Homework Answers

SEE THE IMAGE. ANY DOUBTS, FEEL FREE TO ASK. THUMBS UP

PLEASE

Add Answer to:

You have been given the following return information for a mutual fund, the market index, and...

You have been given the following return information for a mutual fund, the market index, and...

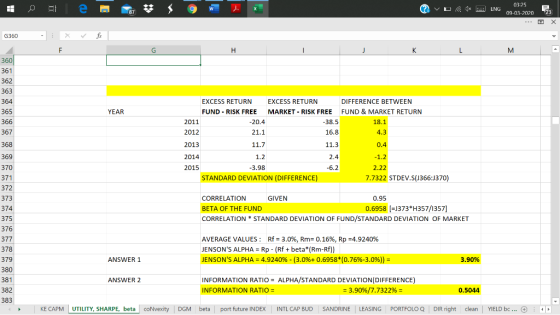

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.87. Year Fund Market Risk-Free 2011 –14.85 % –29.50 % 3 % 2012 25.10 20.00 5 2013 12.90 10.90 2 2014 7.20 8.00 5 2015 –1.50 –3.20 3 Calculate Jensen’s alpha for the fund, as well as its information ratio. (Do not round intermediate calculations. Enter the...

You have been given the following return information for a mutual fund, the market index, and...

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Risk-Free Year 2011 2012 2013 2014 2015 Fund -17.68 25.1 13.4 6.6 -1.8 Market -34.5% 20.5 12.4 8 .4 -4.2 What are the Sharpe and Treynor ratios for the fund? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Sharpe ratio Treynor ratio

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Risk-Free Year 2011 2012 2013 2014 2015 Fund -17.68 25.1 13.4 6.6 -1.8 Market -34.5% 20.5 12.4 8 .4 -4.2 What are the Sharpe and Treynor ratios for the fund? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Sharpe ratio Treynor ratio

You have been given the following return information for a mutual fund, the market index, and...

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97 Risk-F Year 2011 2012 2013 2014 Fund -16.4 25.1 13.2 Market -32.5 20.3 2015 -1.68 What are the Sharpe and Treynor ratios for the fund? (Do not round Intermediate calculations. Round your answers to 4 decimal places.) Sharpe ratio Treynor ratio

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97 Risk-F Year 2011 2012 2013 2014 Fund -16.4 25.1 13.2 Market -32.5 20.3 2015 -1.68 What are the Sharpe and Treynor ratios for the fund? (Do not round Intermediate calculations. Round your answers to 4 decimal places.) Sharpe ratio Treynor ratio

You have been given the following return information for a mutual fund, the market index, and...

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Risk-Free Year 2011 2012 2013 2014 2015 Fund -14.92% 25.1 12.8 7.0 -1.44 Market -28.5% 19.9 10.6 7.6 -2.2 What are the Sharpe and Treynor ratios for the fund? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Answer is complete but not...

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Risk-Free Year 2011 2012 2013 2014 2015 Fund -14.92% 25.1 12.8 7.0 -1.44 Market -28.5% 19.9 10.6 7.6 -2.2 What are the Sharpe and Treynor ratios for the fund? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Answer is complete but not...

8. You have been given the following return information for a mutual fund, the market index,...

8. You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Risk-Free 2% Year 2011 2012 2013 2014 2015 Fund -15.13% 25.1 12.5 6.4 -1.26 Market -25.5% 19.6 9.7 7.6 -2.2 که ن What are the Sharpe and Treynor ratios for the fund? (Do not round intermediate calculations. Round your answers to 4 decimal places.)

8. You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Risk-Free 2% Year 2011 2012 2013 2014 2015 Fund -15.13% 25.1 12.5 6.4 -1.26 Market -25.5% 19.6 9.7 7.6 -2.2 که ن What are the Sharpe and Treynor ratios for the fund? (Do not round intermediate calculations. Round your answers to 4 decimal places.)

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset:...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP 13.0% 12.0 7.0 10.1 5.0 op 30% 25 15 20 Bp 1.30 1.10 0.75 1.00 Market Risk-free 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your ratio answers...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP 13.0% 12.0 7.0 10.1 5.0 op 30% 25 15 20 Bp 1.30 1.10 0.75 1.00 Market Risk-free 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your ratio answers...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset ВР Portfolio Rp 13.0 Оp 39 1.75 х Y 12.0 34 1.30 7.2 24 0.85 Market 11.0 29 1.00 Risk-free 5.6 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset ВР Portfolio Rp 13.0 Оp 39 1.75 х Y 12.0 34 1.30 7.2 24 0.85 Market 11.0 29 1.00 Risk-free 5.6 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset:...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP 15.5% 14.5 7.4 11.7 7.0 Op 36% 31 21 26 0 Bp 1.35 1.15 0.60 1.00 Market Risk-free 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your ratio...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP 15.5% 14.5 7.4 11.7 7.0 Op 36% 31 21 26 0 Bp 1.35 1.15 0.60 1.00 Market Risk-free 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your ratio...

13. An portfolio manager gathered the following information about a fund. Fund's rate of return 20%...

13. An portfolio manager gathered the following information about a fund. Fund's rate of return 20% Market rate of return 11% Risk-free rate 5% Beta of the fund 1.3 The Jensen's alpha for the fund is closest to:

13. An portfolio manager gathered the following information about a fund. Fund's rate of return 20% Market rate of return 11% Risk-free rate 5% Beta of the fund 1.3 The Jensen's alpha for the fund is closest to:

6. (Jensen's alpha) The risk- n's alpha) The risk-free rate is 2%. You observe two fund...

6. (Jensen's alpha) The risk- n's alpha) The risk-free rate is 2%. You observe two fund managers (A and B) and the market portfolio. Use в со JENSEN'S ALPHA 2 Risk-free return 2% 3 Mutual fund 4 Mean return 5 Standard deviation 6 Correlation coefficient with the market (Pim) 7 Beta 8 "Normative return" (based on the SML) 9 Jensen's alpha A 7% 25% 0.36 Market portfolio 10% 18% B 20% 72% 0.5 a. Calculate the beta of each stock...

6. (Jensen's alpha) The risk- n's alpha) The risk-free rate is 2%. You observe two fund managers (A and B) and the market portfolio. Use в со JENSEN'S ALPHA 2 Risk-free return 2% 3 Mutual fund 4 Mean return 5 Standard deviation 6 Correlation coefficient with the market (Pim) 7 Beta 8 "Normative return" (based on the SML) 9 Jensen's alpha A 7% 25% 0.36 Market portfolio 10% 18% B 20% 72% 0.5 a. Calculate the beta of each stock...

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Risk-Free Year 2011 2012 2013 2014 2015 Fund -17.68 25.1 13.4 6.6 -1.8 Market -34.5% 20.5 12.4 8 .4 -4.2 What are the Sharpe and Treynor ratios for the fund? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Sharpe ratio Treynor ratio

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Risk-Free Year 2011 2012 2013 2014 2015 Fund -17.68 25.1 13.4 6.6 -1.8 Market -34.5% 20.5 12.4 8 .4 -4.2 What are the Sharpe and Treynor ratios for the fund? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Sharpe ratio Treynor ratio

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97 Risk-F Year 2011 2012 2013 2014 Fund -16.4 25.1 13.2 Market -32.5 20.3 2015 -1.68 What are the Sharpe and Treynor ratios for the fund? (Do not round Intermediate calculations. Round your answers to 4 decimal places.) Sharpe ratio Treynor ratio

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97 Risk-F Year 2011 2012 2013 2014 Fund -16.4 25.1 13.2 Market -32.5 20.3 2015 -1.68 What are the Sharpe and Treynor ratios for the fund? (Do not round Intermediate calculations. Round your answers to 4 decimal places.) Sharpe ratio Treynor ratio

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Risk-Free Year 2011 2012 2013 2014 2015 Fund -14.92% 25.1 12.8 7.0 -1.44 Market -28.5% 19.9 10.6 7.6 -2.2 What are the Sharpe and Treynor ratios for the fund? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Answer is complete but not...

You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Risk-Free Year 2011 2012 2013 2014 2015 Fund -14.92% 25.1 12.8 7.0 -1.44 Market -28.5% 19.9 10.6 7.6 -2.2 What are the Sharpe and Treynor ratios for the fund? (Do not round intermediate calculations. Round your answers to 4 decimal places.) Answer is complete but not...

8. You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Risk-Free 2% Year 2011 2012 2013 2014 2015 Fund -15.13% 25.1 12.5 6.4 -1.26 Market -25.5% 19.6 9.7 7.6 -2.2 که ن What are the Sharpe and Treynor ratios for the fund? (Do not round intermediate calculations. Round your answers to 4 decimal places.)

8. You have been given the following return information for a mutual fund, the market index, and the risk-free rate. You also know that the return correlation between the fund and the market is 0.97. Risk-Free 2% Year 2011 2012 2013 2014 2015 Fund -15.13% 25.1 12.5 6.4 -1.26 Market -25.5% 19.6 9.7 7.6 -2.2 که ن What are the Sharpe and Treynor ratios for the fund? (Do not round intermediate calculations. Round your answers to 4 decimal places.)

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP 13.0% 12.0 7.0 10.1 5.0 op 30% 25 15 20 Bp 1.30 1.10 0.75 1.00 Market Risk-free 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your ratio answers...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP 13.0% 12.0 7.0 10.1 5.0 op 30% 25 15 20 Bp 1.30 1.10 0.75 1.00 Market Risk-free 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your ratio answers...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset ВР Portfolio Rp 13.0 Оp 39 1.75 х Y 12.0 34 1.30 7.2 24 0.85 Market 11.0 29 1.00 Risk-free 5.6 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset ВР Portfolio Rp 13.0 Оp 39 1.75 х Y 12.0 34 1.30 7.2 24 0.85 Market 11.0 29 1.00 Risk-free 5.6 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP 15.5% 14.5 7.4 11.7 7.0 Op 36% 31 21 26 0 Bp 1.35 1.15 0.60 1.00 Market Risk-free 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your ratio...

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio RP 15.5% 14.5 7.4 11.7 7.0 Op 36% 31 21 26 0 Bp 1.35 1.15 0.60 1.00 Market Risk-free 0 What are the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio? (A negative value should be indicated by a minus sign. Leave no cells blank - be certain to enter "O" wherever required. Do not round intermediate calculations. Round your ratio...

13. An portfolio manager gathered the following information about a fund. Fund's rate of return 20% Market rate of return 11% Risk-free rate 5% Beta of the fund 1.3 The Jensen's alpha for the fund is closest to:

13. An portfolio manager gathered the following information about a fund. Fund's rate of return 20% Market rate of return 11% Risk-free rate 5% Beta of the fund 1.3 The Jensen's alpha for the fund is closest to:

6. (Jensen's alpha) The risk- n's alpha) The risk-free rate is 2%. You observe two fund managers (A and B) and the market portfolio. Use в со JENSEN'S ALPHA 2 Risk-free return 2% 3 Mutual fund 4 Mean return 5 Standard deviation 6 Correlation coefficient with the market (Pim) 7 Beta 8 "Normative return" (based on the SML) 9 Jensen's alpha A 7% 25% 0.36 Market portfolio 10% 18% B 20% 72% 0.5 a. Calculate the beta of each stock...

6. (Jensen's alpha) The risk- n's alpha) The risk-free rate is 2%. You observe two fund managers (A and B) and the market portfolio. Use в со JENSEN'S ALPHA 2 Risk-free return 2% 3 Mutual fund 4 Mean return 5 Standard deviation 6 Correlation coefficient with the market (Pim) 7 Beta 8 "Normative return" (based on the SML) 9 Jensen's alpha A 7% 25% 0.36 Market portfolio 10% 18% B 20% 72% 0.5 a. Calculate the beta of each stock...

Most questions answered within 3 hours.

-

A (8.5) cm tall object is placed at a distance of (14.2) cm from

a convex...

asked 6 minutes ago -

(2) For the following questions, consider a data set that

exhibits a normal distribution. Report the...

asked 7 minutes ago -

What exactly is an information system? How does it work" What

are its people organization,

...

asked 8 minutes ago -

The Food Marketing Institute shows that 17% of households spend

more than $100 per week on...

asked 18 minutes ago -

Go to NCBI BLAST search web page

1st search: GEKDLRRAKDINQEVYNF

2nd search: PTSQRLQLLEPFDK

3rd search: GEKDLRRAKDINQEVYNF...

asked 21 minutes ago -

Explain how each of the following three conditions could be a

red flag for a register...

asked 26 minutes ago -

In a two-way factorial ANOVA, the final F-ratio for

factor AxB is determined by dividing _____...

asked 56 minutes ago -

Show your solutions for answer.

4. An aqueous solution contains 9.21 g of

K4Fe(CN)6 in a...

asked 26 minutes ago -

The random variable X has a uniform distribution with values

between 16 and 18. What is...

asked 36 minutes ago -

Evaluate each of the following transactions in terms of their

effect on assets, liabilities, and equity....

asked 35 minutes ago -

The amounts of nicotine in a certain brand of cigarette are

normally distributed with a mean...

asked 55 minutes ago -

The commercial lending department of First Bank made a

substantial loan to Alpha Company after obtaining...

asked 41 minutes ago