Homework Answers

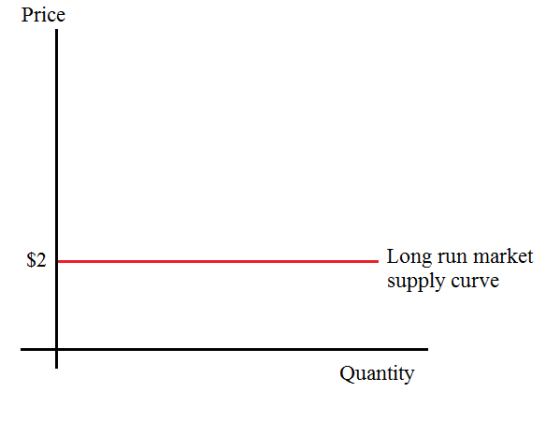

a) In the long run price is equal to minimum of LRAC

Here LRAC = 2q^2 – 4q + 4 and so LRAC’(q) = 0 gives 4q – 4 = 0 or q = 1. Hence long run price is fixed at P = 2(1^2) – 4*1 + 4 = $2

b) Total quantity traded Q = 516 – 2 – 2^2 = 510 units

c) Number of firms = Qs/qs = 510/1 = 510 firms

d) It is a constant cost industry so long run supply function is a horizontal line fixed at a price of $2.

Add Answer to:

Part 3: Answer each problem. Be sure to explain the logic behind your answer and show...

Please show as much work and explanation as possible, thank you so much! 7. Which ones of the followings are true in per...

Please show as much work and explanation as

possible, thank you so much!

7. Which ones of the followings are true in perfectly competitive markets? (a) The industry demand curve is flat. (b) Firms' marginal revenue is constant as quantity varies. (c) From a firm's perspective, its price elasticity of demand is zero. 8. Which ones of the followings are true about firms’ short-run behavior in a perfectly competitive market? (a) Firms shut down whenever profit is negative. (b) Firms...

Please show as much work and explanation as

possible, thank you so much!

7. Which ones of the followings are true in perfectly competitive markets? (a) The industry demand curve is flat. (b) Firms' marginal revenue is constant as quantity varies. (c) From a firm's perspective, its price elasticity of demand is zero. 8. Which ones of the followings are true about firms’ short-run behavior in a perfectly competitive market? (a) Firms shut down whenever profit is negative. (b) Firms...

12. In the long run: A. there will be no entry or exit of firms in...

12. In the long run: A. there will be no entry or exit of firms in this industry B. new firms enter the industry and curve A shifts to the right. C. firms exit this industry and curve A shifts to the left D. new firms enter this industry and curve F shifts to the right Questions 1- 14 refer to Figure 1 I. The industry's short-run supply curve is curve A. A H B. С.Е. D. F 2. The...

12. In the long run: A. there will be no entry or exit of firms in this industry B. new firms enter the industry and curve A shifts to the right. C. firms exit this industry and curve A shifts to the left D. new firms enter this industry and curve F shifts to the right Questions 1- 14 refer to Figure 1 I. The industry's short-run supply curve is curve A. A H B. С.Е. D. F 2. The...

Number 6 . Can you explain the reasoning behind please 6. A perfectly competitive firm produces...

Number 6 . Can you explain the reasoning behind please

6. A perfectly competitive firm produces where p MC-ATC. -M尺 a. Its marginal revenue is always equal to the market price. b. Its marginal cost is always equal to the market price. c. Its marginal revenue is always equal to the average total cost. d. All of the above are correct. 7. The fol llowing graphs show the market for a good traded in a perfectly competitive market, and the...

Number 6 . Can you explain the reasoning behind please

6. A perfectly competitive firm produces where p MC-ATC. -M尺 a. Its marginal revenue is always equal to the market price. b. Its marginal cost is always equal to the market price. c. Its marginal revenue is always equal to the average total cost. d. All of the above are correct. 7. The fol llowing graphs show the market for a good traded in a perfectly competitive market, and the...

Consider a perfectly competitive industry in which each firm i has a total cost function given...

Consider a perfectly competitive industry in which each firm i has a total cost function given by the equation: TC= 128 + 4q+2q^2. Further assume that the industry demand function is given by the following: P = 84 – 2Q. a) Describe the long run market equilibrium. That is, identify the equilibrium price and quantity, output for each firm, the number of firms in the industry and the level of producer and consumer surplus. What is the value of own...

Possible Answers 1: Earn zero profit, Earn positive profit, shut down, operate at a loss 2: Enter, Exit, Neither 3:Zero...

Possible Answers

1: Earn zero profit, Earn positive profit, shut down, operate at

a loss

2: Enter, Exit, Neither

3:Zero, Positive, Negative

4:10,15,20

Consider the perfectly competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average cost (AC), and average variable cost (AVC) curves shown on the following graph. 100 90 80 70 60 50 40 AC 30 20 AVC MC...

Possible Answers

1: Earn zero profit, Earn positive profit, shut down, operate at

a loss

2: Enter, Exit, Neither

3:Zero, Positive, Negative

4:10,15,20

Consider the perfectly competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average cost (AC), and average variable cost (AVC) curves shown on the following graph. 100 90 80 70 60 50 40 AC 30 20 AVC MC...

Please help me answer this economics question concerning graphing. Consider the perfectly competitive market for titanium....

Please help me answer this economics question concerning

graphing.

Consider the perfectly competitive market for titanium. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph 80 72 64 48 D 40 32 24 16 AVC MC 0 3 69 12 15 18 21 24 27 30 QUANTITY (Thousands of pounds)...

Please help me answer this economics question concerning

graphing.

Consider the perfectly competitive market for titanium. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph 80 72 64 48 D 40 32 24 16 AVC MC 0 3 69 12 15 18 21 24 27 30 QUANTITY (Thousands of pounds)...

3. There are two types of firms in an industry. Type 1 firms have the costs...

3. There are two types of firms in an industry. Type 1 firms have the costs TC(n) = 625+ 0.25qi and type 2 firms have costs TC(2) 50000.52 The fixed costs for both types of firms are NOT sunk. (a) Derive each firm's ATC(g), AVC() and MC() functions and plot the curves on separate diagrams (b) Derive each firm's supply function q(p) and show the corresponding curves in the diagrams (c Suppose that there are 10 firms of each type....

3. There are two types of firms in an industry. Type 1 firms have the costs TC(n) = 625+ 0.25qi and type 2 firms have costs TC(2) 50000.52 The fixed costs for both types of firms are NOT sunk. (a) Derive each firm's ATC(g), AVC() and MC() functions and plot the curves on separate diagrams (b) Derive each firm's supply function q(p) and show the corresponding curves in the diagrams (c Suppose that there are 10 firms of each type....

5. Short-run supply and long-run equilibrium Consider the perfectly competitive market for steel. Assume that, regardless...

5. Short-run supply and long-run equilibrium Consider the perfectly competitive market for steel. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. COSTS (Dollars per ton) + MC D AVC 0 10 90 100 20 30 40 50 60 70 80 QUANTITY (Thousands of tons) The following diagram shows the...

5. Short-run supply and long-run equilibrium Consider the perfectly competitive market for steel. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. COSTS (Dollars per ton) + MC D AVC 0 10 90 100 20 30 40 50 60 70 80 QUANTITY (Thousands of tons) The following diagram shows the...

Attempts: Keep the Highest: /4 7. Short-run supply and long-run equilibrium Consider the perfectly competitive...

Attempts: Keep the Highest: /4 7. Short-run supply and long-run equilibrium Consider the perfectly competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average cost (AC), and average variable cost (AVC) curves shown on the following graph 100 60 AVC 0 10 20 3040 50 60 800100 Use the orange points (square symbol) to plot the initial short-run industry supply curve...

Attempts: Keep the Highest: /4 7. Short-run supply and long-run equilibrium Consider the perfectly competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average cost (AC), and average variable cost (AVC) curves shown on the following graph 100 60 AVC 0 10 20 3040 50 60 800100 Use the orange points (square symbol) to plot the initial short-run industry supply curve...

Please show as much work and explanation as

possible, thank you so much!

7. Which ones of the followings are true in perfectly competitive markets? (a) The industry demand curve is flat. (b) Firms' marginal revenue is constant as quantity varies. (c) From a firm's perspective, its price elasticity of demand is zero. 8. Which ones of the followings are true about firms’ short-run behavior in a perfectly competitive market? (a) Firms shut down whenever profit is negative. (b) Firms...

Please show as much work and explanation as

possible, thank you so much!

7. Which ones of the followings are true in perfectly competitive markets? (a) The industry demand curve is flat. (b) Firms' marginal revenue is constant as quantity varies. (c) From a firm's perspective, its price elasticity of demand is zero. 8. Which ones of the followings are true about firms’ short-run behavior in a perfectly competitive market? (a) Firms shut down whenever profit is negative. (b) Firms...

12. In the long run: A. there will be no entry or exit of firms in this industry B. new firms enter the industry and curve A shifts to the right. C. firms exit this industry and curve A shifts to the left D. new firms enter this industry and curve F shifts to the right Questions 1- 14 refer to Figure 1 I. The industry's short-run supply curve is curve A. A H B. С.Е. D. F 2. The...

12. In the long run: A. there will be no entry or exit of firms in this industry B. new firms enter the industry and curve A shifts to the right. C. firms exit this industry and curve A shifts to the left D. new firms enter this industry and curve F shifts to the right Questions 1- 14 refer to Figure 1 I. The industry's short-run supply curve is curve A. A H B. С.Е. D. F 2. The...

Number 6 . Can you explain the reasoning behind please

6. A perfectly competitive firm produces where p MC-ATC. -M尺 a. Its marginal revenue is always equal to the market price. b. Its marginal cost is always equal to the market price. c. Its marginal revenue is always equal to the average total cost. d. All of the above are correct. 7. The fol llowing graphs show the market for a good traded in a perfectly competitive market, and the...

Number 6 . Can you explain the reasoning behind please

6. A perfectly competitive firm produces where p MC-ATC. -M尺 a. Its marginal revenue is always equal to the market price. b. Its marginal cost is always equal to the market price. c. Its marginal revenue is always equal to the average total cost. d. All of the above are correct. 7. The fol llowing graphs show the market for a good traded in a perfectly competitive market, and the...

Possible Answers

1: Earn zero profit, Earn positive profit, shut down, operate at

a loss

2: Enter, Exit, Neither

3:Zero, Positive, Negative

4:10,15,20

Consider the perfectly competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average cost (AC), and average variable cost (AVC) curves shown on the following graph. 100 90 80 70 60 50 40 AC 30 20 AVC MC...

Possible Answers

1: Earn zero profit, Earn positive profit, shut down, operate at

a loss

2: Enter, Exit, Neither

3:Zero, Positive, Negative

4:10,15,20

Consider the perfectly competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average cost (AC), and average variable cost (AVC) curves shown on the following graph. 100 90 80 70 60 50 40 AC 30 20 AVC MC...

Please help me answer this economics question concerning

graphing.

Consider the perfectly competitive market for titanium. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph 80 72 64 48 D 40 32 24 16 AVC MC 0 3 69 12 15 18 21 24 27 30 QUANTITY (Thousands of pounds)...

Please help me answer this economics question concerning

graphing.

Consider the perfectly competitive market for titanium. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph 80 72 64 48 D 40 32 24 16 AVC MC 0 3 69 12 15 18 21 24 27 30 QUANTITY (Thousands of pounds)...

3. There are two types of firms in an industry. Type 1 firms have the costs TC(n) = 625+ 0.25qi and type 2 firms have costs TC(2) 50000.52 The fixed costs for both types of firms are NOT sunk. (a) Derive each firm's ATC(g), AVC() and MC() functions and plot the curves on separate diagrams (b) Derive each firm's supply function q(p) and show the corresponding curves in the diagrams (c Suppose that there are 10 firms of each type....

3. There are two types of firms in an industry. Type 1 firms have the costs TC(n) = 625+ 0.25qi and type 2 firms have costs TC(2) 50000.52 The fixed costs for both types of firms are NOT sunk. (a) Derive each firm's ATC(g), AVC() and MC() functions and plot the curves on separate diagrams (b) Derive each firm's supply function q(p) and show the corresponding curves in the diagrams (c Suppose that there are 10 firms of each type....

5. Short-run supply and long-run equilibrium Consider the perfectly competitive market for steel. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. COSTS (Dollars per ton) + MC D AVC 0 10 90 100 20 30 40 50 60 70 80 QUANTITY (Thousands of tons) The following diagram shows the...

5. Short-run supply and long-run equilibrium Consider the perfectly competitive market for steel. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. COSTS (Dollars per ton) + MC D AVC 0 10 90 100 20 30 40 50 60 70 80 QUANTITY (Thousands of tons) The following diagram shows the...

Attempts: Keep the Highest: /4 7. Short-run supply and long-run equilibrium Consider the perfectly competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average cost (AC), and average variable cost (AVC) curves shown on the following graph 100 60 AVC 0 10 20 3040 50 60 800100 Use the orange points (square symbol) to plot the initial short-run industry supply curve...

Attempts: Keep the Highest: /4 7. Short-run supply and long-run equilibrium Consider the perfectly competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average cost (AC), and average variable cost (AVC) curves shown on the following graph 100 60 AVC 0 10 20 3040 50 60 800100 Use the orange points (square symbol) to plot the initial short-run industry supply curve...

Most questions answered within 3 hours.

-

(Expected rate of return and risk) Carter Inc. is evaluating a

security. Calculate the investment’s expected...

asked 1 hour ago -

What specific indicators can point to lack of progress for

African Americans in American society?

asked 2 hours ago -

1-The Electrons in a beam are moving at 2.7×108 m/s in an

electric field of 15000...

asked 2 hours ago -

A gas tank is a vertical cylinder. It has a radius of 1m, a

height of...

asked 3 hours ago -

Accent Software faces the following conditions. All of these

support Accent’s use of a market-penetration pricing...

asked 4 hours ago -

A mathematically inclined friend emails you the following

instructions: "Meet me in the cafeteria the first...

asked 4 hours ago -

A monopoly sells in two countries . The demand curves in the two

countries are p1...

asked 5 hours ago -

A .15kg rubber ball is bounced off a wall. Before hitting the

wall, the ball moves...

asked 5 hours ago -

A manufacturing company preparing to build a new plant is

considering three potential locations for it....

asked 5 hours ago -

B. If compound Y has approximately the same values of solubility

in toluene as compound X,...

asked 6 hours ago -

Oscar Inc. has inventory in Japan valued at 39,051,000 Yen one

year ago. One year ago...

asked 6 hours ago -

If Canada suffered from "fundamental disequilibrium," and its

government choose not to devalue its currency, a...

asked 6 hours ago