Homework Answers

Add Answer to:

1. Consider the following autoregressive process 2+ = 4.0 + 0.8 2t-1 + Ut, where E...

help wih these question please 3. Consider the following autoregressive process Yt = Bo + B1yt-1...

help wih these question please

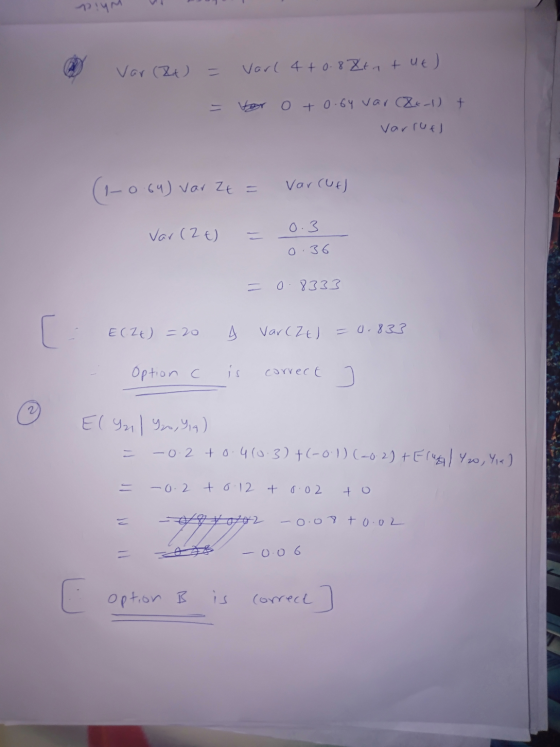

3. Consider the following autoregressive process Yt = Bo + B1yt-1 + B2Yt-2 + Ut, where E (UtYt-1, Yt-2, ...) = 0. You obtained the following parameter estimates: Bo= -0.2, B1 = 0.4 and B2 = -0.1. Furthermore, you have the following observations: 419 = -0.2 and Y20 = 0.3. What is the estimate for E Y 22 y 20,419)? (a) -0.3333 (b) -0.06 (C) 0.3 (d) -0.2857 (e) -0.254 4. You have estimated the...

help wih these question please

3. Consider the following autoregressive process Yt = Bo + B1yt-1 + B2Yt-2 + Ut, where E (UtYt-1, Yt-2, ...) = 0. You obtained the following parameter estimates: Bo= -0.2, B1 = 0.4 and B2 = -0.1. Furthermore, you have the following observations: 419 = -0.2 and Y20 = 0.3. What is the estimate for E Y 22 y 20,419)? (a) -0.3333 (b) -0.06 (C) 0.3 (d) -0.2857 (e) -0.254 4. You have estimated the...

a) Consider the following moving average process, MA(2):

a) Consider the following moving average process, MA(2): Yt = ut + α1ut-1 + α2ut-2 where ut is a white noise process, with E(ut)=0, var(ut)=σ2 and cov(ut,us)=0 . Derive the mean, E(Yt), the variance, var(Yt), and the covariances cov( Yt,Yt+1 ) and cov(Yt,Yt+2 ), of this process. b) Give a definition of a (covariance) stationary time series process. Is the MA(2) process (covariance) stationary?

a) Consider the following moving average process, MA(2): Yt = ut + α1ut-1 + α2ut-2 where ut is a white noise process, with E(ut)=0, var(ut)=σ2 and cov(ut,us)=0 . Derive the mean, E(Yt), the variance, var(Yt), and the covariances cov( Yt,Yt+1 ) and cov(Yt,Yt+2 ), of this process. b) Give a definition of a (covariance) stationary time series process. Is the MA(2) process (covariance) stationary?

Consider the following AR(1) model: 1. a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. the following random 2. Consider walk...

Consider the following AR(1) model: 1. a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. the following random 2. Consider walk model: yeBo yt-1 +ut, t-0,1,..,T a. Show that yt-3βο + yt-3 + ut + ut-1 + ut-2. b. Suppose that 0-0, show that y.-t βο +4 + ut-1 + + u! c. Suppose that that yo -0, and ut for all t are ii.d. with mean 0 and variance...

Consider the following AR(1) model: 1. a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. the following random 2. Consider walk model: yeBo yt-1 +ut, t-0,1,..,T a. Show that yt-3βο + yt-3 + ut + ut-1 + ut-2. b. Suppose that 0-0, show that y.-t βο +4 + ut-1 + + u! c. Suppose that that yo -0, and ut for all t are ii.d. with mean 0 and variance...

2. Consider a following time series process Yt = 1.5Yt−1 −0.5Yt−2 +εt a) Rewrite this process...

2. Consider a following time series process Yt = 1.5Yt−1 −0.5Yt−2 +εt a) Rewrite this process in lag polynomial form. b) Is this process invertible? Is this process covariance stationary? c) Difference this process once and show that ΔYt = Yt −Yt−1 is covariance stationary.

Consider the following assumptions: 1. ?? = ?(? + ??) (data generating process) 2. E(?? )...

Consider the following assumptions: 1. ?? = ?(? + ??) (data generating process) 2. E(?? ) = 0 for all 3. Var(?? ) = ? 2 for all i 4. Cov(?? , ?? ) for ? ≠ ? 5. ?? ∼ ?????? And suppose you’re interested in generating an estimate for ?. a. What is the expected value of the sample mean estimator, ?̂= 1 ? ∑?? , under these assumptions? Is ?̂an unbiased estimator for ?? Show all work...

2. Consider the time series X, = 2 + 0.5t +0.8X1-1 + W, where W N(0.1). (a) (8 points) Calculate E(X2) Is this process weakly stationary? Give reasons for your answer. Hint: Find the mean function of...

2. Consider the time series X, = 2 + 0.5t +0.8X1-1 + W, where W N(0.1). (a) (8 points) Calculate E(X2) Is this process weakly stationary? Give reasons for your answer. Hint: Find the mean function of {X) and then substitute t = 20. (b) (3 points) Calculate Var(X20) Question 2 continues on the next page... Page 4 of 12 c)(4 points) Consider the first differences of the time series above, that is Is {%) a weakly stationary process. Prove...

2. Consider the time series X, = 2 + 0.5t +0.8X1-1 + W, where W N(0.1). (a) (8 points) Calculate E(X2) Is this process weakly stationary? Give reasons for your answer. Hint: Find the mean function of {X) and then substitute t = 20. (b) (3 points) Calculate Var(X20) Question 2 continues on the next page... Page 4 of 12 c)(4 points) Consider the first differences of the time series above, that is Is {%) a weakly stationary process. Prove...

Consider the following network with the initial inputs and outputs i-0.8, irl, i,-0.9 with 0,-01-1 0.3 0.3 0.2 2 0. 0.9...

Consider the following network with the initial inputs and outputs i-0.8, irl, i,-0.9 with 0,-01-1 0.3 0.3 0.2 2 0. 0.9 (04 orm 0. 0.1 2. (Please use matlab) Suppose for above problem, the new inputs and the outputs are as follow: i,-12. 12-3, i,-8 and doー9, di How do you solve the problem with appropriate scaling of the inputs and outputs data sets.

Consider the following network with the initial inputs and outputs i-0.8, irl, i,-0.9 with 0,-01-1 0.3...

Consider the following network with the initial inputs and outputs i-0.8, irl, i,-0.9 with 0,-01-1 0.3 0.3 0.2 2 0. 0.9 (04 orm 0. 0.1 2. (Please use matlab) Suppose for above problem, the new inputs and the outputs are as follow: i,-12. 12-3, i,-8 and doー9, di How do you solve the problem with appropriate scaling of the inputs and outputs data sets.

Consider the following network with the initial inputs and outputs i-0.8, irl, i,-0.9 with 0,-01-1 0.3...

2. (a) Consider the following process: where {Z) is a white noise process with unit variance. [1 ...

2. (a) Consider the following process: where {Z) is a white noise process with unit variance. [1 mark] ii. Find the infinite moving average representation of X,i.e., find the scquence [6 marks] i. Explain why the process is stationary. (6) such that Xt = Σ b,2-j. iii. Calculate the mean and the autocovariance "Yo, γι and 72 of the process. 7 marks iv. Given 40 = 0.1 and Xo = 1.8, find the 2-step ahead forecast of the time series...

2. (a) Consider the following process: where {Z) is a white noise process with unit variance. [1 mark] ii. Find the infinite moving average representation of X,i.e., find the scquence [6 marks] i. Explain why the process is stationary. (6) such that Xt = Σ b,2-j. iii. Calculate the mean and the autocovariance "Yo, γι and 72 of the process. 7 marks iv. Given 40 = 0.1 and Xo = 1.8, find the 2-step ahead forecast of the time series...

Problem 4: Consider the following problem for the heat equation (1) (2) (3) ut= Uxa + s(t), xE (0,1), t > 0 u(0, t)...

Problem 4: Consider the following problem for the heat equation (1) (2) (3) ut= Uxa + s(t), xE (0,1), t > 0 u(0, t) 2, u(1, t) = 4 и (х, 0) — 2(1 — х). where s(t) describes the source term (a) Find a series solution for u(x, t) with s(t) = e"1. (b) What is the convergence criteria for the transient extension function if s(t) = 0.

Problem 4: Consider the following problem for the heat equation (1)...

Problem 4: Consider the following problem for the heat equation (1) (2) (3) ut= Uxa + s(t), xE (0,1), t > 0 u(0, t) 2, u(1, t) = 4 и (х, 0) — 2(1 — х). where s(t) describes the source term (a) Find a series solution for u(x, t) with s(t) = e"1. (b) What is the convergence criteria for the transient extension function if s(t) = 0.

Problem 4: Consider the following problem for the heat equation (1)...

Problem 4: Consider the following problem for the heat equation (1) (2) (3) ut= Uxa + s(t), xE (0,1), t > 0 u(0, t)...

Problem 4: Consider the following problem for the heat equation (1) (2) (3) ut= Uxa + s(t), xE (0,1), t > 0 u(0, t) 2, u(1, t) = 4 и (х, 0) — 2(1 — х). where s(t) describes the source term (a) Find a series solution for u(x, t) with s(t) = e"1. (b) What is the convergence criteria for the transient extension function if s(t) = 0.

Problem 4: Consider the following problem for the heat equation (1)...

Problem 4: Consider the following problem for the heat equation (1) (2) (3) ut= Uxa + s(t), xE (0,1), t > 0 u(0, t) 2, u(1, t) = 4 и (х, 0) — 2(1 — х). where s(t) describes the source term (a) Find a series solution for u(x, t) with s(t) = e"1. (b) What is the convergence criteria for the transient extension function if s(t) = 0.

Problem 4: Consider the following problem for the heat equation (1)...

help wih these question please

3. Consider the following autoregressive process Yt = Bo + B1yt-1 + B2Yt-2 + Ut, where E (UtYt-1, Yt-2, ...) = 0. You obtained the following parameter estimates: Bo= -0.2, B1 = 0.4 and B2 = -0.1. Furthermore, you have the following observations: 419 = -0.2 and Y20 = 0.3. What is the estimate for E Y 22 y 20,419)? (a) -0.3333 (b) -0.06 (C) 0.3 (d) -0.2857 (e) -0.254 4. You have estimated the...

help wih these question please

3. Consider the following autoregressive process Yt = Bo + B1yt-1 + B2Yt-2 + Ut, where E (UtYt-1, Yt-2, ...) = 0. You obtained the following parameter estimates: Bo= -0.2, B1 = 0.4 and B2 = -0.1. Furthermore, you have the following observations: 419 = -0.2 and Y20 = 0.3. What is the estimate for E Y 22 y 20,419)? (a) -0.3333 (b) -0.06 (C) 0.3 (d) -0.2857 (e) -0.254 4. You have estimated the...

Consider the following AR(1) model: 1. a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. the following random 2. Consider walk model: yeBo yt-1 +ut, t-0,1,..,T a. Show that yt-3βο + yt-3 + ut + ut-1 + ut-2. b. Suppose that 0-0, show that y.-t βο +4 + ut-1 + + u! c. Suppose that that yo -0, and ut for all t are ii.d. with mean 0 and variance...

Consider the following AR(1) model: 1. a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. the following random 2. Consider walk model: yeBo yt-1 +ut, t-0,1,..,T a. Show that yt-3βο + yt-3 + ut + ut-1 + ut-2. b. Suppose that 0-0, show that y.-t βο +4 + ut-1 + + u! c. Suppose that that yo -0, and ut for all t are ii.d. with mean 0 and variance...

2. Consider the time series X, = 2 + 0.5t +0.8X1-1 + W, where W N(0.1). (a) (8 points) Calculate E(X2) Is this process weakly stationary? Give reasons for your answer. Hint: Find the mean function of {X) and then substitute t = 20. (b) (3 points) Calculate Var(X20) Question 2 continues on the next page... Page 4 of 12 c)(4 points) Consider the first differences of the time series above, that is Is {%) a weakly stationary process. Prove...

2. Consider the time series X, = 2 + 0.5t +0.8X1-1 + W, where W N(0.1). (a) (8 points) Calculate E(X2) Is this process weakly stationary? Give reasons for your answer. Hint: Find the mean function of {X) and then substitute t = 20. (b) (3 points) Calculate Var(X20) Question 2 continues on the next page... Page 4 of 12 c)(4 points) Consider the first differences of the time series above, that is Is {%) a weakly stationary process. Prove...

Consider the following network with the initial inputs and outputs i-0.8, irl, i,-0.9 with 0,-01-1 0.3 0.3 0.2 2 0. 0.9 (04 orm 0. 0.1 2. (Please use matlab) Suppose for above problem, the new inputs and the outputs are as follow: i,-12. 12-3, i,-8 and doー9, di How do you solve the problem with appropriate scaling of the inputs and outputs data sets.

Consider the following network with the initial inputs and outputs i-0.8, irl, i,-0.9 with 0,-01-1 0.3...

Consider the following network with the initial inputs and outputs i-0.8, irl, i,-0.9 with 0,-01-1 0.3 0.3 0.2 2 0. 0.9 (04 orm 0. 0.1 2. (Please use matlab) Suppose for above problem, the new inputs and the outputs are as follow: i,-12. 12-3, i,-8 and doー9, di How do you solve the problem with appropriate scaling of the inputs and outputs data sets.

Consider the following network with the initial inputs and outputs i-0.8, irl, i,-0.9 with 0,-01-1 0.3...

2. (a) Consider the following process: where {Z) is a white noise process with unit variance. [1 mark] ii. Find the infinite moving average representation of X,i.e., find the scquence [6 marks] i. Explain why the process is stationary. (6) such that Xt = Σ b,2-j. iii. Calculate the mean and the autocovariance "Yo, γι and 72 of the process. 7 marks iv. Given 40 = 0.1 and Xo = 1.8, find the 2-step ahead forecast of the time series...

2. (a) Consider the following process: where {Z) is a white noise process with unit variance. [1 mark] ii. Find the infinite moving average representation of X,i.e., find the scquence [6 marks] i. Explain why the process is stationary. (6) such that Xt = Σ b,2-j. iii. Calculate the mean and the autocovariance "Yo, γι and 72 of the process. 7 marks iv. Given 40 = 0.1 and Xo = 1.8, find the 2-step ahead forecast of the time series...

Problem 4: Consider the following problem for the heat equation (1) (2) (3) ut= Uxa + s(t), xE (0,1), t > 0 u(0, t) 2, u(1, t) = 4 и (х, 0) — 2(1 — х). where s(t) describes the source term (a) Find a series solution for u(x, t) with s(t) = e"1. (b) What is the convergence criteria for the transient extension function if s(t) = 0.

Problem 4: Consider the following problem for the heat equation (1)...

Problem 4: Consider the following problem for the heat equation (1) (2) (3) ut= Uxa + s(t), xE (0,1), t > 0 u(0, t) 2, u(1, t) = 4 и (х, 0) — 2(1 — х). where s(t) describes the source term (a) Find a series solution for u(x, t) with s(t) = e"1. (b) What is the convergence criteria for the transient extension function if s(t) = 0.

Problem 4: Consider the following problem for the heat equation (1)...

Problem 4: Consider the following problem for the heat equation (1) (2) (3) ut= Uxa + s(t), xE (0,1), t > 0 u(0, t) 2, u(1, t) = 4 и (х, 0) — 2(1 — х). where s(t) describes the source term (a) Find a series solution for u(x, t) with s(t) = e"1. (b) What is the convergence criteria for the transient extension function if s(t) = 0.

Problem 4: Consider the following problem for the heat equation (1)...

Problem 4: Consider the following problem for the heat equation (1) (2) (3) ut= Uxa + s(t), xE (0,1), t > 0 u(0, t) 2, u(1, t) = 4 и (х, 0) — 2(1 — х). where s(t) describes the source term (a) Find a series solution for u(x, t) with s(t) = e"1. (b) What is the convergence criteria for the transient extension function if s(t) = 0.

Problem 4: Consider the following problem for the heat equation (1)...

Most questions answered within 3 hours.

-

26) Briefly describe, using words or simple diagrams, the

chemiosmotic theory for coupling oxidation to phosphorylation...

asked 1 hour ago -

Suppose that XX is a random variable with mean 16 and standard

deviation 5 . Also...

asked 1 hour ago -

Calculate the number density of argon gas at a temperature of

24C and a pressure of...

asked 5 hours ago -

Alternative

Classification

How to Estimate

Probabilities from Data? ( For continuous Attributes)

And How to generate...

asked 5 hours ago -

An explosion breaks a 20.0-kg object into three parts. The

object is initially moving at a...

asked 6 hours ago -

Calculate the approximate number of residues of Rubisco, which

is involved in carbon fixation in plants,...

asked 7 hours ago -

Other decisions about scientific claims can have a much broader

impact.ENERGYarrow-10x10.png, environment, health, security - all...

asked 7 hours ago -

I need to write a research paper and work cited about this

topic: The United States...

asked 8 hours ago -

Hello! I was wondering if I could have some help?

If the vapor pressure of carvone...

asked 8 hours ago -

An economist wants to estimate the mean per capita income (in

thousands of dollars) for a...

asked 9 hours ago -

What would be the input/output characteristic of a circuit

obtained by putting two of your 2's-complementers...

asked 8 hours ago -

In Drosophila, the transition from the syncytial blastoderm

stage to the cellular blastoderm stage is a...

asked 9 hours ago