Homework Answers

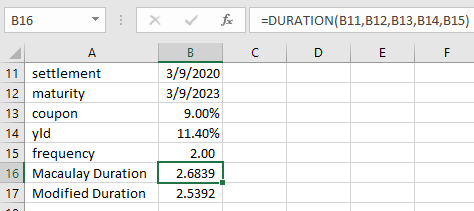

Macaulay duration is calculated using DURATION function in Excel :

Settlement = date today, which is 03/09/2020

Maturity = maturity date, which is 3 years from today, or 03/09/2023

coupon = coupon rate = 9%

yld = YTM = 6%, or 11.4%

Frequency = number of coupon payments per year = 2

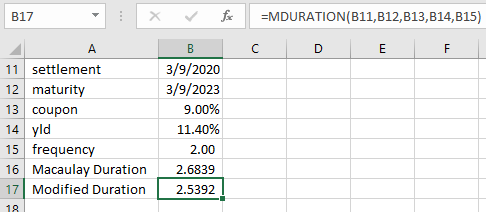

Modified duration is calculated using MDURATION function in Excel :

Settlement = date today, which is 03/09/2020

Maturity = maturity date, which is 3 years from today, or 03/09/2023

coupon = coupon rate = 9%

yld = YTM = 6%, or 11.4%

Frequency = number of coupon payments per year = 2

Add Answer to:

Find the duration of a 9.0% coupon bond making semiannually coupon payments if it has three...

Find the duration of a 7.4% coupon bond making semiannually coupon payments if it has three...

Find the duration of a 7.4% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 9.4%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 9.4% YTM Years

Find the duration of a 7.4% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 9.4%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 9.4% YTM Years

Find the duration of a 5.0% coupon bond making semiannually coupon payments if it has three...

Find the duration of a 5.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 8% YTM Years

Find the duration of a 5.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 8% YTM Years

Find the duration of a 7.2% coupon bond making semiannually coupon payments if it has three...

Find the duration of a 7.2% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 10.0%? Note: The face value of the bond is $100. (Do not round Intermediate calculations. Round your answers to 4 decimal places.) 6% YTM 10% YTM

Find the duration of a 7.2% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 10.0%? Note: The face value of the bond is $100. (Do not round Intermediate calculations. Round your answers to 4 decimal places.) 6% YTM 10% YTM

Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three...

Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM 8% YTM 2.8827 X 2.8792 X Years Years

Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM 8% YTM 2.8827 X 2.8792 X Years Years

Find the duration of a 6% coupon bond making semiannually coupon payments if it has three...

Find the duration of a 6% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6%. What is the duration if the yield to maturity is 10%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Duration 6% YTM years 10% YTM years

Find the duration of a 6% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6%. What is the duration if the yield to maturity is 10%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Duration 6% YTM years 10% YTM years

Problem 16-5 Find the duration of a 4.0% coupon bond making semiannually coupon payments if it...

Problem 16-5 Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Years 6% YTM 8% YTM : Years

Problem 16-5 Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Years 6% YTM 8% YTM : Years

Find the duration of a 7% coupon bond making annual coupon payments if it has three...

Find the duration of a 7% coupon bond making annual coupon payments if it has three years until maturity and a yield to maturity of 7.4%. What is the duration if the yield to maturity is 11.4%? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Duration YTM 7.4% YTM 11.4% YTM

Find the duration of a 7% coupon bond making annual coupon payments if it has three years until maturity and a yield to maturity of 7.4%. What is the duration if the yield to maturity is 11.4%? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Duration YTM 7.4% YTM 11.4% YTM

Find the duration of a 8% coupon bond making annual coupon payments if it has 3 years until matur...

Find the duration of a 8% coupon bond making annual coupon payments if it has 3 years until maturity and has a yield to maturity of 10%. Note: The face value of the bond is $1,000. (Do not round intermediate calculations. Round your answers to 3 decimal places.) 10% YTM: Duration = ________ years

Find the duration of a 8% coupon bond making annual coupon payments if it has three...

Find the duration of a 8% coupon bond making annual coupon payments if it has three years until maturity and a yield to maturity of 72% What is the duration if the yield to maturity is 11.2%? (Do not round Intermediate calculations. Round your answers to 4 decimal places.) 7.22 YTM 11.2 YTM

Find the duration of a 8% coupon bond making annual coupon payments if it has three years until maturity and a yield to maturity of 72% What is the duration if the yield to maturity is 11.2%? (Do not round Intermediate calculations. Round your answers to 4 decimal places.) 7.22 YTM 11.2 YTM

a. Find the duration of a 7% coupon bond making annual coupon payments if it has...

a. Find the duration of a 7% coupon bond making annual coupon payments if it has three years until maturity and has a yield to maturity of 7%. Note: The face value of the bond is $1,000. (Do not round intermediate calculations. Round your answers to 3 decimal places.) 7% ΥTM years b. What is the duration if the yield to maturity is 8.4%? Note: The face value of the bond is $1,000. (Do not round intermediate calculations. Round your...

a. Find the duration of a 7% coupon bond making annual coupon payments if it has three years until maturity and has a yield to maturity of 7%. Note: The face value of the bond is $1,000. (Do not round intermediate calculations. Round your answers to 3 decimal places.) 7% ΥTM years b. What is the duration if the yield to maturity is 8.4%? Note: The face value of the bond is $1,000. (Do not round intermediate calculations. Round your...

Find the duration of a 7.4% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 9.4%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 9.4% YTM Years

Find the duration of a 7.4% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 9.4%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 9.4% YTM Years

Find the duration of a 5.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 8% YTM Years

Find the duration of a 5.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM Years 8% YTM Years

Find the duration of a 7.2% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 10.0%? Note: The face value of the bond is $100. (Do not round Intermediate calculations. Round your answers to 4 decimal places.) 6% YTM 10% YTM

Find the duration of a 7.2% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 10.0%? Note: The face value of the bond is $100. (Do not round Intermediate calculations. Round your answers to 4 decimal places.) 6% YTM 10% YTM

Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM 8% YTM 2.8827 X 2.8792 X Years Years

Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) 6% YTM 8% YTM 2.8827 X 2.8792 X Years Years

Find the duration of a 6% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6%. What is the duration if the yield to maturity is 10%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Duration 6% YTM years 10% YTM years

Find the duration of a 6% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6%. What is the duration if the yield to maturity is 10%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Duration 6% YTM years 10% YTM years

Problem 16-5 Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Years 6% YTM 8% YTM : Years

Problem 16-5 Find the duration of a 4.0% coupon bond making semiannually coupon payments if it has three years until maturity and has a yield to maturity of 6.0%. What is the duration if the yield to maturity is 8.0%? Note: The face value of the bond is $100. (Do not round intermediate calculations. Round your answers to 4 decimal places.) Years 6% YTM 8% YTM : Years

Find the duration of a 7% coupon bond making annual coupon payments if it has three years until maturity and a yield to maturity of 7.4%. What is the duration if the yield to maturity is 11.4%? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Duration YTM 7.4% YTM 11.4% YTM

Find the duration of a 7% coupon bond making annual coupon payments if it has three years until maturity and a yield to maturity of 7.4%. What is the duration if the yield to maturity is 11.4%? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Duration YTM 7.4% YTM 11.4% YTM

Find the duration of a 8% coupon bond making annual coupon payments if it has three years until maturity and a yield to maturity of 72% What is the duration if the yield to maturity is 11.2%? (Do not round Intermediate calculations. Round your answers to 4 decimal places.) 7.22 YTM 11.2 YTM

Find the duration of a 8% coupon bond making annual coupon payments if it has three years until maturity and a yield to maturity of 72% What is the duration if the yield to maturity is 11.2%? (Do not round Intermediate calculations. Round your answers to 4 decimal places.) 7.22 YTM 11.2 YTM

a. Find the duration of a 7% coupon bond making annual coupon payments if it has three years until maturity and has a yield to maturity of 7%. Note: The face value of the bond is $1,000. (Do not round intermediate calculations. Round your answers to 3 decimal places.) 7% ΥTM years b. What is the duration if the yield to maturity is 8.4%? Note: The face value of the bond is $1,000. (Do not round intermediate calculations. Round your...

a. Find the duration of a 7% coupon bond making annual coupon payments if it has three years until maturity and has a yield to maturity of 7%. Note: The face value of the bond is $1,000. (Do not round intermediate calculations. Round your answers to 3 decimal places.) 7% ΥTM years b. What is the duration if the yield to maturity is 8.4%? Note: The face value of the bond is $1,000. (Do not round intermediate calculations. Round your...

Most questions answered within 3 hours.

-

In 2017, Juan entered into a contract to write a book. The

publisher advanced Juan $50,000,...

asked 7 minutes ago -

Determine the number of kinds of protons in each molecule (w/

respect to NMR spectroscopy). Drawing...

asked 17 minutes ago -

A jeweler whose near point is 68 cm from his eye uses a

magnifying glass as...

asked 15 minutes ago -

A company wants to determine how many units of each of two

products, A and B,...

asked 19 minutes ago -

The blood pressure of a person changes throughout the day.

Suppose the systolic blood pressure of...

asked 28 minutes ago -

A chemistry student desired to study sulfur. Sulfur exhibited

the following characteristics with oxygen:

(a) It...

asked 24 minutes ago -

An Atwood machine is constructed of a solid-disk frictionless

pulley of mass m3 and radius R....

asked 26 minutes ago -

what are the advantages of lanthanum hexaboride over tungsten

filament for electron emission

what is the...

asked 27 minutes ago -

Question 5

Your uncle offers to sell you his vintage Rolls Royce. He

suggests a payment...

asked 32 minutes ago -

Quality grading of beef products as Prime, Choice, Select. What

type of data?

A) ratio

B)...

asked 41 minutes ago -

For the following unbalanced reaction at 0.800

atm and 34.5°C:

MoS2(s) + O2(g) → MoO3(s) +...

asked 49 minutes ago -

When 12 mL of 0.2 M NaOH is added to 25 mL of 0.15 M HCl,...

asked 53 minutes ago