A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 5.9%. The probability distributions of

the risky funds are:

| Expected Return | Standard Deviation | |||

| Stock fund (S) | 20 | % | 49 | % |

| Bond fund (B) | 9 | % | 43 | % |

The correlation between the fund returns is .0721.

Suppose now that your portfolio must yield an expected return of

18% and be efficient, that is, on the best feasible CAL.

a. What is the standard deviation of your

portfolio? (Do not round intermediate calculations. Round

your answer to 2 decimal places.)

Standard deviation

%

b-1. What is the proportion invested in the T-bill fund? (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Proportion invested in the T-bill fund

%

b-2. What is the proportion invested in each of

the two risky funds? (Do not round intermediate

calculations. Round your answers to 2 decimal places.)

| Proportion Invested | |

| Stocks | % |

| Bonds | % |

Homework Answers

SEE THE IMAGE. ANY DOUBTS, FEEL FREE TO ASK. THUMBS UP

PLEASE

Add Answer to:

A pension fund manager is considering three mutual funds. The

first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.9%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 20% 9% Standard Deviation 49% 43% The correlation between the fund returns is .0721. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.9%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 20% 9% Standard Deviation 49% 43% The correlation between the fund returns is .0721. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.1%. The probability distributions of the risky funds are: Expected Return 11% Stock fund (S) Bond fund (B) Standard Deviation 33% 25% 8% The correlation between the fund returns is 1560. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.1%. The probability distributions of the risky funds are: Expected Return 11% Stock fund (S) Bond fund (B) Standard Deviation 33% 25% 8% The correlation between the fund returns is 1560. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return 10% Standard Deviation 39% Stock fund (S) Bond fund (B) 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return 10% Standard Deviation 39% Stock fund (S) Bond fund (B) 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.8%. The probability distributions of the risky funds are: Expected Return 18% Standard Deviation Stock fund (S) Bond fund (B) 38% 98 32% The correlation between the fund returns is .1313. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.8%. The probability distributions of the risky funds are: Expected Return 18% Standard Deviation Stock fund (S) Bond fund (B) 38% 98 32% The correlation between the fund returns is .1313. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) Bond fund (B) 39% 10% 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) Bond fund (B) 39% 10% 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 4.8%. The probability distributions of

the risky funds are:

Expected Return

Standard Deviation

Stock fund (S)

18

%

38

%

Bond fund (B)

9

%

32

%

The correlation between the fund returns is .1313.

Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 4.8%. The probability distributions of

the risky funds are:

Expected Return

Standard Deviation

Stock fund (S)

18

%

38

%

Bond fund (B)

9

%

32

%

The correlation between the fund returns is .1313.

Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.3%. The probability distributions of the risky funds are Expected Return Standard Deviation Stock fund (S) Bond fund (8) 14% 43% 7% 37% The correlation between the fund returns is 0459 Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.3%. The probability distributions of the risky funds are Expected Return Standard Deviation Stock fund (S) Bond fund (8) 14% 43% 7% 37% The correlation between the fund returns is 0459 Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 3.0%. The probability distributions of the risky funds are Expected Return 12% Stock fund (S) Bond fund (B) Standard Deviation 41% 30% 5% The correlation between the fund returns is .0667. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 3.0%. The probability distributions of the risky funds are Expected Return 12% Stock fund (S) Bond fund (B) Standard Deviation 41% 30% 5% The correlation between the fund returns is .0667. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-teerm government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.8 %. The probability distributions of the risky funds are: standard Deviation Expected Return 191 98 Stock fund (8) Bond fund (B) 488 42 The correlation between the fund returns is .0762. Suppose now that your portfolio must yleld an...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-teerm government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.8 %. The probability distributions of the risky funds are: standard Deviation Expected Return 191 98 Stock fund (8) Bond fund (B) 488 42 The correlation between the fund returns is .0762. Suppose now that your portfolio must yleld an...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.5%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 15 % 35 % Bond fund (B) 6 % 29 % The correlation between the fund returns is .0517. Suppose now that your portfolio...

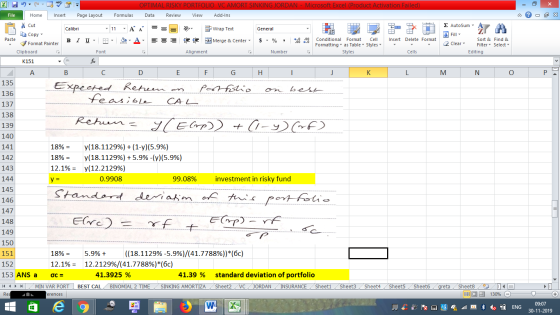

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.9%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 20% 9% Standard Deviation 49% 43% The correlation between the fund returns is .0721. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.9%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 20% 9% Standard Deviation 49% 43% The correlation between the fund returns is .0721. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.1%. The probability distributions of the risky funds are: Expected Return 11% Stock fund (S) Bond fund (B) Standard Deviation 33% 25% 8% The correlation between the fund returns is 1560. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.1%. The probability distributions of the risky funds are: Expected Return 11% Stock fund (S) Bond fund (B) Standard Deviation 33% 25% 8% The correlation between the fund returns is 1560. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return 10% Standard Deviation 39% Stock fund (S) Bond fund (B) 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return 10% Standard Deviation 39% Stock fund (S) Bond fund (B) 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.8%. The probability distributions of the risky funds are: Expected Return 18% Standard Deviation Stock fund (S) Bond fund (B) 38% 98 32% The correlation between the fund returns is .1313. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.8%. The probability distributions of the risky funds are: Expected Return 18% Standard Deviation Stock fund (S) Bond fund (B) 38% 98 32% The correlation between the fund returns is .1313. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) Bond fund (B) 39% 10% 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) Bond fund (B) 39% 10% 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 4.8%. The probability distributions of

the risky funds are:

Expected Return

Standard Deviation

Stock fund (S)

18

%

38

%

Bond fund (B)

9

%

32

%

The correlation between the fund returns is .1313.

Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 4.8%. The probability distributions of

the risky funds are:

Expected Return

Standard Deviation

Stock fund (S)

18

%

38

%

Bond fund (B)

9

%

32

%

The correlation between the fund returns is .1313.

Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.3%. The probability distributions of the risky funds are Expected Return Standard Deviation Stock fund (S) Bond fund (8) 14% 43% 7% 37% The correlation between the fund returns is 0459 Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.3%. The probability distributions of the risky funds are Expected Return Standard Deviation Stock fund (S) Bond fund (8) 14% 43% 7% 37% The correlation between the fund returns is 0459 Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 3.0%. The probability distributions of the risky funds are Expected Return 12% Stock fund (S) Bond fund (B) Standard Deviation 41% 30% 5% The correlation between the fund returns is .0667. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 3.0%. The probability distributions of the risky funds are Expected Return 12% Stock fund (S) Bond fund (B) Standard Deviation 41% 30% 5% The correlation between the fund returns is .0667. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-teerm government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.8 %. The probability distributions of the risky funds are: standard Deviation Expected Return 191 98 Stock fund (8) Bond fund (B) 488 42 The correlation between the fund returns is .0762. Suppose now that your portfolio must yleld an...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-teerm government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.8 %. The probability distributions of the risky funds are: standard Deviation Expected Return 191 98 Stock fund (8) Bond fund (B) 488 42 The correlation between the fund returns is .0762. Suppose now that your portfolio must yleld an...

Most questions answered within 3 hours.

-

The free energy change for the following reaction at 25 °C, when

[Sn2+] = 1.17 M...

asked 1 hour ago -

An MNE is this kind of industry when competition in one country

is essentially independent of...

asked 2 hours ago -

. For this set of questions, determine what

proportion of a normal distribution is located betweeneach...

asked 3 hours ago -

A college student is employed as a door-to-door newspaper

salesman. Historical data suggests that the student...

asked 4 hours ago -

MATLAB HW 11 problem using Switch Case and Input commands

Write a script file that calculates...

asked 3 hours ago -

Considering gravitational time dilation, calculate the time that

passes in Earth’s surface while 1 hour passes...

asked 4 hours ago -

Minitab Problem: Take the Lake Hume June rainfall data and find

use the processes outlined in...

asked 5 hours ago -

X Company is trying to decide whether to continue using old

equipment to make Product A...

asked 5 hours ago -

IN PYTHON ONLY !! Program 2: Re-work

program #5 (WeeklyHours) from the previous assignment such that...

asked 5 hours ago -

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 7 hours ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 8 hours ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 8 hours ago