This morning you agreed to buy a one-year Treasury bond in six months. The bond has...

|

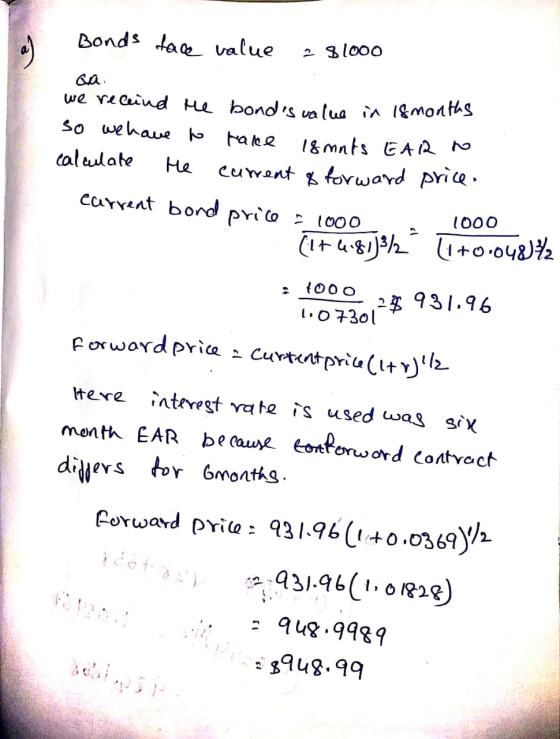

This morning you agreed to buy a one-year Treasury bond in six months. The bond has a face value of $1,000. Use the spot interest rates listed here to answer the following questions. |

| Time | EAR | ||

| 6 months | 3.69 | % | |

| 12 months | 4.13 | ||

| 18 months | 4.81 | ||

| 24 months | 5.53 | ||

| a. | What is the forward price of this contract? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) |

| b. | Suppose shortly after you purchased the forward contract all rates increased by 25 basis points. For example, the six-month rate increased from 3.69 percent to 3.94 percent. What is the price of a forward contract otherwise identical to yours given these changes? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) |

Homework Answers

Add Answer to:

This morning you agreed to buy a one-year Treasury bond in six

months. The bond has...

signment 0 Saved Help Save & This morning you agreed to buy a one-year Treasury bond...

signment 0 Saved Help Save & This morning you agreed to buy a one-year Treasury bond in six months. The bond has a face value of $1,000. Use the spot interest rates listed here to answer the following questions. Time 6 months 12 months 18 months 24 months EAR 3.80% 4.24 4.92 5.64 a. What is the forward price of this contract? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g.. 32.16.) b. Suppose shortly...

signment 0 Saved Help Save & This morning you agreed to buy a one-year Treasury bond in six months. The bond has a face value of $1,000. Use the spot interest rates listed here to answer the following questions. Time 6 months 12 months 18 months 24 months EAR 3.80% 4.24 4.92 5.64 a. What is the forward price of this contract? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g.. 32.16.) b. Suppose shortly...

Consider the following a. What is the duration of a two-year bond that pays an annual...

Consider the following a. What is the duration of a two-year bond that pays an annual coupon of 10 percent and whose current yield to maturity is 13 percent? Use $1,000 as the face value. (Do not round intermediate calculations. Round your answer to 3 decimal places. (e.g.. 32.161)) b. What is the expected change in the price of the bond if interest rates are expected to increase by 0.3 percent? (Negative amount should be indicated by a minus sign....

Consider the following a. What is the duration of a two-year bond that pays an annual coupon of 10 percent and whose current yield to maturity is 13 percent? Use $1,000 as the face value. (Do not round intermediate calculations. Round your answer to 3 decimal places. (e.g.. 32.161)) b. What is the expected change in the price of the bond if interest rates are expected to increase by 0.3 percent? (Negative amount should be indicated by a minus sign....

Consider an eight-year, 11.5 percent annual coupon bond with a face value of $1,000. The bond...

Consider an eight-year, 11.5 percent annual coupon bond with a face value of $1,000. The bond is trading at a rate of 8.5 percent. a. What is the price of the bond? (Do not round intermediate calculations. Round your answer to 2 decimal places. (e.g., 32.16)) Price of the bond $ b. If the rate of interest increases 1 percent, what will be the bond’s new price? (Do not round intermediate calculations. Round your answer to 2 decimal places. (e.g.,...

You bought a stock three months ago for $43.48 per share. The stock paid no dividends....

You bought a stock three months ago for $43.48 per share. The stock paid no dividends. The current share price is $47.09 What is the APR of your investment? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places (e.g., 32.16).) APR % What is the EAR of your investment? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places (e.g., 32.16).) EAR %

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of 9.4 percent, a YTM of 7.4 percent, and has 19 years to maturity. Bond Y is a discount bond making semiannual payments. This bond has a coupon rate of 7.4 percent, a YTM of 9.4 percent, and also has 19 years to maturity. Assume the interest rates remain unchanged and both bonds have a par value of $1,000. a. What are the prices of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of 9.4 percent, a YTM of 7.4 percent, and has 19 years to maturity. Bond Y is a discount bond making semiannual payments. This bond has a coupon rate of 7.4 percent, a YTM of 9.4 percent, and also has 19 years to maturity. Assume the interest rates remain unchanged and both bonds have a par value of $1,000. a. What are the prices of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of 8.2 percent, a YTM of 6.2 percent, and has 15 years to maturity. Bond Y is a discount bond making semiannual payments. This bond has a coupon rate of 6.2 percent, a YTM of 8.2 percent, and also has 15 years to maturity. Assume the interest rates remain unchanged and both bonds have a par value of $1,000. a. What are the prices of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of 8.2 percent, a YTM of 6.2 percent, and has 15 years to maturity. Bond Y is a discount bond making semiannual payments. This bond has a coupon rate of 6.2 percent, a YTM of 8.2 percent, and also has 15 years to maturity. Assume the interest rates remain unchanged and both bonds have a par value of $1,000. a. What are the prices of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of 9.2 percent, a YTM of 7.2 percent, and has 17 years to maturity. Bond Y is a discount bond making semiannual payments. This bond has a coupon rate of 7.2 percent, a YTM of 9.2 percent, and also has 17 years to maturity. Assume the interest rates remain unchanged and both bonds have a par value of $1,000. a. What are the prices of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of 9.2 percent, a YTM of 7.2 percent, and has 17 years to maturity. Bond Y is a discount bond making semiannual payments. This bond has a coupon rate of 7.2 percent, a YTM of 9.2 percent, and also has 17 years to maturity. Assume the interest rates remain unchanged and both bonds have a par value of $1,000. a. What are the prices of...

A put option that expires in six months with an exercise price of $45 sells for...

A put option that expires in six months with an exercise price of $45 sells for $2.34. The stock is currently priced at $48, and the risk-free rate is 3.5 percent per year, compounded continuously. What is the price of a call option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call priceſ A call option with an exercise price of $70 and four months to expiration has...

A put option that expires in six months with an exercise price of $45 sells for $2.34. The stock is currently priced at $48, and the risk-free rate is 3.5 percent per year, compounded continuously. What is the price of a call option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call priceſ A call option with an exercise price of $70 and four months to expiration has...

A call option has an exercise price of $70 and matures in six months. The current...

A call option has an exercise price of $70 and matures in six months. The current stock price is $73, and the risk-free rate is 5 percent per year, compounded continuously. What is the price of the call if the standard deviation of the stock is O percent per year? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call option price

A call option has an exercise price of $70 and matures in six months. The current stock price is $73, and the risk-free rate is 5 percent per year, compounded continuously. What is the price of the call if the standard deviation of the stock is O percent per year? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call option price

1. You buy a zero coupon bond at the beginning of the year that has a...

1. You buy a zero coupon bond at the beginning of the year that has a face value of $1,000, a YTM of 10 percent, and 22 years to maturity. You hold the bond for the entire year. Assume semiannual compounding. How much interest income will you have to declare on your tax return? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) what is the Interest income $ ? 2. Ayden, Inc., has...

signment 0 Saved Help Save & This morning you agreed to buy a one-year Treasury bond in six months. The bond has a face value of $1,000. Use the spot interest rates listed here to answer the following questions. Time 6 months 12 months 18 months 24 months EAR 3.80% 4.24 4.92 5.64 a. What is the forward price of this contract? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g.. 32.16.) b. Suppose shortly...

signment 0 Saved Help Save & This morning you agreed to buy a one-year Treasury bond in six months. The bond has a face value of $1,000. Use the spot interest rates listed here to answer the following questions. Time 6 months 12 months 18 months 24 months EAR 3.80% 4.24 4.92 5.64 a. What is the forward price of this contract? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g.. 32.16.) b. Suppose shortly...

Consider the following a. What is the duration of a two-year bond that pays an annual coupon of 10 percent and whose current yield to maturity is 13 percent? Use $1,000 as the face value. (Do not round intermediate calculations. Round your answer to 3 decimal places. (e.g.. 32.161)) b. What is the expected change in the price of the bond if interest rates are expected to increase by 0.3 percent? (Negative amount should be indicated by a minus sign....

Consider the following a. What is the duration of a two-year bond that pays an annual coupon of 10 percent and whose current yield to maturity is 13 percent? Use $1,000 as the face value. (Do not round intermediate calculations. Round your answer to 3 decimal places. (e.g.. 32.161)) b. What is the expected change in the price of the bond if interest rates are expected to increase by 0.3 percent? (Negative amount should be indicated by a minus sign....

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of 9.4 percent, a YTM of 7.4 percent, and has 19 years to maturity. Bond Y is a discount bond making semiannual payments. This bond has a coupon rate of 7.4 percent, a YTM of 9.4 percent, and also has 19 years to maturity. Assume the interest rates remain unchanged and both bonds have a par value of $1,000. a. What are the prices of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of 9.4 percent, a YTM of 7.4 percent, and has 19 years to maturity. Bond Y is a discount bond making semiannual payments. This bond has a coupon rate of 7.4 percent, a YTM of 9.4 percent, and also has 19 years to maturity. Assume the interest rates remain unchanged and both bonds have a par value of $1,000. a. What are the prices of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of 8.2 percent, a YTM of 6.2 percent, and has 15 years to maturity. Bond Y is a discount bond making semiannual payments. This bond has a coupon rate of 6.2 percent, a YTM of 8.2 percent, and also has 15 years to maturity. Assume the interest rates remain unchanged and both bonds have a par value of $1,000. a. What are the prices of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of 8.2 percent, a YTM of 6.2 percent, and has 15 years to maturity. Bond Y is a discount bond making semiannual payments. This bond has a coupon rate of 6.2 percent, a YTM of 8.2 percent, and also has 15 years to maturity. Assume the interest rates remain unchanged and both bonds have a par value of $1,000. a. What are the prices of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of 9.2 percent, a YTM of 7.2 percent, and has 17 years to maturity. Bond Y is a discount bond making semiannual payments. This bond has a coupon rate of 7.2 percent, a YTM of 9.2 percent, and also has 17 years to maturity. Assume the interest rates remain unchanged and both bonds have a par value of $1,000. a. What are the prices of...

Bond X is a premium bond making semiannual payments. The bond has a coupon rate of 9.2 percent, a YTM of 7.2 percent, and has 17 years to maturity. Bond Y is a discount bond making semiannual payments. This bond has a coupon rate of 7.2 percent, a YTM of 9.2 percent, and also has 17 years to maturity. Assume the interest rates remain unchanged and both bonds have a par value of $1,000. a. What are the prices of...

A put option that expires in six months with an exercise price of $45 sells for $2.34. The stock is currently priced at $48, and the risk-free rate is 3.5 percent per year, compounded continuously. What is the price of a call option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call priceſ A call option with an exercise price of $70 and four months to expiration has...

A put option that expires in six months with an exercise price of $45 sells for $2.34. The stock is currently priced at $48, and the risk-free rate is 3.5 percent per year, compounded continuously. What is the price of a call option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call priceſ A call option with an exercise price of $70 and four months to expiration has...

A call option has an exercise price of $70 and matures in six months. The current stock price is $73, and the risk-free rate is 5 percent per year, compounded continuously. What is the price of the call if the standard deviation of the stock is O percent per year? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call option price

A call option has an exercise price of $70 and matures in six months. The current stock price is $73, and the risk-free rate is 5 percent per year, compounded continuously. What is the price of the call if the standard deviation of the stock is O percent per year? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call option price

Most questions answered within 3 hours.

-

trust is best established through the combination of ------and

------- .

1. magnanimity and justice

2....

asked 24 seconds from now -

Suppose that the satellite around the earth has an orbit that is

24 KM larger in...

asked 1 minute ago -

A nozzle with a radius of 0.250 cm is attached to a garden hose

with a...

asked 11 minutes ago -

PLEASE do not use any loops for the program; only recursion is

allowed

4. Write a...

asked 19 minutes ago -

Please help me with me. I did the first part to write the operations but in...

asked 17 minutes ago -

Use Cryptool to find the Cryptographic SHA-1 hash value of the

string "abc". The calculator is...

asked 21 minutes ago -

You are attempting to calculate a firm’s free cash flow to

equity. You know the following...

asked 1 hour ago -

the following reaction occurs in a balloon containing

N2O2 gas

N2O4(g)=2NO2(g)

will the volume of the...

asked 1 hour ago -

answer the questions throughout this program

public class Day implements Comparable {

Private Boolean atWork;...

asked 1 hour ago -

This is C++ code for parking fee management program

#include <iostream>

#include <iomanip>

using namespace std;...

asked 2 hours ago -

The free energy change for the following reaction at 25 °C, when

[Sn2+] = 1.17 M...

asked 3 hours ago -

An MNE is this kind of industry when competition in one country

is essentially independent of...

asked 5 hours ago