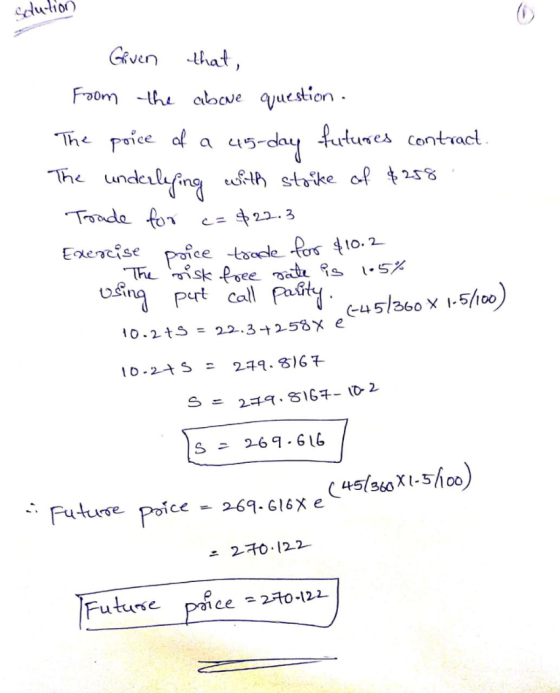

Calculate the price of a 45-day futures contract, if you know that 45-day call options on...

Calculate the price of a 45-day futures contract, if you know that 45-day call options on the underlying with strike of $258 trade for c=$22.3 and put options with the same maturity and exercise price trade for $10.2. The risk free rate is 1.5%. Please provide your answer rounded to two decimals.

Homework Answers

Add Answer to:

Calculate the price of a 45-day futures contract, if you know

that 45-day call options on...

The current price of the futures contract is $30. A six-month call option on the futures...

The current price of the futures contract is $30. A six-month call option on the futures contract with a strike price of $30 is trading at a price of $3. What is the price of a six-month put option on this futures contract with the same strike price? Please provide your answer in unit of dollars without the dollar sign (rounded to the nearest cent)

Question 16. You know that put call parity must hold and you observe the following information...

Question 16. You know that put call parity must hold and you observe the following information in the market: Spot: 195kr Strike: 180kr Call premium: 24kr Put premium: 7kr Time to maturity: 9 months exactly (the Call and the Put options have the same underlying security, strike price and maturity date) What is the risk-free rate?

A stock's current price is $72. A call option with 3-month maturity and strike price of...

A stock's current price is $72. A call option with 3-month maturity and strike price of $ 68 is trading for 6, while a put with the same strike and expiration is trading for $20. The risk free rate is 2%. How much arbitrage profit can you make by selling the put and purchasing a synthetic put? (Provide your answer rounded to two decimals.) You have purchased a put option for $ 11 three months ago. The option's strike price...

4. A trader buys a European call option and sells a European put option. The options...

4. A trader buys a European call option and sells a European put option. The options have the same underlying asset, strike price and maturity. Show that the trader's position is equivalent to a forward contract with delivery price that is equal to the strike price of the options.

4. A trader buys a European call option and sells a European put option. The options have the same underlying asset, strike price and maturity. Show that the trader's position is equivalent to a forward contract with delivery price that is equal to the strike price of the options.

4. A trader buys a call option and sells a put option. The options have the...

4. A trader buys a call option and sells a put option. The options have the same underlying asset, strike price, and maturity. Describe the trader's position. What is the advantage to making such a trade?

4. A trader buys a call option and sells a put option. The options have the same underlying asset, strike price, and maturity. Describe the trader's position. What is the advantage to making such a trade?

What is the delta of a short position in 600 European call options on silver futures?...

What is the delta of a short position in 600 European call options on silver futures? The options mature in 8 months and the silver futures contract matures in 9 months. The current 9 month futures price is $30.00 per ounce. The exercise price of the option is $31.00 per ounce. The risk-free interest rate is 5% per year and the volatility is 20 percent per year.

8. The five factors affecting prices of call and put options Both call and put options...

8. The five factors affecting prices of call and put options Both call and put options are affected by the following five factors: the exercise price, the underlying stock price, the time to expiration, the stock’s standard deviation, and the risk-free rate. However, the direction of the effects on call and put options could be different. Use the following table to identify whether each statement describes put options or call options: Statement Put Option Call Option 1. An increase in...

5. Options and Futures a. Your employer is offering you stock options on the firm as...

5. Options and Futures a. Your employer is offering you stock options on the firm as part of your pay package. You know the following about this offer: Current stock price - $25 Exercise price - $35 Maturity (yrs.)-2 Risk-free rate -4.5% Stock volatility -30% What is the value of the option? Suppose the Fed reduces Treasury rates to 4.0%, what is the new price of the option? Your company's share price falls to $23, what is the new price...

5. Options and Futures a. Your employer is offering you stock options on the firm as part of your pay package. You know the following about this offer: Current stock price - $25 Exercise price - $35 Maturity (yrs.)-2 Risk-free rate -4.5% Stock volatility -30% What is the value of the option? Suppose the Fed reduces Treasury rates to 4.0%, what is the new price of the option? Your company's share price falls to $23, what is the new price...

Assume that we have the following derivatives portfolio: A long futures contract on stock A, with...

Assume that we have the following derivatives portfolio: A long futures contract on stock A, with strike price 82 and a long put option contract on the same stock, with the same strike price. The option's premium is 8 and is payed today. The risk free rate of interest is 5%, and the time of expiration is 1 year. What will be the present value profit for the above derivatives portfolio if the stock's spot price is 109 at the...

Assume that we have the following derivatives portfolio: A long futures contract on stock A, with...

Assume that we have the following derivatives portfolio: A long futures contract on stock A, with strike price 90 and a long put option contract on the same stock, with the same strike price. The option's premium is 6 and is payed today. The risk free rate of interest is 5%, and the time of expiration is 1 year. What will be the present value profit for the above derivatives portfolio if the stock's spot price is 116 at the...

4. A trader buys a European call option and sells a European put option. The options have the same underlying asset, strike price and maturity. Show that the trader's position is equivalent to a forward contract with delivery price that is equal to the strike price of the options.

4. A trader buys a European call option and sells a European put option. The options have the same underlying asset, strike price and maturity. Show that the trader's position is equivalent to a forward contract with delivery price that is equal to the strike price of the options.

4. A trader buys a call option and sells a put option. The options have the same underlying asset, strike price, and maturity. Describe the trader's position. What is the advantage to making such a trade?

4. A trader buys a call option and sells a put option. The options have the same underlying asset, strike price, and maturity. Describe the trader's position. What is the advantage to making such a trade?

5. Options and Futures a. Your employer is offering you stock options on the firm as part of your pay package. You know the following about this offer: Current stock price - $25 Exercise price - $35 Maturity (yrs.)-2 Risk-free rate -4.5% Stock volatility -30% What is the value of the option? Suppose the Fed reduces Treasury rates to 4.0%, what is the new price of the option? Your company's share price falls to $23, what is the new price...

5. Options and Futures a. Your employer is offering you stock options on the firm as part of your pay package. You know the following about this offer: Current stock price - $25 Exercise price - $35 Maturity (yrs.)-2 Risk-free rate -4.5% Stock volatility -30% What is the value of the option? Suppose the Fed reduces Treasury rates to 4.0%, what is the new price of the option? Your company's share price falls to $23, what is the new price...

Most questions answered within 3 hours.

-

What is facilitated diffusion and how does it differ from

symport and antiport transportation? How do...

asked 17 minutes ago -

if a firm producing 100 units at $5.00 each experience

an 80% experience curve, what will...

asked 54 minutes ago -

A solid, uniform disk of radius 0.250 m and mass 53.7 kg rolls

down a ramp...

asked 3 hours ago -

Given the following table of high speed internet access vs.

annual home income:

Home Income

%...

asked 3 hours ago -

A baseball batter hits a 0.145kg baseball straight up into the

air. The baseball leaves the...

asked 4 hours ago -

An FM modulator is tested using

single-tone baseband signal with frequency of 50kHz and a sprectrum...

asked 4 hours ago -

Write the ionic equations for the first stage of salts

hydrolysis.

Anion, Cation?

Na2S

NiSO4

K2SO4...

asked 6 hours ago -

suppose there is a normally distributed population with a mean of

250 and a standard deviation...

asked 6 hours ago -

Question Three

Suppose you as project manager are using the Waterfall

development methodology on a large...

asked 7 hours ago -

Which statement is not true about welfare in Canada?

A.Benefits typically vary based on one's ability...

asked 8 hours ago -

Please help me with FLOWCHART and UML diagram for class,

thank you!

#include <iostream>

#include <fstream>...

asked 9 hours ago -

3. Describe the “logic circuit” of the Lac operon. Which

proteins are bound or not to...

asked 9 hours ago