Homework Answers

Add Answer to:

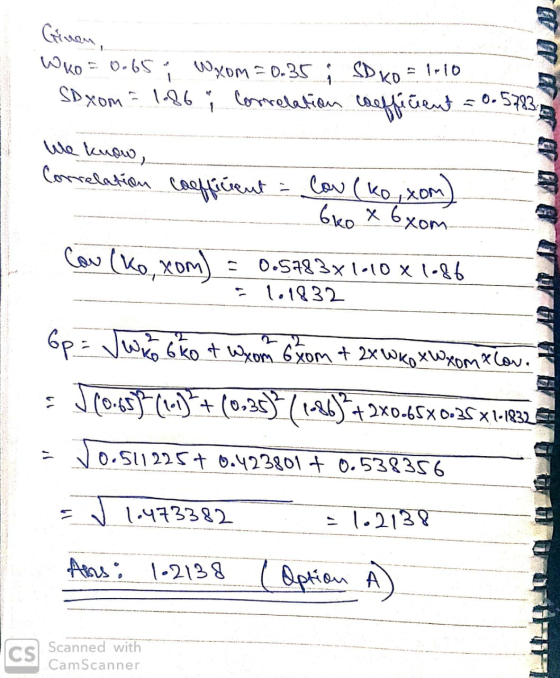

QUESTION 3 An investor has a portfolio consisting of 65% KO and 35% XOM. What is...

P.14 An investor holding a portfolio consisting of two stocks invests 25% of assets in Stock...

P.14 An investor holding a portfolio consisting of two stocks invests 25% of assets in Stock A and 75% into Stock B. The return RA from Stock A has a mean of 4% and a standard deviation of A = 8%. Stock B has an expected return E(RB) = 8% with a standard deviation of ob = 12%. The portfolio return is P = 0.25RA +0.75RB. (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of...

P.14 An investor holding a portfolio consisting of two stocks invests 25% of assets in Stock A and 75% into Stock B. The return RA from Stock A has a mean of 4% and a standard deviation of A = 8%. Stock B has an expected return E(RB) = 8% with a standard deviation of ob = 12%. The portfolio return is P = 0.25RA +0.75RB. (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of...

statistics 4. An investor holds a portfolio consisting of two stocks. She puts 25% of her...

statistics

4. An investor holds a portfolio consisting of two stocks. She puts 25% of her money in Stock A and 75% into Stock B. Stock A has an expected return of Ri=8% and a standard deviation of 0,=12%. Stock B has an expected return of Rg=15% with a standard deviation of o,=22%. The portfolio return is P=0.25RA +0.75R, (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of the returns on the portfolio assuming that...

statistics

4. An investor holds a portfolio consisting of two stocks. She puts 25% of her money in Stock A and 75% into Stock B. Stock A has an expected return of Ri=8% and a standard deviation of 0,=12%. Stock B has an expected return of Rg=15% with a standard deviation of o,=22%. The portfolio return is P=0.25RA +0.75R, (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of the returns on the portfolio assuming that...

Consider the following case: Rajiv is an amateur investor who holds a small portfolio consisting of...

Consider the following case: Rajiv is an amateur investor who holds a small portfolio consisting of only four stocks. The stock holdings in his portfolio are shown in the following table: Stock Percentage of Portfolio Expected Return Standard Deviation Artemis Inc. 20% 6.00% 23.00% Babish & Co. 30% 14.00% 27.00% Cornell Industries 35% 12.00% 30.00% Danforth Motors 15% 5.00% 32.00% The expected return on Rajiv’s stock portfolio is a) 10.35% b) 7.7625% c) 15.52% d) 13.9725% Suppose each stock in...

Consider the following case: Andre is an amateur investor who holds a small portfolio consisting of only four stock...

Consider the following case: Andre is an amateur investor who holds a small portfolio consisting of only four stocks. The stock holdings in his portfolio are shown in the following table: Standard Percentage of Expected Stock Deviation Portfolio Return Artemis Inc. 20% 8.00% 31.00% Babish & Co. Cornell Industries 35.00% 30% 14.00% 38.00% 35% 12.00% Danforth Motors 15% 5.00% 40.00% What is the expected return on Andre's stock portfolio? 14.51% 16.13% 10.75% 8.06% Suppose each stock in Andre's portfolio has...

Consider the following case: Andre is an amateur investor who holds a small portfolio consisting of only four stocks. The stock holdings in his portfolio are shown in the following table: Standard Percentage of Expected Stock Deviation Portfolio Return Artemis Inc. 20% 8.00% 31.00% Babish & Co. Cornell Industries 35.00% 30% 14.00% 38.00% 35% 12.00% Danforth Motors 15% 5.00% 40.00% What is the expected return on Andre's stock portfolio? 14.51% 16.13% 10.75% 8.06% Suppose each stock in Andre's portfolio has...

An investor can design a risky portfolio based on two stocks, A and B. Stock A...

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 45% and a standard deviation of return of 9%. Stock B has an expected return of 15% and a standard deviation of return of 2%.The correlation coefficient between the returns of A and B is 0.0025. The risk-free rate of return is 2%. The standard deviation of return on the minimum variance portfolio is _________.

Question 3 (total of 20 marks): An investor holds a portfolio comprising three assets (or stocks)...

Question 3 (total of 20 marks): An investor holds a portfolio comprising three assets (or stocks) A, B and C. Refer to the below tables to answer the questions that follow. Assume that returns are effective annual rates: Variables Stock A Stock B Stock C 33% 40% 25% Stock return standard deviation 0.25 $ 55,000.00 0.33 35,000.00 0.22 10,000.00 Investment $ $ Assume the following information holds: Correlation coefficient of the returns between A & B 0.10 Correlation coefficient of...

Question 3 (total of 20 marks): An investor holds a portfolio comprising three assets (or stocks) A, B and C. Refer to the below tables to answer the questions that follow. Assume that returns are effective annual rates: Variables Stock A Stock B Stock C 33% 40% 25% Stock return standard deviation 0.25 $ 55,000.00 0.33 35,000.00 0.22 10,000.00 Investment $ $ Assume the following information holds: Correlation coefficient of the returns between A & B 0.10 Correlation coefficient of...

a. You have constructed a portfolio consisting of 40 percent Stock A and 60 percent Stock...

a. You have constructed a portfolio consisting of 40 percent Stock A and 60 percent Stock B. Stock A has expected return of 15 percent and standard deviation of 20 percent. Stock B has expected return of 7 percent and standard deviation of 10 percent. The correlation between the returns of these stocks is 0.5. Compute the expected return and standard deviation of your portfolio returns. (10 pts)

a. You have constructed a portfolio consisting of 40 percent Stock A and 60 percent Stock B. Stock A has expected return of 15 percent and standard deviation of 20 percent. Stock B has expected return of 7 percent and standard deviation of 10 percent. The correlation between the returns of these stocks is 0.5. Compute the expected return and standard deviation of your portfolio returns. (10 pts)

An investor can design a risky portfolio based on two stocks, A and B. Stock A...

An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 14% and a standard deviation of return of 24.0%. Stock B has an expected return of 10% and a standard deviation of return of 4%. The correlation coefficient between the returns of A and B is 0.50. The risk-free rate of return is 8%. The proportion of the optimal risky portfolio that should be invested in stock A is...

Consider an investor who owns two stocks. Google Inc. (GOOGL) has an expected return of 8...

Consider an investor who owns two stocks. Google Inc. (GOOGL) has an expected return of 8 percent, and the investor owns $15,000 worth of the stock and he also owns $10,000 of Amazon Inc. (AMZN), which has an expected return of 6 percent. What is the expected return of his portfolio? The correlation between the two stocks is ? = ‒ 0.4. What is the standard deviation of the portfolio if the standard deviations of the two stocks are ??????...

Show work in excel please An investor can design a risky portfolio based on two stocks,...

Show work in excel please An investor can design a risky portfolio based on two stocks, A and B. Stock A has an expected return of 19% and a standard deviation of return of 15.0%. Stock B has an expected return of 15% and a standard deviation of return of 6%. The correlation coefficient between the returns of A and B is 0.80. The risk-free rate of return is 11%. The proportion of the optimal risky portfolio that should be...

P.14 An investor holding a portfolio consisting of two stocks invests 25% of assets in Stock A and 75% into Stock B. The return RA from Stock A has a mean of 4% and a standard deviation of A = 8%. Stock B has an expected return E(RB) = 8% with a standard deviation of ob = 12%. The portfolio return is P = 0.25RA +0.75RB. (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of...

P.14 An investor holding a portfolio consisting of two stocks invests 25% of assets in Stock A and 75% into Stock B. The return RA from Stock A has a mean of 4% and a standard deviation of A = 8%. Stock B has an expected return E(RB) = 8% with a standard deviation of ob = 12%. The portfolio return is P = 0.25RA +0.75RB. (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of...

statistics

4. An investor holds a portfolio consisting of two stocks. She puts 25% of her money in Stock A and 75% into Stock B. Stock A has an expected return of Ri=8% and a standard deviation of 0,=12%. Stock B has an expected return of Rg=15% with a standard deviation of o,=22%. The portfolio return is P=0.25RA +0.75R, (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of the returns on the portfolio assuming that...

statistics

4. An investor holds a portfolio consisting of two stocks. She puts 25% of her money in Stock A and 75% into Stock B. Stock A has an expected return of Ri=8% and a standard deviation of 0,=12%. Stock B has an expected return of Rg=15% with a standard deviation of o,=22%. The portfolio return is P=0.25RA +0.75R, (a) Compute the expected return on the portfolio. (b) Compute the standard deviation of the returns on the portfolio assuming that...

Consider the following case: Andre is an amateur investor who holds a small portfolio consisting of only four stocks. The stock holdings in his portfolio are shown in the following table: Standard Percentage of Expected Stock Deviation Portfolio Return Artemis Inc. 20% 8.00% 31.00% Babish & Co. Cornell Industries 35.00% 30% 14.00% 38.00% 35% 12.00% Danforth Motors 15% 5.00% 40.00% What is the expected return on Andre's stock portfolio? 14.51% 16.13% 10.75% 8.06% Suppose each stock in Andre's portfolio has...

Consider the following case: Andre is an amateur investor who holds a small portfolio consisting of only four stocks. The stock holdings in his portfolio are shown in the following table: Standard Percentage of Expected Stock Deviation Portfolio Return Artemis Inc. 20% 8.00% 31.00% Babish & Co. Cornell Industries 35.00% 30% 14.00% 38.00% 35% 12.00% Danforth Motors 15% 5.00% 40.00% What is the expected return on Andre's stock portfolio? 14.51% 16.13% 10.75% 8.06% Suppose each stock in Andre's portfolio has...

Question 3 (total of 20 marks): An investor holds a portfolio comprising three assets (or stocks) A, B and C. Refer to the below tables to answer the questions that follow. Assume that returns are effective annual rates: Variables Stock A Stock B Stock C 33% 40% 25% Stock return standard deviation 0.25 $ 55,000.00 0.33 35,000.00 0.22 10,000.00 Investment $ $ Assume the following information holds: Correlation coefficient of the returns between A & B 0.10 Correlation coefficient of...

Question 3 (total of 20 marks): An investor holds a portfolio comprising three assets (or stocks) A, B and C. Refer to the below tables to answer the questions that follow. Assume that returns are effective annual rates: Variables Stock A Stock B Stock C 33% 40% 25% Stock return standard deviation 0.25 $ 55,000.00 0.33 35,000.00 0.22 10,000.00 Investment $ $ Assume the following information holds: Correlation coefficient of the returns between A & B 0.10 Correlation coefficient of...

a. You have constructed a portfolio consisting of 40 percent Stock A and 60 percent Stock B. Stock A has expected return of 15 percent and standard deviation of 20 percent. Stock B has expected return of 7 percent and standard deviation of 10 percent. The correlation between the returns of these stocks is 0.5. Compute the expected return and standard deviation of your portfolio returns. (10 pts)

a. You have constructed a portfolio consisting of 40 percent Stock A and 60 percent Stock B. Stock A has expected return of 15 percent and standard deviation of 20 percent. Stock B has expected return of 7 percent and standard deviation of 10 percent. The correlation between the returns of these stocks is 0.5. Compute the expected return and standard deviation of your portfolio returns. (10 pts)

Most questions answered within 3 hours.

-

A scientist randomly mutates the DNA of a bacterium. She then

sequences the bacterium’s daughter cells,...

asked 4 minutes ago -

A 3.15-g bullet embeds itself in a 1.17-kg block, which is

attached to a spring of...

asked 12 minutes ago -

A hawk is flying horizontally at 24.0 m/s in a straight line,

185 m above the...

asked 13 minutes ago -

Draw a Supply and Demand Graph for yourself. Now draw a dashed

line vertically down through...

asked 10 minutes ago -

1a. An aqueous solution of calcium hydroxide is

standardized by titration with a 0.116 M solution...

asked 15 minutes ago -

In response to concerns about nutritional contents of fast

foods, McDonald's has announced that it will...

asked 31 minutes ago -

A gun with inertia 5.5 kg fires a 13-g bullet at a stationary

target located 1.0...

asked 32 minutes ago -

A box contains twenty-five screws which are identical in size,

but 13 of which are copper...

asked 35 minutes ago -

“Is it possible that objectively

a product is high quality but subjectively low

quality?”

Please support...

asked 36 minutes ago -

OCHEM LAB

Why does hydration of 2-methyl-3-butyn-2-ol give the ketone,

3-hydroxy-3-methyl-2-butanone (4), rather than the aldehyde,...

asked 46 minutes ago -

A sample of gas at 15 ⁰C and 0.988 atm has a volume of 2.58

liters....

asked 53 minutes ago -

Enzymes are required in retroviruses because the genome

is not used directly as mRNA (T/F)

Please...

asked 51 minutes ago