Homework Answers

*Please rate thumbs up

Add Answer to:

You are evaluating a fund that had an annual average return of 7.23%. During that time,...

You are evaluating a fund that had an annual average return of 7.2%. During that time,...

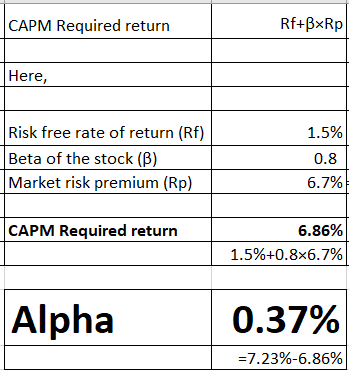

You are evaluating a fund that had an annual average return of 7.2%. During that time, the average risk-free rate was 1.5% and the average market return was 8%. If the fund's beta is 0.8, what was its alpha? Answer in percent, rounded to one decimal place (e.g. 4.32% = 4.3).

What is the CAPM required return of a stock with a beta of 1.2 if the...

What is the CAPM required return of a stock with a beta of 1.2 if the risk-free rate is 1.9% and the expected market risk premium is 5.5%? Answer in percent, rounded to two decimal places. (e.g., 4.32% = 4.32). [Hint: CAPM required return = Risk-free rate + beta x EMRP. Remember order of operations. Multiply beta and EMRP first, then add the risk-free rate]

You have been given the following return information for a mutual fund, the market index, and...

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.95. Risk-Free Year 2011 2012 2013 2014 2015 Fund -19.40% 25.10 13.70 7.20 -1.98 Market -37.50% 20.80 13.30 8.40 -4.20 NON Calculate Jensen's alpha for the fund, as well as its information ratio. (Do not round intermediate calculations. Enter the alpha as a percent rounded to 2...

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.95. Risk-Free Year 2011 2012 2013 2014 2015 Fund -19.40% 25.10 13.70 7.20 -1.98 Market -37.50% 20.80 13.30 8.40 -4.20 NON Calculate Jensen's alpha for the fund, as well as its information ratio. (Do not round intermediate calculations. Enter the alpha as a percent rounded to 2...

Question 15 A mutual fund has earned an annual average return of 15% over the last...

Question 15 A mutual fund has earned an annual average return of 15% over the last 5 years. During that time, the average risk-free rate was 2% and the average market return was 12% per year. The correlation coefficient between the mutual fund’s and market’s returns was 0.7. The standard deviation of returns was 45% for the mutual fund and 22% for the market. What was the fund’s CAPM alpha? a) -2.9% b) -1.3% c) 0.3% d) 1.9% e) 3.5%

You have been given the following return information for a mutual fund, the market index, and...

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.87. Year Fund Market Risk-Free 2011 –14.85 % –29.50 % 3 % 2012 25.10 20.00 5 2013 12.90 10.90 2 2014 7.20 8.00 5 2015 –1.50 –3.20 3 Calculate Jensen’s alpha for the fund, as well as its information ratio. (Do not round intermediate calculations. Enter the...

PORTFOLIO REQUIRED RETURN Suppose you are the money manager of a $5.3 million investment fund. The...

PORTFOLIO REQUIRED RETURN Suppose you are the money manager of a $5.3 million investment fund. The fund consists of four stocks with the following investments and betas: Stock Investment Beta A $ 340,000 1.50 B 760,000 (0.50) C 1,300,000 1.25 D 2,900,000 0.75 If the market's required rate of return is 8% and the risk-free rate is 5%, what is the fund's required rate of return? Do not round intermediate calculations. Round your answer to two decimal places. CAPM AND REQUIRED...

13. An portfolio manager gathered the following information about a fund. Fund's rate of return 20%...

13. An portfolio manager gathered the following information about a fund. Fund's rate of return 20% Market rate of return 11% Risk-free rate 5% Beta of the fund 1.3 The Jensen's alpha for the fund is closest to:

13. An portfolio manager gathered the following information about a fund. Fund's rate of return 20% Market rate of return 11% Risk-free rate 5% Beta of the fund 1.3 The Jensen's alpha for the fund is closest to:

please answer those two questions 1. 2. What is the CAPM required return of a stock...

please answer those two questions

1.

2.

What is the CAPM required return of a stock with a beta of 2.2 if the risk-free rate is 1.5% and the expected market risk premium is 4.8%? Answer in percent, rounded to two decimal places. (e.g., 4.32% = 4.32) Numeric Answer: On Blackboard under "Course Content / Homeworks and Practice Tests" there is an Excel file titled "HW 6 Data" with monthly stock return data to be used for this question: What...

please answer those two questions

1.

2.

What is the CAPM required return of a stock with a beta of 2.2 if the risk-free rate is 1.5% and the expected market risk premium is 4.8%? Answer in percent, rounded to two decimal places. (e.g., 4.32% = 4.32) Numeric Answer: On Blackboard under "Course Content / Homeworks and Practice Tests" there is an Excel file titled "HW 6 Data" with monthly stock return data to be used for this question: What...

1. 2. A stock you are looking at has generated the following annual returns: 10.0%, -5.0%...

1.

2.

A stock you are looking at has generated the following annual returns: 10.0%, -5.0% and 4.0%. What was the standard deviation of its returns? Answer in percent, rounded to two decimal places (e.g., 4.32% = 4.32). Numeric Answer: 11.66 You are incorrect 11.66 A stock has generated an annual average return of 8.0% with a standard deviation of 45.0% during the last 10 years. If the average risk-free rate was 1.6%, what was this stock's Sharpe Ratio? Round...

1.

2.

A stock you are looking at has generated the following annual returns: 10.0%, -5.0% and 4.0%. What was the standard deviation of its returns? Answer in percent, rounded to two decimal places (e.g., 4.32% = 4.32). Numeric Answer: 11.66 You are incorrect 11.66 A stock has generated an annual average return of 8.0% with a standard deviation of 45.0% during the last 10 years. If the average risk-free rate was 1.6%, what was this stock's Sharpe Ratio? Round...

You are an analyst for a large public pension fund and you have been assigned the...

You are an analyst for a large public pension fund and you have been assigned the task of evaluating two different external portfolio managers (Y and Z). You consider the following historical average return, standard deviation, and CAPM beta estimates for these two managers over the past five years: Portfolio Actual Avg. Return Standard Deviation Beta Manager Y 11.00 % 11.80 % 1.30 Manager Z 7.00 % 8.50 % 0.90 Additionally, your estimate for the risk premium for the market...

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.95. Risk-Free Year 2011 2012 2013 2014 2015 Fund -19.40% 25.10 13.70 7.20 -1.98 Market -37.50% 20.80 13.30 8.40 -4.20 NON Calculate Jensen's alpha for the fund, as well as its information ratio. (Do not round intermediate calculations. Enter the alpha as a percent rounded to 2...

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.95. Risk-Free Year 2011 2012 2013 2014 2015 Fund -19.40% 25.10 13.70 7.20 -1.98 Market -37.50% 20.80 13.30 8.40 -4.20 NON Calculate Jensen's alpha for the fund, as well as its information ratio. (Do not round intermediate calculations. Enter the alpha as a percent rounded to 2...

13. An portfolio manager gathered the following information about a fund. Fund's rate of return 20% Market rate of return 11% Risk-free rate 5% Beta of the fund 1.3 The Jensen's alpha for the fund is closest to:

13. An portfolio manager gathered the following information about a fund. Fund's rate of return 20% Market rate of return 11% Risk-free rate 5% Beta of the fund 1.3 The Jensen's alpha for the fund is closest to:

please answer those two questions

1.

2.

What is the CAPM required return of a stock with a beta of 2.2 if the risk-free rate is 1.5% and the expected market risk premium is 4.8%? Answer in percent, rounded to two decimal places. (e.g., 4.32% = 4.32) Numeric Answer: On Blackboard under "Course Content / Homeworks and Practice Tests" there is an Excel file titled "HW 6 Data" with monthly stock return data to be used for this question: What...

please answer those two questions

1.

2.

What is the CAPM required return of a stock with a beta of 2.2 if the risk-free rate is 1.5% and the expected market risk premium is 4.8%? Answer in percent, rounded to two decimal places. (e.g., 4.32% = 4.32) Numeric Answer: On Blackboard under "Course Content / Homeworks and Practice Tests" there is an Excel file titled "HW 6 Data" with monthly stock return data to be used for this question: What...

1.

2.

A stock you are looking at has generated the following annual returns: 10.0%, -5.0% and 4.0%. What was the standard deviation of its returns? Answer in percent, rounded to two decimal places (e.g., 4.32% = 4.32). Numeric Answer: 11.66 You are incorrect 11.66 A stock has generated an annual average return of 8.0% with a standard deviation of 45.0% during the last 10 years. If the average risk-free rate was 1.6%, what was this stock's Sharpe Ratio? Round...

1.

2.

A stock you are looking at has generated the following annual returns: 10.0%, -5.0% and 4.0%. What was the standard deviation of its returns? Answer in percent, rounded to two decimal places (e.g., 4.32% = 4.32). Numeric Answer: 11.66 You are incorrect 11.66 A stock has generated an annual average return of 8.0% with a standard deviation of 45.0% during the last 10 years. If the average risk-free rate was 1.6%, what was this stock's Sharpe Ratio? Round...

Most questions answered within 3 hours.

-

Cash Payback Period

Primera Banco is evaluating two capital investment proposals for

a drive-up ATM kiosk,...

asked 23 seconds ago -

Create a button in Swift (Xcode) that will create a charge,

create a charge using Stripe's...

asked 24 seconds ago -

1A- Why don’t voters complain about U.S. tariffs on imported

sugar?

Because sugar is only a...

asked 2 minutes ago -

The reaction rate of CO and NO2 in the reaction

CO(g) + NO2(g) → CO2(g) +...

asked 1 minute ago -

In

the last 3 months, mike never knows when he is going to get his

allowance...

asked 3 minutes ago -

Imagine that a chemist puts 6.40 mol each of

C3H8 and O2 in a 1.00-L container...

asked 19 minutes ago -

How much money should be invested today in order to have $8340

at the end of...

asked 22 minutes ago -

You are conducting research for a hospital and issue a survey to

patients.

Based on the...

asked 23 minutes ago -

What might be a negative mutation that would hinder the

bug population?

asked 32 minutes ago -

A company just paid a dividend of $1.50 per share. The consensus

forecast of financial analysts...

asked 28 minutes ago -

A mass of 0.50 g of an unknown acid HA required 20.0 mL of 0.25

M...

asked 38 minutes ago -

Mitch is a director and officer of Numero Uno, Inc. Mitch makes

a marketing decision that...

asked 39 minutes ago