B&G Incorporated decided to change from the FIFO method of valuing inventory to the weighted average method in July 2017. The cumulative effect on prior years of retrospective application of the new inventory costing method was determined to be $15,000 net of $4,000 tax. As prices are decreasing, cost of sales would be lower and ending inventory higher for the preceding period. Retained earnings on January 1, 2017 was $241,000.

Here are the choices:

Homework Answers

| Statement of Retained Earnings (Partial) | |

| For the year ended December 31, 2017 | |

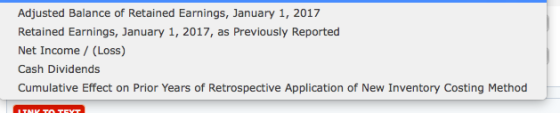

| Retained earnings on January 1, 2017 as Previously reported | $241,000 |

| Cumulative Effect on prior years of Retrospective application of new inventory costing method | $ 15,000 |

| Adjusted balance of Retained Earnings, January 1, 2017 | $ 256000 |

Add Answer to:

B&G Incorporated decided to change from the FIFO method of

valuing inventory to the weighted average...

Swifty Co. decides at the beginning of 2017 to adopt the FIFO method of inventory valuation. Swifty had used the LIFO method for financial reporting since its inception on January 1, 2015, and had mai...

Swifty Co. decides at the beginning of 2017 to adopt the FIFO method of inventory valuation. Swifty had used the LIFO method for financial reporting since its inception on January 1, 2015, and had maintained records adequate to apply the FIFO method retrospectively. Swifty concluded that FIFO is the preferable inventory method because it reflects the current cost of inventory on the balance sheet. The following table presents the effects of the change in accounting principles on inventory and cost...

he Cecil-Booker Vending Company changed its method of valuing inventory from the average cost method to...

he Cecil-Booker Vending Company changed its method of valuing inventory from the average cost method to the FIFO cost method at the beginning of 2018. At December 31, 2017, inventories were $124,000 (average cost basis) and were $128,000 a year earlier. Cecil-Booker’s accountants determined that the inventories would have totaled $163,000 at December 31, 2017, and $168,000 at December 31, 2016, if determined on a FIFO basis. A tax rate of 40% is in effect for all years. One hundred...

Presented below are income statements prepared on a LIFO and FIFO basis for Grouper Company, which...

Presented below are income statements prepared on a LIFO and

FIFO basis for Grouper Company, which started operations on January

1, 2016. The company presently uses the LIFO method of pricing its

inventory and has decided to switch to the FIFO method in 2017. The

FIFO income statement is computed in accordance with the

requirements of GAAP. Grouper’s profit-sharing agreement with its

employees indicates that the company will pay employees 10% of

income before profit-sharing. Income taxes are ignored.

LIFO...

Presented below are income statements prepared on a LIFO and

FIFO basis for Grouper Company, which started operations on January

1, 2016. The company presently uses the LIFO method of pricing its

inventory and has decided to switch to the FIFO method in 2017. The

FIFO income statement is computed in accordance with the

requirements of GAAP. Grouper’s profit-sharing agreement with its

employees indicates that the company will pay employees 10% of

income before profit-sharing. Income taxes are ignored.

LIFO...

Aquatic Equipment Corporation decided to switch from the LIFO method of costing inventories to the FIFO...

Aquatic Equipment Corporation decided to switch from the LIFO method of costing inventories to the FIFO method at the beginning of 2018. The inventory as reported at the end of 2017 using LIFO would have been $64,000 higher using FIFO. Retained earnings at the end of 2017 was reported as $820,000 (reflecting the LIFO method). The tax rate is 34%. Required: 1. Calculate the balance in retained earnings at the time of the change (beginning of 2018) as it would...

Company began operations several years ago and has used the average-cost method of inventory valuation since its inception. In 2019, it decides to switch to the FIFO method. You are provided with the...

Company began operations several years ago and has used the average-cost method of inventory valuation since its inception. In 2019, it decides to switch to the FIFO method. You are provided with the following information. Net income under avg cost Excess of average cost over fifo cost goods sold pretax Net income FIFO basis Years prior 2017 $370,000 $72,000 2017 $340,000 60,000 2018 $320,000 44,000 2019 $380,000 Instructions: 1. Prepare the journal entry to record the change from the Average...

Joey Co. decided to switch from LIFO method of costing inventories to the FIFO method at...

Joey Co. decided to switch from LIFO method of costing inventories to the FIFO method at the beginning of 2018 [1/1/2019]. The inventory as reported at the end of 2016 using LIFO would have been $60,000 higher using FIFO. Retained earnings had been reported at 12/31/2018 as $780,000 [reflecting the LIFO method]. The Tax rate is 40% 1). Calculate the balance in retained earnings at the time of the change [beginning of 20191 as it would have been reported if...

Joey Co. decided to switch from LIFO method of costing inventories to the FIFO method at the beginning of 2018 [1/1/2019]. The inventory as reported at the end of 2016 using LIFO would have been $60,000 higher using FIFO. Retained earnings had been reported at 12/31/2018 as $780,000 [reflecting the LIFO method]. The Tax rate is 40% 1). Calculate the balance in retained earnings at the time of the change [beginning of 20191 as it would have been reported if...

5. During 2014, Brookside Trading decided to change from the FIFO method of inventory valuation to...

5. During 2014, Brookside Trading decided to change from the FIFO method of inventory valuation to the weighted average method. Inventory balances under each method were as follows: January 1 December 31 FIFO 7,200,000 7,900,000 Weighted Average 7,700,000 8,300,000 Ignoring income tax, compute for the amount that should be reported as the effect of the accounting change in the statement of changes in equity for 2014,

5. During 2014, Brookside Trading decided to change from the FIFO method of inventory valuation to the weighted average method. Inventory balances under each method were as follows: January 1 December 31 FIFO 7,200,000 7,900,000 Weighted Average 7,700,000 8,300,000 Ignoring income tax, compute for the amount that should be reported as the effect of the accounting change in the statement of changes in equity for 2014,

"On December 31, Year 18, Oriole, Inc. appropriately changed its inventory valuation method to FIFO cost...

"On December 31, Year 18, Oriole, Inc. appropriately changed its inventory valuation method to FIFO cost from weighted-average cost for financial statement and income tax purposes. The change will result in a $3650000 increase in the beginning inventory at January 1, Year 18. Assume a 30% income tax rate. The cumulative effect of this accounting change on beginning retained earnings is" $0.00 "$1,095,000.00 " "$2,555,000.00 " "$3,650,000.00 "

Gerald Co. decided to switch from the FIFO method of costing inventories to the average cost...

Gerald Co. decided to switch from the FIFO method of costing inventories to the average cost method at the beginning of 2016. At December 31, 2015, Gerald’s inventory using FIFO was $20,780. Gerald inventory using average cost would have been $42,520. Gerald’s tax rate is 30%. What is the change to Retained Earnings? Indicate the amount and whether Retained Earnings would be debited (D) or Credited (C). Answer with the amount and either a D or C right beside the...

Martinez Corp. began operations in 2014. During the years 2014-2016, it reported net income and declared...

Martinez Corp. began operations in 2014. During the years

2014-2016, it reported net income and declared dividends as

follows.

Net income

Dividends declared

2014

$27,000

$ –0–

2015

118,000

–0–

2016

234,000

48,000

During 2017, Martinez Corp.:

●

discovered that it had

failed, in 2015, to record $44,000 in depreciation on equipment in

one of its warehouses.

●

changed, on January 1 ,2017,

from the average cost to the FIFO method of accounting for its

inventory. If Martinez Corp. had...

Martinez Corp. began operations in 2014. During the years

2014-2016, it reported net income and declared dividends as

follows.

Net income

Dividends declared

2014

$27,000

$ –0–

2015

118,000

–0–

2016

234,000

48,000

During 2017, Martinez Corp.:

●

discovered that it had

failed, in 2015, to record $44,000 in depreciation on equipment in

one of its warehouses.

●

changed, on January 1 ,2017,

from the average cost to the FIFO method of accounting for its

inventory. If Martinez Corp. had...

Presented below are income statements prepared on a LIFO and

FIFO basis for Grouper Company, which started operations on January

1, 2016. The company presently uses the LIFO method of pricing its

inventory and has decided to switch to the FIFO method in 2017. The

FIFO income statement is computed in accordance with the

requirements of GAAP. Grouper’s profit-sharing agreement with its

employees indicates that the company will pay employees 10% of

income before profit-sharing. Income taxes are ignored.

LIFO...

Presented below are income statements prepared on a LIFO and

FIFO basis for Grouper Company, which started operations on January

1, 2016. The company presently uses the LIFO method of pricing its

inventory and has decided to switch to the FIFO method in 2017. The

FIFO income statement is computed in accordance with the

requirements of GAAP. Grouper’s profit-sharing agreement with its

employees indicates that the company will pay employees 10% of

income before profit-sharing. Income taxes are ignored.

LIFO...

Joey Co. decided to switch from LIFO method of costing inventories to the FIFO method at the beginning of 2018 [1/1/2019]. The inventory as reported at the end of 2016 using LIFO would have been $60,000 higher using FIFO. Retained earnings had been reported at 12/31/2018 as $780,000 [reflecting the LIFO method]. The Tax rate is 40% 1). Calculate the balance in retained earnings at the time of the change [beginning of 20191 as it would have been reported if...

Joey Co. decided to switch from LIFO method of costing inventories to the FIFO method at the beginning of 2018 [1/1/2019]. The inventory as reported at the end of 2016 using LIFO would have been $60,000 higher using FIFO. Retained earnings had been reported at 12/31/2018 as $780,000 [reflecting the LIFO method]. The Tax rate is 40% 1). Calculate the balance in retained earnings at the time of the change [beginning of 20191 as it would have been reported if...

5. During 2014, Brookside Trading decided to change from the FIFO method of inventory valuation to the weighted average method. Inventory balances under each method were as follows: January 1 December 31 FIFO 7,200,000 7,900,000 Weighted Average 7,700,000 8,300,000 Ignoring income tax, compute for the amount that should be reported as the effect of the accounting change in the statement of changes in equity for 2014,

5. During 2014, Brookside Trading decided to change from the FIFO method of inventory valuation to the weighted average method. Inventory balances under each method were as follows: January 1 December 31 FIFO 7,200,000 7,900,000 Weighted Average 7,700,000 8,300,000 Ignoring income tax, compute for the amount that should be reported as the effect of the accounting change in the statement of changes in equity for 2014,

Martinez Corp. began operations in 2014. During the years

2014-2016, it reported net income and declared dividends as

follows.

Net income

Dividends declared

2014

$27,000

$ –0–

2015

118,000

–0–

2016

234,000

48,000

During 2017, Martinez Corp.:

●

discovered that it had

failed, in 2015, to record $44,000 in depreciation on equipment in

one of its warehouses.

●

changed, on January 1 ,2017,

from the average cost to the FIFO method of accounting for its

inventory. If Martinez Corp. had...

Martinez Corp. began operations in 2014. During the years

2014-2016, it reported net income and declared dividends as

follows.

Net income

Dividends declared

2014

$27,000

$ –0–

2015

118,000

–0–

2016

234,000

48,000

During 2017, Martinez Corp.:

●

discovered that it had

failed, in 2015, to record $44,000 in depreciation on equipment in

one of its warehouses.

●

changed, on January 1 ,2017,

from the average cost to the FIFO method of accounting for its

inventory. If Martinez Corp. had...

Most questions answered within 3 hours.

-

1. A manufacturer of processing chips knows that 2% of its chips

are defective in some...

asked 37 minutes ago -

Discuss what you think the exit polls tell us about voters.

asked 1 hour ago -

The electron in a hydrogen atom can undergo a transition from

n=1 to n=6, absorbing a...

asked 1 hour ago -

Based on what you learned in chapter 11, why would an

individual with a high BMI...

asked 1 hour ago -

Assume the economy can be described by the consumption function

C = $300 billion + 0.9Y...

asked 1 hour ago -

Within an environment where change is needed, you must recognize

the obstacles that can make changes...

asked 1 hour ago -

Travelcraft, Inc., manufactures a complete line of fiberglass

suitcases and attaché cases. The firm has...

asked 1 hour ago -

1a.

During 2021, a company sells 270 units of inventory for $94

each. The company has...

asked 1 hour ago -

A 7.3 kg ladder, 1.92 m long, rests on two sawhorses, as shown

in Figure 20....

asked 1 hour ago -

What is an important first step when conducting a usability

study?

A) Develop measurable tasks that...

asked 1 hour ago -

Suppose Y ~ N(4,200) and Z ~ N(6,25) and Y and Z are

independent. What is...

asked 2 hours ago -

Define poikilotherm and homeotherm, highlighting how

they are different. Both homeotherms and poikilotherms do not have...

asked 2 hours ago