Homework Answers

Add Answer to:

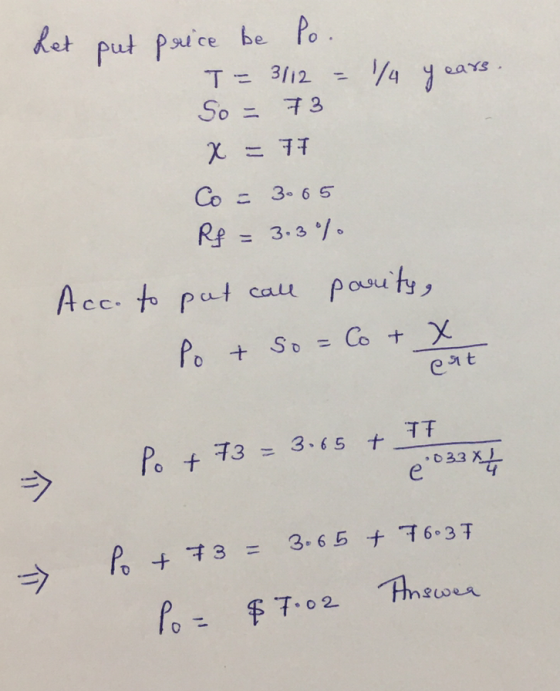

Problem 22-6 Put-Call Parity A stock is currently selling for $73 per share. A call option...

Question 12 2 pts A stock is currently selling for $41 per share. A call option...

Question 12 2 pts A stock is currently selling for $41 per share. A call option with an exercise price of $45 sells for $3.17 and expires in three months. If the risk-free rate of interest is 4.42 % per year, compounded continuously, what is the price of a put option with the same exercise price? (Round answer to 2 decimal places. Do not round intermediate calculations). Topic: Put-Call Parity

Question 12 2 pts A stock is currently selling for $41 per share. A call option with an exercise price of $45 sells for $3.17 and expires in three months. If the risk-free rate of interest is 4.42 % per year, compounded continuously, what is the price of a put option with the same exercise price? (Round answer to 2 decimal places. Do not round intermediate calculations). Topic: Put-Call Parity

Problem 22-8 Put-Call Parity A put option and a call option with an exercise price of...

Problem 22-8 Put-Call Parity A put option and a call option with an exercise price of $75 and three months to expiration sell for $1.35 and $5.70, respectively. If the risk-free rate is 4.4 percent per year, compounded continuously, what is the current stock price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Current stock price

Problem 22-8 Put-Call Parity A put option and a call option with an exercise price of $75 and three months to expiration sell for $1.35 and $5.70, respectively. If the risk-free rate is 4.4 percent per year, compounded continuously, what is the current stock price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Current stock price

A put option that expires in six months with an exercise price of $45 sells for...

A put option that expires in six months with an exercise price of $45 sells for $4.80. The stock is currently priced at $41, and the risk-free rate is 3.3 percent per year, compounded continuously. What is the price of a call option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.)

A put option that expires in six months with an exercise price of $45 sells for...

A put option that expires in six months with an exercise price of $45 sells for $2.34. The stock is currently priced at $48, and the risk-free rate is 3.5 percent per year, compounded continuously. What is the price of a call option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call priceſ A call option with an exercise price of $70 and four months to expiration has...

A put option that expires in six months with an exercise price of $45 sells for $2.34. The stock is currently priced at $48, and the risk-free rate is 3.5 percent per year, compounded continuously. What is the price of a call option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call priceſ A call option with an exercise price of $70 and four months to expiration has...

What are the prices of a call option and a put option with the following characteristics?...

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your final answers to 2 decimal places. (e.g., 32.16)) Stock price = $85 Exercise price = $80 Risk-free rate = 3.80% per year, compounded continuously Maturity = 5 months Standard deviation = 55% per year Call price $ Put price $

What are the prices of a call option and a put option with the following characteristics?...

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Stock price = $86 Exercise price = $85 Risk-free rate = 5.00% per year, compounded continuously Maturity = 4 months Standard deviation = 62% per year Call price $ Put price $

A call option with an exercise price of $70 and three months to expiration has a...

A call option with an exercise price of $70 and three months to expiration has a price of $4.10. The stock is currently priced at $69.80, and the risk-free rate is 5 percent per year, compounded continuously. What is the price of a put option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Put option price $

A call option with an exercise price of $25 and four months to expiration has a...

A call option with an exercise price of $25 and four months to expiration has a price of $2.75. The stock is currently priced at $23.80, and the risk-free rate is 2.5 percent per year, compounded continuously. What is the price of a put option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Put option price

A call option with an exercise price of $25 and four months to expiration has a price of $2.75. The stock is currently priced at $23.80, and the risk-free rate is 2.5 percent per year, compounded continuously. What is the price of a put option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Put option price

What are the prices of a call option and a put option with the following characteristics?...

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.9.,32.16.) Stock price $64 Exercise price $60 Risk-free rate continuously 2.7% per year, compounded Maturity4 months Standard-62% per year deviation Call price Put price

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.9.,32.16.) Stock price $64 Exercise price $60 Risk-free rate continuously 2.7% per year, compounded Maturity4 months Standard-62% per year deviation Call price Put price

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios...

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free...

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free...

Question 12 2 pts A stock is currently selling for $41 per share. A call option with an exercise price of $45 sells for $3.17 and expires in three months. If the risk-free rate of interest is 4.42 % per year, compounded continuously, what is the price of a put option with the same exercise price? (Round answer to 2 decimal places. Do not round intermediate calculations). Topic: Put-Call Parity

Question 12 2 pts A stock is currently selling for $41 per share. A call option with an exercise price of $45 sells for $3.17 and expires in three months. If the risk-free rate of interest is 4.42 % per year, compounded continuously, what is the price of a put option with the same exercise price? (Round answer to 2 decimal places. Do not round intermediate calculations). Topic: Put-Call Parity

Problem 22-8 Put-Call Parity A put option and a call option with an exercise price of $75 and three months to expiration sell for $1.35 and $5.70, respectively. If the risk-free rate is 4.4 percent per year, compounded continuously, what is the current stock price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Current stock price

Problem 22-8 Put-Call Parity A put option and a call option with an exercise price of $75 and three months to expiration sell for $1.35 and $5.70, respectively. If the risk-free rate is 4.4 percent per year, compounded continuously, what is the current stock price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Current stock price

A put option that expires in six months with an exercise price of $45 sells for $2.34. The stock is currently priced at $48, and the risk-free rate is 3.5 percent per year, compounded continuously. What is the price of a call option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call priceſ A call option with an exercise price of $70 and four months to expiration has...

A put option that expires in six months with an exercise price of $45 sells for $2.34. The stock is currently priced at $48, and the risk-free rate is 3.5 percent per year, compounded continuously. What is the price of a call option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Call priceſ A call option with an exercise price of $70 and four months to expiration has...

A call option with an exercise price of $25 and four months to expiration has a price of $2.75. The stock is currently priced at $23.80, and the risk-free rate is 2.5 percent per year, compounded continuously. What is the price of a put option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Put option price

A call option with an exercise price of $25 and four months to expiration has a price of $2.75. The stock is currently priced at $23.80, and the risk-free rate is 2.5 percent per year, compounded continuously. What is the price of a put option with the same exercise price? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) Put option price

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.9.,32.16.) Stock price $64 Exercise price $60 Risk-free rate continuously 2.7% per year, compounded Maturity4 months Standard-62% per year deviation Call price Put price

What are the prices of a call option and a put option with the following characteristics? (Do not round intermediate calculations and round your answers to 2 decimal places, e.9.,32.16.) Stock price $64 Exercise price $60 Risk-free rate continuously 2.7% per year, compounded Maturity4 months Standard-62% per year deviation Call price Put price

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free...

9. Put-call parity and the value of a put option Aa Aa E Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free...

Most questions answered within 3 hours.

-

T

F 53) Most differences

between human groups are the result of biology rather than

culture....

asked 3 seconds from now -

A 5.20 mW helium neon laser emits a visible laser beam with a

wavelength of 633...

asked 2 minutes ago -

Assignment:

Your

organization has made a strategic decision

to

outsourcework

currently performed in house. You have...

asked 1 minute ago -

A hospital performs 100 surgeries per week. The probability that

complications after surgery occur is 10%....

asked 2 minutes ago -

In preparing its cash flow statement for the year ended December

31, 2018, Green Co. gathered...

asked 4 minutes ago -

Donna is 18 years old and full time accounting student.She is

saving for an overseas holiday...

asked 4 minutes ago -

Service-oriented architectures (SOA) provide

object-oriented architectures for web platforms that represent a

collection of services. SOA...

asked 5 minutes ago -

Le Terroir Winery is considering an expansion project to produce

fine wines. The trial expansion will...

asked 14 minutes ago -

The Bahraini public budget experiences deficit in the last

seven years, what are procedures are taken...

asked 21 minutes ago -

You invested $30,000 in a mutual fund at the beginning of the

year when the NAV...

asked 24 minutes ago -

Would you expect the price elasticity of supply for guitars to

be more inelastic in the...

asked 26 minutes ago -

A snowmobile is originally at the point with position vector

30.1 m at 95.0° counterclockwise from...

asked 26 minutes ago