Homework Answers

First we need to calculate the weight of stock in the optimal portfolio

Weight of the bond is 1-weight of stock = 1-0.75 = 0.25

Portfolio Expected return is calcualted by solving the following equation:

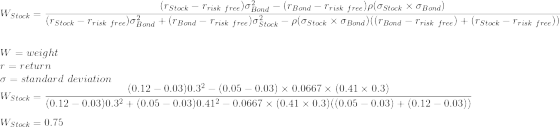

Portfolio standard deviation is calculated by solving the following

equation:

This is the calculation only of the risky portfolio.

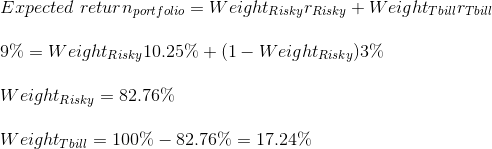

Now we need to calculate the proportion of a portfolio comprising the risky portfolio and the T bill to get a return of 9% Once we know the weights, we can calculate the standard deviation of this portfolio

Portfolio Expected return is calcualted by solving the following equation:

As tbill is not risky it has a stadard deviation of 0 so the portfolio stadard deviation is as follows:

So the answer to the first question is 26.59%

Proportions of bond and stock in this portfolio are as follows:

| Asset | Weight | Portfolio weight | Final weight |

| Stock | 75.00% | 82.76% | 0.8276 x 75 = 62.07% |

| Bond | 25.00% | 82.76% | 0.8276 x 25 = 20.69% |

Add Answer to:

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term governmen...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 3.0%. The probability distributions of

the risky funds are:

Expected Return

Standard Deviation

Stock fund (S)

12

%

41

%

Bond fund (B)

5

%

30

%

The correlation between the fund returns is .0667.

Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 3.0%. The probability distributions of

the risky funds are:

Expected Return

Standard Deviation

Stock fund (S)

12

%

41

%

Bond fund (B)

5

%

30

%

The correlation between the fund returns is .0667.

Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.1%. The probability distributions of the risky funds are: Expected Return 11% Stock fund (S) Bond fund (B) Standard Deviation 33% 25% 8% The correlation between the fund returns is 1560. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.1%. The probability distributions of the risky funds are: Expected Return 11% Stock fund (S) Bond fund (B) Standard Deviation 33% 25% 8% The correlation between the fund returns is 1560. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return 10% Standard Deviation 39% Stock fund (S) Bond fund (B) 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return 10% Standard Deviation 39% Stock fund (S) Bond fund (B) 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.8%. The probability distributions of the risky funds are: Expected Return 18% Standard Deviation Stock fund (S) Bond fund (B) 38% 98 32% The correlation between the fund returns is .1313. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.8%. The probability distributions of the risky funds are: Expected Return 18% Standard Deviation Stock fund (S) Bond fund (B) 38% 98 32% The correlation between the fund returns is .1313. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.9%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) 20 % 49 % Bond fund (B) 9 % 43 % The correlation between the fund returns is .0721. Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) Bond fund (B) 39% 10% 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) Bond fund (B) 39% 10% 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.9%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 20% 9% Standard Deviation 49% 43% The correlation between the fund returns is .0721. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.9%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 20% 9% Standard Deviation 49% 43% The correlation between the fund returns is .0721. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 4.8%. The probability distributions of

the risky funds are:

Expected Return

Standard Deviation

Stock fund (S)

18

%

38

%

Bond fund (B)

9

%

32

%

The correlation between the fund returns is .1313.

Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 4.8%. The probability distributions of

the risky funds are:

Expected Return

Standard Deviation

Stock fund (S)

18

%

38

%

Bond fund (B)

9

%

32

%

The correlation between the fund returns is .1313.

Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.3%. The probability distributions of the risky funds are Expected Return Standard Deviation Stock fund (S) Bond fund (8) 14% 43% 7% 37% The correlation between the fund returns is 0459 Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.3%. The probability distributions of the risky funds are Expected Return Standard Deviation Stock fund (S) Bond fund (8) 14% 43% 7% 37% The correlation between the fund returns is 0459 Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-teerm government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.8 %. The probability distributions of the risky funds are: standard Deviation Expected Return 191 98 Stock fund (8) Bond fund (B) 488 42 The correlation between the fund returns is .0762. Suppose now that your portfolio must yleld an...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-teerm government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.8 %. The probability distributions of the risky funds are: standard Deviation Expected Return 191 98 Stock fund (8) Bond fund (B) 488 42 The correlation between the fund returns is .0762. Suppose now that your portfolio must yleld an...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 3.0%. The probability distributions of

the risky funds are:

Expected Return

Standard Deviation

Stock fund (S)

12

%

41

%

Bond fund (B)

5

%

30

%

The correlation between the fund returns is .0667.

Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 3.0%. The probability distributions of

the risky funds are:

Expected Return

Standard Deviation

Stock fund (S)

12

%

41

%

Bond fund (B)

5

%

30

%

The correlation between the fund returns is .0667.

Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.1%. The probability distributions of the risky funds are: Expected Return 11% Stock fund (S) Bond fund (B) Standard Deviation 33% 25% 8% The correlation between the fund returns is 1560. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.1%. The probability distributions of the risky funds are: Expected Return 11% Stock fund (S) Bond fund (B) Standard Deviation 33% 25% 8% The correlation between the fund returns is 1560. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return 10% Standard Deviation 39% Stock fund (S) Bond fund (B) 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return 10% Standard Deviation 39% Stock fund (S) Bond fund (B) 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.8%. The probability distributions of the risky funds are: Expected Return 18% Standard Deviation Stock fund (S) Bond fund (B) 38% 98 32% The correlation between the fund returns is .1313. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.8%. The probability distributions of the risky funds are: Expected Return 18% Standard Deviation Stock fund (S) Bond fund (B) 38% 98 32% The correlation between the fund returns is .1313. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) Bond fund (B) 39% 10% 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.9%. The probability distributions of the risky funds are: Expected Return Standard Deviation Stock fund (S) Bond fund (B) 39% 10% 5% 33% The correlation between the fund returns is .0030. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.9%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 20% 9% Standard Deviation 49% 43% The correlation between the fund returns is .0721. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.9%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Expected Return 20% 9% Standard Deviation 49% 43% The correlation between the fund returns is .0721. Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 4.8%. The probability distributions of

the risky funds are:

Expected Return

Standard Deviation

Stock fund (S)

18

%

38

%

Bond fund (B)

9

%

32

%

The correlation between the fund returns is .1313.

Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The

first is a stock fund, the second is a long-term government and

corporate bond fund, and the third is a T-bill money market fund

that yields a sure rate of 4.8%. The probability distributions of

the risky funds are:

Expected Return

Standard Deviation

Stock fund (S)

18

%

38

%

Bond fund (B)

9

%

32

%

The correlation between the fund returns is .1313.

Suppose now that your portfolio...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.3%. The probability distributions of the risky funds are Expected Return Standard Deviation Stock fund (S) Bond fund (8) 14% 43% 7% 37% The correlation between the fund returns is 0459 Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.3%. The probability distributions of the risky funds are Expected Return Standard Deviation Stock fund (S) Bond fund (8) 14% 43% 7% 37% The correlation between the fund returns is 0459 Suppose now that your portfolio must yield an expected...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-teerm government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.8 %. The probability distributions of the risky funds are: standard Deviation Expected Return 191 98 Stock fund (8) Bond fund (B) 488 42 The correlation between the fund returns is .0762. Suppose now that your portfolio must yleld an...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-teerm government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 5.8 %. The probability distributions of the risky funds are: standard Deviation Expected Return 191 98 Stock fund (8) Bond fund (B) 488 42 The correlation between the fund returns is .0762. Suppose now that your portfolio must yleld an...

Most questions answered within 3 hours.

-

The Bahraini public budget experiences deficit in the last

seven years, what are procedures are taken...

asked 1 minute ago -

You invested $30,000 in a mutual fund at the beginning of the

year when the NAV...

asked 5 minutes ago -

Would you expect the price elasticity of supply for guitars to

be more inelastic in the...

asked 7 minutes ago -

A snowmobile is originally at the point with position vector

30.1 m at 95.0° counterclockwise from...

asked 7 minutes ago -

MAN3240 Organizational Behavior

In one to two paragraphs

6.) How can understanding emotions make me more...

asked 15 minutes ago -

Identify one individual who, in your opinion, is an excellent

leader. List the qualities that this...

asked 12 minutes ago -

For the data set shown below, complete parts (a) through (d)

below. x 3 4 5...

asked 18 minutes ago -

A university administrator working in student housing wants to

determine if the percentage of students residing...

asked 32 minutes ago -

3). Describe human population growth that has occurred in the

past 400 years. Use terms learned...

asked 29 minutes ago -

A

projectile is blue at a target. The distance from the point of

impact to the...

asked 54 minutes ago -

Given a 32 bit processor, with 2 MB of physical RAM split into 512

frames. What...

asked 44 minutes ago -

What were the main rulings in the Supreme Court cases which are

Morgan v. Virginia (1946)...

asked 43 minutes ago