond fund (8) 31% The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 47%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund 373 (5) Bond fund (8) 31% The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.2%. The probability distributions of the risky funds are: Expected Return 13% 6% Standard Deviation 42% 36% Stock fund (S) Bond fund (B) The correlation between the fund returns is .0222. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.2%. The probability distributions of the risky funds are: Expected Return 13% 6% Standard Deviation 42% 36% Stock fund (S) Bond fund (B) The correlation between the fund returns is .0222. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.6%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 17% 46% Bond fund (B) 8% 40% The correlation between the fund returns is 0.0600. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.7%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 17% 37% Bond fund (B) 8% 31% The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.4%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 14% 34% Bond fund (B) 5% 28% The correlation between the fund returns is 0.0214. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 3.0%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 12% 41% Bond fund (B) 5% 30% The correlation between the fund returns is 0.0667. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Standard Deviation Stock fund (5) Bond fund (B) Expected Return 15% 9% The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Standard Deviation Stock fund (5) Bond fund (B) Expected Return 15% 9% The correlation between the fund returns is 15. What is the expected return and standard deviation for the minimum...

Poforlio and fund management

Question A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return|Standard Deviation Stock fund (S) 15% 32% Bond fund (B) 23 9 The correlation between the fund returns is .15. Tabulate and draw the investment...

Poforlio and fund management

Question A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return|Standard Deviation Stock fund (S) 15% 32% Bond fund (B) 23 9 The correlation between the fund returns is .15. Tabulate and draw the investment...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long- term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return 15% Stock fund (5) Bond fund (B) Standard Deviation 32% 23% 9% The correlation between the fund returns is 0.15. a. What would be the investment proportions of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long- term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.5%. The probability distributions of the risky funds are: Expected Return 15% Stock fund (5) Bond fund (B) Standard Deviation 32% 23% 9% The correlation between the fund returns is 0.15. a. What would be the investment proportions of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 47%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund 373 (5) Bond fund (8) 31% The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 47%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund 373 (5) Bond fund (8) 31% The correlation between the fund returns is 0.1065. What is the expected return and standard deviation for the minimum...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.2%. The probability distributions of the risky funds are: Expected Return 13% 6% Standard Deviation 42% 36% Stock fund (S) Bond fund (B) The correlation between the fund returns is .0222. What is the expected return and standard deviation for...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.2%. The probability distributions of the risky funds are: Expected Return 13% 6% Standard Deviation 42% 36% Stock fund (S) Bond fund (B) The correlation between the fund returns is .0222. What is the expected return and standard deviation for...

Most questions answered within 3 hours.

-

(Expected rate of return and risk) Carter Inc. is evaluating a

security. Calculate the investment’s expected...

asked 1 hour ago -

What specific indicators can point to lack of progress for

African Americans in American society?

asked 2 hours ago -

1-The Electrons in a beam are moving at 2.7×108 m/s in an

electric field of 15000...

asked 2 hours ago -

A gas tank is a vertical cylinder. It has a radius of 1m, a

height of...

asked 2 hours ago -

Accent Software faces the following conditions. All of these

support Accent’s use of a market-penetration pricing...

asked 3 hours ago -

A mathematically inclined friend emails you the following

instructions: "Meet me in the cafeteria the first...

asked 3 hours ago -

A monopoly sells in two countries . The demand curves in the two

countries are p1...

asked 4 hours ago -

A .15kg rubber ball is bounced off a wall. Before hitting the

wall, the ball moves...

asked 5 hours ago -

A manufacturing company preparing to build a new plant is

considering three potential locations for it....

asked 5 hours ago -

B. If compound Y has approximately the same values of solubility

in toluene as compound X,...

asked 6 hours ago -

Oscar Inc. has inventory in Japan valued at 39,051,000 Yen one

year ago. One year ago...

asked 6 hours ago -

If Canada suffered from "fundamental disequilibrium," and its

government choose not to devalue its currency, a...

asked 6 hours ago