Homework Answers

Given,

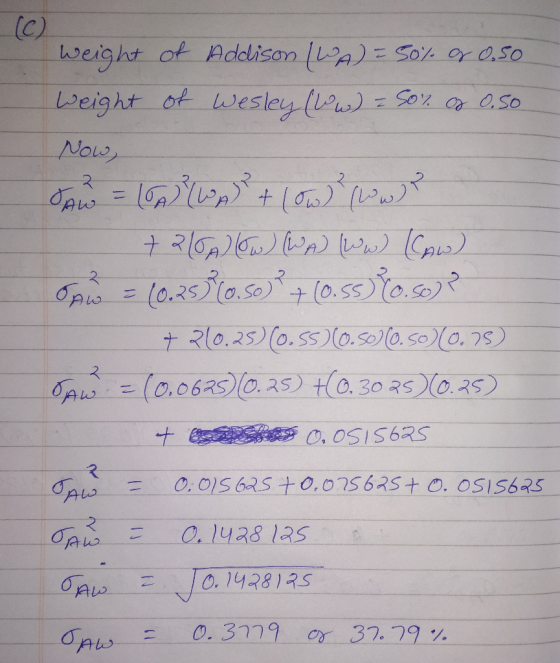

Volatility of Addison's stock = 25% or 0.25

Volatility of Wesley's stock = 55% or 0.55

Correlation = 75% or 0.75

Solution :-

Add Answer to:

solve a, b, and c

JUIC: U ULIP 18 (12 complete) V W Score: 74.36%, 9.67...

(%) P11-11 (similar to) Suppose Wesley Publishing's stock has a volatility of 40%, while Addison Printing's...

(%) P11-11 (similar to) Suppose Wesley Publishing's stock has a volatility of 40%, while Addison Printing's stock has a volatility of 25%. If the correlation between these stocks is 40%, what is the volatility of the following portfolios of Addison and Wesley: a. 100% Addison b, 75% Addison and 25% Wesley c.50% Addison and 50% Wesley a. The volatility of a portfolio of 100% Addison stock is 25 %. (Round to two decimal places.) b. The volatility of a portfolio...

(%) P11-11 (similar to) Suppose Wesley Publishing's stock has a volatility of 40%, while Addison Printing's stock has a volatility of 25%. If the correlation between these stocks is 40%, what is the volatility of the following portfolios of Addison and Wesley: a. 100% Addison b, 75% Addison and 25% Wesley c.50% Addison and 50% Wesley a. The volatility of a portfolio of 100% Addison stock is 25 %. (Round to two decimal places.) b. The volatility of a portfolio...

Score: 0 of 1 pt 11 of 12 (4 complete) HW Score: 33.33%, 4 of 12...

Score: 0 of 1 pt 11 of 12 (4 complete) HW Score: 33.33%, 4 of 12 pts P 11-25 (similar to) : Question Help Consider the following 6 months of returns for 2 stocks and a portfolio of those 2 stocks: Note: The portfolio is composed of 50% of Stock A and 50% of Stock B. a. What is the expected return and standard deviation of returns for each of the two stocks? b. What is the expected return and...

Score: 0 of 1 pt 11 of 12 (4 complete) HW Score: 33.33%, 4 of 12 pts P 11-25 (similar to) : Question Help Consider the following 6 months of returns for 2 stocks and a portfolio of those 2 stocks: Note: The portfolio is composed of 50% of Stock A and 50% of Stock B. a. What is the expected return and standard deviation of returns for each of the two stocks? b. What is the expected return and...

letter b please You have estimated the following probability distribution of returns for two stocks: Stock...

letter b please

You have estimated the following probability distribution of returns for two stocks: Stock N Stock O Probability 0.20 0.30 Return 8% Probability 0.20 0.30 0.30 Return 26% 12 0.30 0.20 -4 0.20 -4 Calculate the expected rate of return and standard deviation for cach stock If the correlation between the returns on the two stocks is -0.40, calculate the portfolio returm and the standard deviation for portfolios containing 100%, 75 % , 50 % , 25 %...

letter b please

You have estimated the following probability distribution of returns for two stocks: Stock N Stock O Probability 0.20 0.30 Return 8% Probability 0.20 0.30 0.30 Return 26% 12 0.30 0.20 -4 0.20 -4 Calculate the expected rate of return and standard deviation for cach stock If the correlation between the returns on the two stocks is -0.40, calculate the portfolio returm and the standard deviation for portfolios containing 100%, 75 % , 50 % , 25 %...

Outcome Probability .10 .20 UAWN Stock W +2% +18% +9% -12% +8% Stock X +25% +10%...

Outcome Probability .10 .20 UAWN Stock W +2% +18% +9% -12% +8% Stock X +25% +10% +14% +3% -10% .10 a. What is the expected return for each stock? b. What is the standard deviation for each stock? c. What is the correlation between the stocks? d. If you hold a portfolio of the stocks that is weighted 60% W, and 40% X, what is the expected return and standard deviation for the portfolio? e. Assume that Stock X is...

Outcome Probability .10 .20 UAWN Stock W +2% +18% +9% -12% +8% Stock X +25% +10% +14% +3% -10% .10 a. What is the expected return for each stock? b. What is the standard deviation for each stock? c. What is the correlation between the stocks? d. If you hold a portfolio of the stocks that is weighted 60% W, and 40% X, what is the expected return and standard deviation for the portfolio? e. Assume that Stock X is...

Score: 0 of 1 pt 3 of 12 (0 complete) HW Score: 0%, 0 of 12...

Score: 0 of 1 pt 3 of 12 (0 complete) HW Score: 0%, 0 of 12 pts P 12-4 (book/static) Question Help You are considering how to invest part of your retirement savings. You have decided to put $200,000 into three stocks: 50% of the money in GoldFinger (currently $25/share), 25% of the money in Moosehead (currently $80/share), and the remainder in Venture Associates (currently $2/share). Suppose GoldFinger stock goes up to $30/share, Moosehead stock drops to $60/share, and Venture...

Score: 0 of 1 pt 3 of 12 (0 complete) HW Score: 0%, 0 of 12 pts P 12-4 (book/static) Question Help You are considering how to invest part of your retirement savings. You have decided to put $200,000 into three stocks: 50% of the money in GoldFinger (currently $25/share), 25% of the money in Moosehead (currently $80/share), and the remainder in Venture Associates (currently $2/share). Suppose GoldFinger stock goes up to $30/share, Moosehead stock drops to $60/share, and Venture...

Stocks A and B each have an expected return of 12%, a beta of 1.2, and...

Stocks A and B each have an expected return of 12%, a beta of 1.2, and a standard deviation of 25%. The returns on the two stocks have a correlation of 0.6. Portfolio P has 50% in Stock A and 50% in Stock B. Which of the following statements is CORRECT? Portfolio P has a beta that is greater than 1.2. Portfolio P has a standard deviation that is greater than 25%. Portfolio P has an expected return that is...

B. MICFUELUNUML U C. idiosyncratic risk CD. systematic risk 0.5. Which of thes A. II,IV B....

B. MICFUELUNUML U C. idiosyncratic risk CD. systematic risk 0.5. Which of thes A. II,IV B. II,IV.v C. 1,111,1V ck A and Z have a correlation 05 D. 1,111, E. I, 3 Stock A and Stock B have a correlation Correlation-0.7, Stock A and Z have than a portfolio of story are an in is part of market A. Stock A and Z have a stronge CB. A portfolio of stock A and B P C C. Stock A and...

B. MICFUELUNUML U C. idiosyncratic risk CD. systematic risk 0.5. Which of thes A. II,IV B. II,IV.v C. 1,111,1V ck A and Z have a correlation 05 D. 1,111, E. I, 3 Stock A and Stock B have a correlation Correlation-0.7, Stock A and Z have than a portfolio of story are an in is part of market A. Stock A and Z have a stronge CB. A portfolio of stock A and B P C C. Stock A and...

P 12-18 (similar to) 8 You have a portfolio with a standard deviation of 28% and an expected return of 20%. You are...

P 12-18 (similar to) 8 You have a portfolio with a standard deviation of 28% and an expected return of 20%. You are considering adding one of the two stocks in the following table. If after adding the stock you will have 25% of your money in the new stock and 75% of your money in your existing portfolio, which one should you add? Expected Return Standard Correlation with Your Portfolio's Returns Deviation Stock A 16% 21% 0.2 Stock B...

P 12-18 (similar to) 8 You have a portfolio with a standard deviation of 28% and an expected return of 20%. You are considering adding one of the two stocks in the following table. If after adding the stock you will have 25% of your money in the new stock and 75% of your money in your existing portfolio, which one should you add? Expected Return Standard Correlation with Your Portfolio's Returns Deviation Stock A 16% 21% 0.2 Stock B...

Find the STD of the portfolio and round to two decimal places 12 of 17 (8...

Find the STD of the portfolio and round to two decimal places

12 of 17 (8 complete) HW Score: 37%, 37 of 100 pts Score: 0 of 3 pts P 12-10 (similar to) Assigned Media Question Help Using the data in the following table, and the fact that the correlation of A and B is 0.55, calculate the volatility (standard deviation) of a portfolio that is 50% invested in stock A and 50% invested in stock B the sprea Realized...

Find the STD of the portfolio and round to two decimal places

12 of 17 (8 complete) HW Score: 37%, 37 of 100 pts Score: 0 of 3 pts P 12-10 (similar to) Assigned Media Question Help Using the data in the following table, and the fact that the correlation of A and B is 0.55, calculate the volatility (standard deviation) of a portfolio that is 50% invested in stock A and 50% invested in stock B the sprea Realized...

plz solve complete question, all parts. B 12-8 (book/static) Question Help Stocks A and B have...

plz solve complete question, all parts.

B 12-8 (book/static) Question Help Stocks A and B have the following returns: 1 2 3 4 5 Stock A 0.10 0.07 0.15 -0.05 0.08 Stock B 0.06 0.02 0.05 0.01 -0.02 a. What are the expected returns of the two stocks? b. What are the standard deviations of the returns of the two stocks? c. If their correlation is 0.46, what is the expected return and standard deviation of a portfolio of 70%...

plz solve complete question, all parts.

B 12-8 (book/static) Question Help Stocks A and B have the following returns: 1 2 3 4 5 Stock A 0.10 0.07 0.15 -0.05 0.08 Stock B 0.06 0.02 0.05 0.01 -0.02 a. What are the expected returns of the two stocks? b. What are the standard deviations of the returns of the two stocks? c. If their correlation is 0.46, what is the expected return and standard deviation of a portfolio of 70%...

(%) P11-11 (similar to) Suppose Wesley Publishing's stock has a volatility of 40%, while Addison Printing's stock has a volatility of 25%. If the correlation between these stocks is 40%, what is the volatility of the following portfolios of Addison and Wesley: a. 100% Addison b, 75% Addison and 25% Wesley c.50% Addison and 50% Wesley a. The volatility of a portfolio of 100% Addison stock is 25 %. (Round to two decimal places.) b. The volatility of a portfolio...

(%) P11-11 (similar to) Suppose Wesley Publishing's stock has a volatility of 40%, while Addison Printing's stock has a volatility of 25%. If the correlation between these stocks is 40%, what is the volatility of the following portfolios of Addison and Wesley: a. 100% Addison b, 75% Addison and 25% Wesley c.50% Addison and 50% Wesley a. The volatility of a portfolio of 100% Addison stock is 25 %. (Round to two decimal places.) b. The volatility of a portfolio...

Score: 0 of 1 pt 11 of 12 (4 complete) HW Score: 33.33%, 4 of 12 pts P 11-25 (similar to) : Question Help Consider the following 6 months of returns for 2 stocks and a portfolio of those 2 stocks: Note: The portfolio is composed of 50% of Stock A and 50% of Stock B. a. What is the expected return and standard deviation of returns for each of the two stocks? b. What is the expected return and...

Score: 0 of 1 pt 11 of 12 (4 complete) HW Score: 33.33%, 4 of 12 pts P 11-25 (similar to) : Question Help Consider the following 6 months of returns for 2 stocks and a portfolio of those 2 stocks: Note: The portfolio is composed of 50% of Stock A and 50% of Stock B. a. What is the expected return and standard deviation of returns for each of the two stocks? b. What is the expected return and...

letter b please

You have estimated the following probability distribution of returns for two stocks: Stock N Stock O Probability 0.20 0.30 Return 8% Probability 0.20 0.30 0.30 Return 26% 12 0.30 0.20 -4 0.20 -4 Calculate the expected rate of return and standard deviation for cach stock If the correlation between the returns on the two stocks is -0.40, calculate the portfolio returm and the standard deviation for portfolios containing 100%, 75 % , 50 % , 25 %...

letter b please

You have estimated the following probability distribution of returns for two stocks: Stock N Stock O Probability 0.20 0.30 Return 8% Probability 0.20 0.30 0.30 Return 26% 12 0.30 0.20 -4 0.20 -4 Calculate the expected rate of return and standard deviation for cach stock If the correlation between the returns on the two stocks is -0.40, calculate the portfolio returm and the standard deviation for portfolios containing 100%, 75 % , 50 % , 25 %...

Outcome Probability .10 .20 UAWN Stock W +2% +18% +9% -12% +8% Stock X +25% +10% +14% +3% -10% .10 a. What is the expected return for each stock? b. What is the standard deviation for each stock? c. What is the correlation between the stocks? d. If you hold a portfolio of the stocks that is weighted 60% W, and 40% X, what is the expected return and standard deviation for the portfolio? e. Assume that Stock X is...

Outcome Probability .10 .20 UAWN Stock W +2% +18% +9% -12% +8% Stock X +25% +10% +14% +3% -10% .10 a. What is the expected return for each stock? b. What is the standard deviation for each stock? c. What is the correlation between the stocks? d. If you hold a portfolio of the stocks that is weighted 60% W, and 40% X, what is the expected return and standard deviation for the portfolio? e. Assume that Stock X is...

Score: 0 of 1 pt 3 of 12 (0 complete) HW Score: 0%, 0 of 12 pts P 12-4 (book/static) Question Help You are considering how to invest part of your retirement savings. You have decided to put $200,000 into three stocks: 50% of the money in GoldFinger (currently $25/share), 25% of the money in Moosehead (currently $80/share), and the remainder in Venture Associates (currently $2/share). Suppose GoldFinger stock goes up to $30/share, Moosehead stock drops to $60/share, and Venture...

Score: 0 of 1 pt 3 of 12 (0 complete) HW Score: 0%, 0 of 12 pts P 12-4 (book/static) Question Help You are considering how to invest part of your retirement savings. You have decided to put $200,000 into three stocks: 50% of the money in GoldFinger (currently $25/share), 25% of the money in Moosehead (currently $80/share), and the remainder in Venture Associates (currently $2/share). Suppose GoldFinger stock goes up to $30/share, Moosehead stock drops to $60/share, and Venture...

B. MICFUELUNUML U C. idiosyncratic risk CD. systematic risk 0.5. Which of thes A. II,IV B. II,IV.v C. 1,111,1V ck A and Z have a correlation 05 D. 1,111, E. I, 3 Stock A and Stock B have a correlation Correlation-0.7, Stock A and Z have than a portfolio of story are an in is part of market A. Stock A and Z have a stronge CB. A portfolio of stock A and B P C C. Stock A and...

B. MICFUELUNUML U C. idiosyncratic risk CD. systematic risk 0.5. Which of thes A. II,IV B. II,IV.v C. 1,111,1V ck A and Z have a correlation 05 D. 1,111, E. I, 3 Stock A and Stock B have a correlation Correlation-0.7, Stock A and Z have than a portfolio of story are an in is part of market A. Stock A and Z have a stronge CB. A portfolio of stock A and B P C C. Stock A and...

P 12-18 (similar to) 8 You have a portfolio with a standard deviation of 28% and an expected return of 20%. You are considering adding one of the two stocks in the following table. If after adding the stock you will have 25% of your money in the new stock and 75% of your money in your existing portfolio, which one should you add? Expected Return Standard Correlation with Your Portfolio's Returns Deviation Stock A 16% 21% 0.2 Stock B...

P 12-18 (similar to) 8 You have a portfolio with a standard deviation of 28% and an expected return of 20%. You are considering adding one of the two stocks in the following table. If after adding the stock you will have 25% of your money in the new stock and 75% of your money in your existing portfolio, which one should you add? Expected Return Standard Correlation with Your Portfolio's Returns Deviation Stock A 16% 21% 0.2 Stock B...

Find the STD of the portfolio and round to two decimal places

12 of 17 (8 complete) HW Score: 37%, 37 of 100 pts Score: 0 of 3 pts P 12-10 (similar to) Assigned Media Question Help Using the data in the following table, and the fact that the correlation of A and B is 0.55, calculate the volatility (standard deviation) of a portfolio that is 50% invested in stock A and 50% invested in stock B the sprea Realized...

Find the STD of the portfolio and round to two decimal places

12 of 17 (8 complete) HW Score: 37%, 37 of 100 pts Score: 0 of 3 pts P 12-10 (similar to) Assigned Media Question Help Using the data in the following table, and the fact that the correlation of A and B is 0.55, calculate the volatility (standard deviation) of a portfolio that is 50% invested in stock A and 50% invested in stock B the sprea Realized...

plz solve complete question, all parts.

B 12-8 (book/static) Question Help Stocks A and B have the following returns: 1 2 3 4 5 Stock A 0.10 0.07 0.15 -0.05 0.08 Stock B 0.06 0.02 0.05 0.01 -0.02 a. What are the expected returns of the two stocks? b. What are the standard deviations of the returns of the two stocks? c. If their correlation is 0.46, what is the expected return and standard deviation of a portfolio of 70%...

plz solve complete question, all parts.

B 12-8 (book/static) Question Help Stocks A and B have the following returns: 1 2 3 4 5 Stock A 0.10 0.07 0.15 -0.05 0.08 Stock B 0.06 0.02 0.05 0.01 -0.02 a. What are the expected returns of the two stocks? b. What are the standard deviations of the returns of the two stocks? c. If their correlation is 0.46, what is the expected return and standard deviation of a portfolio of 70%...

Most questions answered within 3 hours.

-

In C++ Programming, Try using loops only.

This lab demonstrates the use of the While Loop...

asked 33 minutes ago -

Effect of DCMU and sodium azide on Chlamydomonas? We did an

experiment where we had Chlamydomonas...

asked 1 hour ago -

1a) According to the ideal gas law, _______________.

a. a gas has infinite volume at absolute...

asked 2 hours ago -

Oakdale Fashions, Inc. had $245,000 in 2018 taxable income.

Using the tax schedule in Table 2.3...

asked 3 hours ago -

The marketing class at CSUS had an average score of 150. An

educational analyst determined that...

asked 4 hours ago -

Justin Case has purchased a $250 000 home by putting 20 % down

and taking out...

asked 4 hours ago -

1. In a labor market, marginal cost for a firm is

____________.

a. recruiting cost

b....

asked 5 hours ago -

On January 1, 2019, ABC Company issued $60,000,000 of 20-year,

10.5% bonds when the market rate...

asked 5 hours ago -

39.4% of US homes continue to use a landline in addition to cell

phone service. 3...

asked 6 hours ago -

Starting with benzene, synthesize 1-phenyl-1-butyne.

Show intermediates and reagents.

asked 7 hours ago -

Create a 32-run crossed array design with six control factors

and two noise factors such that...

asked 8 hours ago -

A 500g sample of sand from source A has the following amounts

retained on each sieve....

asked 8 hours ago