Homework Answers

Add Answer to:

Consider the following AR(1) model: 1. a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. the following random 2. Consider walk...

Consider the following model 1. Consider the following AR(1) model: a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. b. Show th...

Consider the following

model

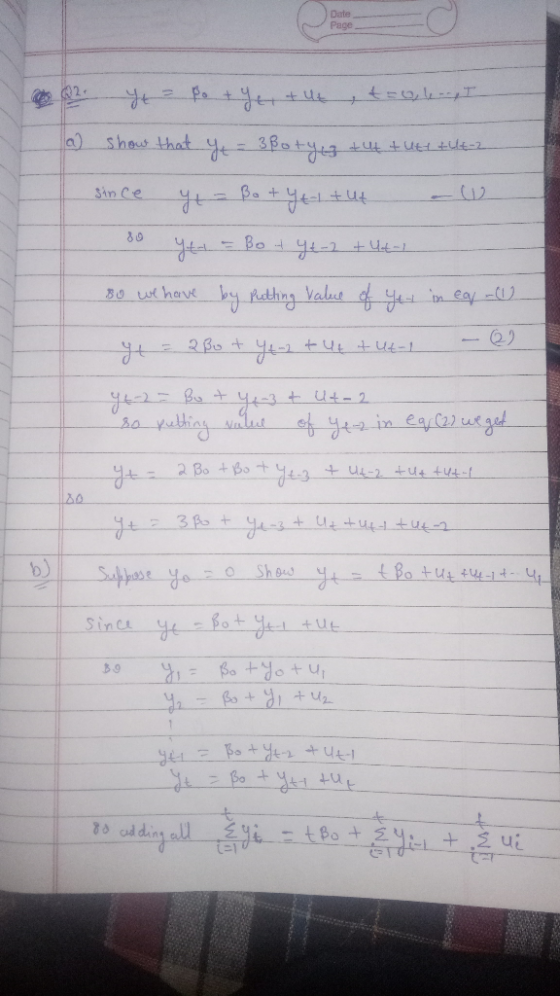

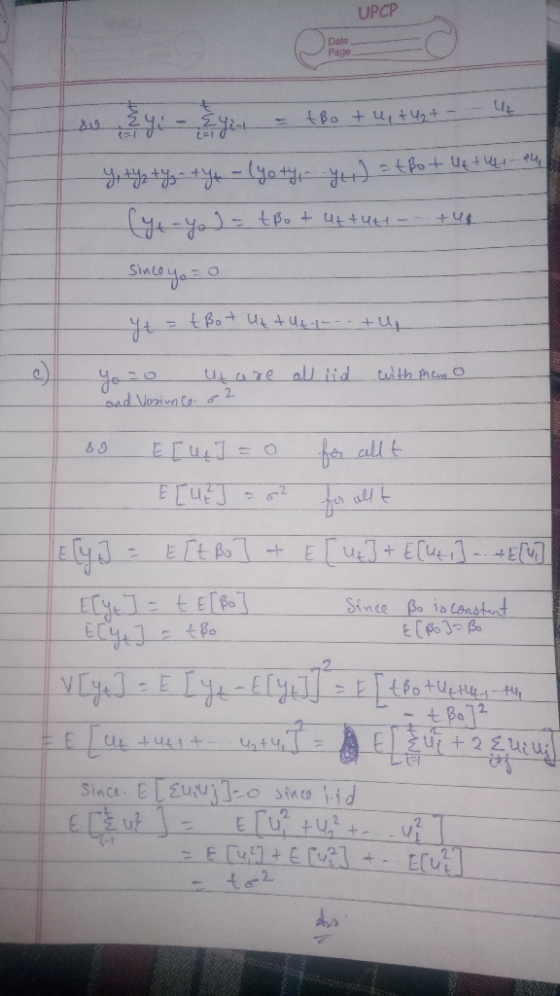

1. Consider the following AR(1) model: a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. b. Show that 1 t-2 2. Consider the following random walk model: ytBo yt-1 +ut, t 0,1,...,T Show that ye 3o yt-3 + ut + Ut-1 +t-2 Suppose that yo - 0, show that yt - tPo + ut + ut-1++u, Suppose that that yo -0, and ut for all t...

Consider the following

model

1. Consider the following AR(1) model: a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. b. Show that 1 t-2 2. Consider the following random walk model: ytBo yt-1 +ut, t 0,1,...,T Show that ye 3o yt-3 + ut + Ut-1 +t-2 Suppose that yo - 0, show that yt - tPo + ut + ut-1++u, Suppose that that yo -0, and ut for all t...

1. (20 points) Consider the linear regression model y = a + Bt + ut, ut...

1. (20 points) Consider the linear regression model y = a + Bt + ut, ut id(0,%), (t = 1, ...,T). An estimator of B is b=1-1 YT- 41 (a) is estimator b consistent? (Hint: use Chebyshev's inequality) (b) If u i.i.d. N(0,1), what is the asymptotic distribution of b?

1. (20 points) Consider the linear regression model y = a + Bt + ut, ut id(0,%), (t = 1, ...,T). An estimator of B is b=1-1 YT- 41 (a) is estimator b consistent? (Hint: use Chebyshev's inequality) (b) If u i.i.d. N(0,1), what is the asymptotic distribution of b?

Consider the following simple regression model: a. Suppose that OLS assumptions 1 to 4 hold true. We know that homoskedasticity assumption is statedas: Var[UjIx] = σ2 for all i Now, suppose that...

Consider the following simple regression model: a. Suppose that OLS assumptions 1 to 4 hold true. We know that homoskedasticity assumption is statedas: Var[UjIx] = σ2 for all i Now, suppose that homoskedasticity does not hold. Mathematically, this is expressed as In other words, the subscript i in σ12 means that the conditional variance of errors for each individual i is different. Under heteroskedasticity, we can derive the expression for the variance of Var(B) as SST Where SSTx is the...

Consider the following simple regression model: a. Suppose that OLS assumptions 1 to 4 hold true. We know that homoskedasticity assumption is statedas: Var[UjIx] = σ2 for all i Now, suppose that homoskedasticity does not hold. Mathematically, this is expressed as In other words, the subscript i in σ12 means that the conditional variance of errors for each individual i is different. Under heteroskedasticity, we can derive the expression for the variance of Var(B) as SST Where SSTx is the...

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1)....

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1). (a) Show that X+ is causal. (b) Find the first four coefficients (VO, ..., 43) of the MA(0) representation of Xt. (c) Find the pacf at lag 3, 233, of the AR(2) model.

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1). (a) Show that X+ is causal. (b) Find the first four coefficients (VO, ..., 43) of the MA(0) representation of Xt. (c) Find the pacf at lag 3, 233, of the AR(2) model.

Question 2 (10 points) You are given the following model y-put ei. Consider two alternative estimators of β, b2xvix? and b = Zy/X 1. Which estimator would you choose and why if the model satisfies al...

Question 2 (10 points) You are given the following model y-put ei. Consider two alternative estimators of β, b2xvix? and b = Zy/X 1. Which estimator would you choose and why if the model satisfies all the assumptions of classical regression? Prove your results. (4 points) 2. Now suppose that var(y)-hxi, where h is a positive constant (a) Obtain the correct variance of the OLS estimator. (2 points) (b) Show that the BLU estimator is now 6. Derive its variance....

Question 2 (10 points) You are given the following model y-put ei. Consider two alternative estimators of β, b2xvix? and b = Zy/X 1. Which estimator would you choose and why if the model satisfies all the assumptions of classical regression? Prove your results. (4 points) 2. Now suppose that var(y)-hxi, where h is a positive constant (a) Obtain the correct variance of the OLS estimator. (2 points) (b) Show that the BLU estimator is now 6. Derive its variance....

1. Consider the following unobserved effects regression model: Suppose that the idiosyncratic error u, t 1,..,T...

1. Consider the following unobserved effects regression model: Suppose that the idiosyncratic error u, t 1,..,T are serially correlated with constant variance σ2. Show that the correlation between adjacent differences, Δυ" and Δυ,-l is -0.5. Therefore under the ideal FE assumptions, first differencing induces negative serial correlation of a known value. [Note:

1. Consider the following unobserved effects regression model: Suppose that the idiosyncratic error u, t 1,..,T are serially correlated with constant variance σ2. Show that the correlation between adjacent differences, Δυ" and Δυ,-l is -0.5. Therefore under the ideal FE assumptions, first differencing induces negative serial correlation of a known value. [Note:

(1) Suppose that we observe data for Treasury Bill rates that are characterized by an AR(3)...

(1) Suppose that we observe data for Treasury Bill rates that are characterized by an AR(3) model, where u is iid, so that E(u,|y-1, y-2)0. We observe data monthly data from 1979 to November of 2018, so that T- 479 observations. Find the forecast for Decem mber of 2018. That is, find E(yT+1VT,Vr-1, yT-2, . . .). Your solution will depend on all the parameters and the observed data. Show your work. (Imenth cheed) (b) Find the forecast for January...

(1) Suppose that we observe data for Treasury Bill rates that are characterized by an AR(3) model, where u is iid, so that E(u,|y-1, y-2)0. We observe data monthly data from 1979 to November of 2018, so that T- 479 observations. Find the forecast for Decem mber of 2018. That is, find E(yT+1VT,Vr-1, yT-2, . . .). Your solution will depend on all the parameters and the observed data. Show your work. (Imenth cheed) (b) Find the forecast for January...

1. A simple dynamic programming model of capital accumulation Consider the following economy. Individuals have preferences...

1. A simple dynamic programming model of capital accumulation Consider the following economy. Individuals have preferences U Blog (ct) and a constraint of the form (a) Write the Bellman equation for this economy. (b) Find the FOC(s) that must be satisfied for an optimal consumption and capital plan. (c) Show the following consumption policy is consistent with the condition(s) that you produced in (b). objective. Show that it takes the form and determine the values of γ and θ. (d)...

1. A simple dynamic programming model of capital accumulation Consider the following economy. Individuals have preferences U Blog (ct) and a constraint of the form (a) Write the Bellman equation for this economy. (b) Find the FOC(s) that must be satisfied for an optimal consumption and capital plan. (c) Show the following consumption policy is consistent with the condition(s) that you produced in (b). objective. Show that it takes the form and determine the values of γ and θ. (d)...

QUESTION4 (a) Let e be a zero-mean, unit-variance white noise process. Consider a process that begins...

QUESTION4 (a) Let e be a zero-mean, unit-variance white noise process. Consider a process that begins at time t = 0 and is defined recursively as follows. Let Y0 = ceo and Y1-CgY0-ei. Then let Y,-φ1Yt-it wt-1-et for t > ï as in an AR(2) process. Show that the process mean, E(Y.), is zero. (b) Suppose that (a is generated according to }.-10 e,-tet-+扣-1 with e,-N(0.) 0 Find the mean and covariance functions for (Y). Is (Y) stationary? Justify your...

QUESTION4 (a) Let e be a zero-mean, unit-variance white noise process. Consider a process that begins at time t = 0 and is defined recursively as follows. Let Y0 = ceo and Y1-CgY0-ei. Then let Y,-φ1Yt-it wt-1-et for t > ï as in an AR(2) process. Show that the process mean, E(Y.), is zero. (b) Suppose that (a is generated according to }.-10 e,-tet-+扣-1 with e,-N(0.) 0 Find the mean and covariance functions for (Y). Is (Y) stationary? Justify your...

Suppose assumptions SLR.1-SLR.3 are satisfied and consider a regression model of savings (sav) on income (inc):...

Suppose assumptions SLR.1-SLR.3 are satisfied and consider a regression model of savings (sav) on income (inc): inc2 xe B1inc + u, where u = Bo sav = Suppose e is a random variable with the following properties: E(einc) 0 Var(elinc) a) Does this regression satisfy the zero conditional mean b) Does this regression satisfy the homoskedasticity assumption (SLR.5)? c) In the real world, why might the variance of savings depend on income? assumption (SLR.4)?

Suppose assumptions SLR.1-SLR.3 are satisfied and consider a regression model of savings (sav) on income (inc): inc2 xe B1inc + u, where u = Bo sav = Suppose e is a random variable with the following properties: E(einc) 0 Var(elinc) a) Does this regression satisfy the zero conditional mean b) Does this regression satisfy the homoskedasticity assumption (SLR.5)? c) In the real world, why might the variance of savings depend on income? assumption (SLR.4)?

Consider the following

model

1. Consider the following AR(1) model: a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. b. Show that 1 t-2 2. Consider the following random walk model: ytBo yt-1 +ut, t 0,1,...,T Show that ye 3o yt-3 + ut + Ut-1 +t-2 Suppose that yo - 0, show that yt - tPo + ut + ut-1++u, Suppose that that yo -0, and ut for all t...

Consider the following

model

1. Consider the following AR(1) model: a. Explain why this dynamic model violates TS'3 ZCM assumption made for the unbiasedness of the FDL model estimators. b. Show that 1 t-2 2. Consider the following random walk model: ytBo yt-1 +ut, t 0,1,...,T Show that ye 3o yt-3 + ut + Ut-1 +t-2 Suppose that yo - 0, show that yt - tPo + ut + ut-1++u, Suppose that that yo -0, and ut for all t...

1. (20 points) Consider the linear regression model y = a + Bt + ut, ut id(0,%), (t = 1, ...,T). An estimator of B is b=1-1 YT- 41 (a) is estimator b consistent? (Hint: use Chebyshev's inequality) (b) If u i.i.d. N(0,1), what is the asymptotic distribution of b?

1. (20 points) Consider the linear regression model y = a + Bt + ut, ut id(0,%), (t = 1, ...,T). An estimator of B is b=1-1 YT- 41 (a) is estimator b consistent? (Hint: use Chebyshev's inequality) (b) If u i.i.d. N(0,1), what is the asymptotic distribution of b?

Consider the following simple regression model: a. Suppose that OLS assumptions 1 to 4 hold true. We know that homoskedasticity assumption is statedas: Var[UjIx] = σ2 for all i Now, suppose that homoskedasticity does not hold. Mathematically, this is expressed as In other words, the subscript i in σ12 means that the conditional variance of errors for each individual i is different. Under heteroskedasticity, we can derive the expression for the variance of Var(B) as SST Where SSTx is the...

Consider the following simple regression model: a. Suppose that OLS assumptions 1 to 4 hold true. We know that homoskedasticity assumption is statedas: Var[UjIx] = σ2 for all i Now, suppose that homoskedasticity does not hold. Mathematically, this is expressed as In other words, the subscript i in σ12 means that the conditional variance of errors for each individual i is different. Under heteroskedasticity, we can derive the expression for the variance of Var(B) as SST Where SSTx is the...

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1). (a) Show that X+ is causal. (b) Find the first four coefficients (VO, ..., 43) of the MA(0) representation of Xt. (c) Find the pacf at lag 3, 233, of the AR(2) model.

Consider the following AR(2) model: Xt – Xt–1 + + X4-2 = Zt, Z4 ~ WN(0,1). (a) Show that X+ is causal. (b) Find the first four coefficients (VO, ..., 43) of the MA(0) representation of Xt. (c) Find the pacf at lag 3, 233, of the AR(2) model.

Question 2 (10 points) You are given the following model y-put ei. Consider two alternative estimators of β, b2xvix? and b = Zy/X 1. Which estimator would you choose and why if the model satisfies all the assumptions of classical regression? Prove your results. (4 points) 2. Now suppose that var(y)-hxi, where h is a positive constant (a) Obtain the correct variance of the OLS estimator. (2 points) (b) Show that the BLU estimator is now 6. Derive its variance....

Question 2 (10 points) You are given the following model y-put ei. Consider two alternative estimators of β, b2xvix? and b = Zy/X 1. Which estimator would you choose and why if the model satisfies all the assumptions of classical regression? Prove your results. (4 points) 2. Now suppose that var(y)-hxi, where h is a positive constant (a) Obtain the correct variance of the OLS estimator. (2 points) (b) Show that the BLU estimator is now 6. Derive its variance....

1. Consider the following unobserved effects regression model: Suppose that the idiosyncratic error u, t 1,..,T are serially correlated with constant variance σ2. Show that the correlation between adjacent differences, Δυ" and Δυ,-l is -0.5. Therefore under the ideal FE assumptions, first differencing induces negative serial correlation of a known value. [Note:

1. Consider the following unobserved effects regression model: Suppose that the idiosyncratic error u, t 1,..,T are serially correlated with constant variance σ2. Show that the correlation between adjacent differences, Δυ" and Δυ,-l is -0.5. Therefore under the ideal FE assumptions, first differencing induces negative serial correlation of a known value. [Note:

(1) Suppose that we observe data for Treasury Bill rates that are characterized by an AR(3) model, where u is iid, so that E(u,|y-1, y-2)0. We observe data monthly data from 1979 to November of 2018, so that T- 479 observations. Find the forecast for Decem mber of 2018. That is, find E(yT+1VT,Vr-1, yT-2, . . .). Your solution will depend on all the parameters and the observed data. Show your work. (Imenth cheed) (b) Find the forecast for January...

(1) Suppose that we observe data for Treasury Bill rates that are characterized by an AR(3) model, where u is iid, so that E(u,|y-1, y-2)0. We observe data monthly data from 1979 to November of 2018, so that T- 479 observations. Find the forecast for Decem mber of 2018. That is, find E(yT+1VT,Vr-1, yT-2, . . .). Your solution will depend on all the parameters and the observed data. Show your work. (Imenth cheed) (b) Find the forecast for January...

1. A simple dynamic programming model of capital accumulation Consider the following economy. Individuals have preferences U Blog (ct) and a constraint of the form (a) Write the Bellman equation for this economy. (b) Find the FOC(s) that must be satisfied for an optimal consumption and capital plan. (c) Show the following consumption policy is consistent with the condition(s) that you produced in (b). objective. Show that it takes the form and determine the values of γ and θ. (d)...

1. A simple dynamic programming model of capital accumulation Consider the following economy. Individuals have preferences U Blog (ct) and a constraint of the form (a) Write the Bellman equation for this economy. (b) Find the FOC(s) that must be satisfied for an optimal consumption and capital plan. (c) Show the following consumption policy is consistent with the condition(s) that you produced in (b). objective. Show that it takes the form and determine the values of γ and θ. (d)...

QUESTION4 (a) Let e be a zero-mean, unit-variance white noise process. Consider a process that begins at time t = 0 and is defined recursively as follows. Let Y0 = ceo and Y1-CgY0-ei. Then let Y,-φ1Yt-it wt-1-et for t > ï as in an AR(2) process. Show that the process mean, E(Y.), is zero. (b) Suppose that (a is generated according to }.-10 e,-tet-+扣-1 with e,-N(0.) 0 Find the mean and covariance functions for (Y). Is (Y) stationary? Justify your...

QUESTION4 (a) Let e be a zero-mean, unit-variance white noise process. Consider a process that begins at time t = 0 and is defined recursively as follows. Let Y0 = ceo and Y1-CgY0-ei. Then let Y,-φ1Yt-it wt-1-et for t > ï as in an AR(2) process. Show that the process mean, E(Y.), is zero. (b) Suppose that (a is generated according to }.-10 e,-tet-+扣-1 with e,-N(0.) 0 Find the mean and covariance functions for (Y). Is (Y) stationary? Justify your...

Suppose assumptions SLR.1-SLR.3 are satisfied and consider a regression model of savings (sav) on income (inc): inc2 xe B1inc + u, where u = Bo sav = Suppose e is a random variable with the following properties: E(einc) 0 Var(elinc) a) Does this regression satisfy the zero conditional mean b) Does this regression satisfy the homoskedasticity assumption (SLR.5)? c) In the real world, why might the variance of savings depend on income? assumption (SLR.4)?

Suppose assumptions SLR.1-SLR.3 are satisfied and consider a regression model of savings (sav) on income (inc): inc2 xe B1inc + u, where u = Bo sav = Suppose e is a random variable with the following properties: E(einc) 0 Var(elinc) a) Does this regression satisfy the zero conditional mean b) Does this regression satisfy the homoskedasticity assumption (SLR.5)? c) In the real world, why might the variance of savings depend on income? assumption (SLR.4)?

Most questions answered within 3 hours.

-

An entomologist discovers a dung beetle rolling a ball of dung

along the ground, and decides...

asked 25 minutes ago -

Humans have used horses for transportation for millions of

years. Therefore, they will use horses for...

asked 2 hours ago -

The following are the Jensen Corporation's unit costs of making

and selling an item at a...

asked 2 hours ago -

Does direct Medicare reimbursement of Advanced practice nurses

increase access to their services?

asked 3 hours ago -

List and explain why a company would choose to use a

published

compensation survey vs. creating...

asked 3 hours ago -

A discrete random variable X can take values from 1 to 10. Find

the variance of...

asked 4 hours ago -

The primary financial goal of a corporation is to maximize:

shareholders wealth.

earnings per share.

stock...

asked 4 hours ago -

determine whether the vectors u=(1,2,3,), v=(-2,1,0) and

w=(1,0,1) are linearly dependent or independent.

asked 4 hours ago -

python

Define a function called print_values which takes a dictionary

object as a parameter. The function...

asked 5 hours ago -

In Chapter 1 you created a program named Triangle in

which you displayed a seven-line triangle...

asked 5 hours ago -

Research question: What are the differences between separately

stated and non separately stated transactions in an...

asked 5 hours ago -

By using Arduino write a code that connects two LEDs to two

push-buttons. Each button controls...

asked 6 hours ago