Homework Answers

Add Answer to:

Week 3 CH7 6 Saved Help Save & Exit 2 Check m Problem 7-8 25 points...

Week 3.CH7 6 Saved Help Save&Exit Check my Problem 7-7 25 points A pension fund manager...

Week 3.CH7 6 Saved Help Save&Exit Check my Problem 7-7 25 points A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 8% The probability distribution of the risky funds is as follows: Expected standard Deviation Return Stock fund (s Bond fund (8) 14 The correlation between the fund returns is...

Week 3.CH7 6 Saved Help Save&Exit Check my Problem 7-7 25 points A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 8% The probability distribution of the risky funds is as follows: Expected standard Deviation Return Stock fund (s Bond fund (8) 14 The correlation between the fund returns is...

24 Help Save& Exit Submit New Side You received no credit for this in the s...

24 Help Save& Exit Submit New Side You received no credit for this in the s a long-term government and corporate bond fund HW-2 and the third is a T-bill money market fund thot yields a rate of 4% The A pension fund manager is considering three mutual funds. The first is a stock fund, the band fund, and the third is a T-bill money market fund that yields a rate of 6%. The nt and corporate funds is 23...

24 Help Save& Exit Submit New Side You received no credit for this in the s a long-term government and corporate bond fund HW-2 and the third is a T-bill money market fund thot yields a rate of 4% The A pension fund manager is considering three mutual funds. The first is a stock fund, the band fund, and the third is a T-bill money market fund that yields a rate of 6%. The nt and corporate funds is 23...

Problem 7-8 A pension fund manager is considering three mutual funds. The first is a stock...

Problem 7-8 A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: Expected Return 24% 12 Standard Deviation 30% Stock fund (5) Bond fund (B) 19 The correlation between the fund returns is 0.13. What is the Sharpe ratio of...

Problem 7-8 A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: Expected Return 24% 12 Standard Deviation 30% Stock fund (5) Bond fund (B) 19 The correlation between the fund returns is 0.13. What is the Sharpe ratio of...

Help Save & Exit Submit Check my work A pension fund manager is considering three mutual...

Help Save & Exit Submit Check my work A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.3%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Stock fund (S) Expected Return 1 Standard Deviation 3 :48 The correlation between the fund returns is...

Help Save & Exit Submit Check my work A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.3%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Stock fund (S) Expected Return 1 Standard Deviation 3 :48 The correlation between the fund returns is...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term gove...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4% The probability distribution of the risky funds is as follows: Expected Return 23% Standard Deviation 29% Stock fund (S) Bond fund (8) 14 17 The correlation between the fund returns is 0.12 What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4% The probability distribution of the risky funds is as follows: Expected Return 23% Standard Deviation 29% Stock fund (S) Bond fund (8) 14 17 The correlation between the fund returns is 0.12 What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: 10 points Expected Return 24% 12 Standard Deviation 30% 19 Stock fund (S) Bond fund (B) eBook The correlation between the fund returns is 0.13. What is the Sharpe ratio...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: 10 points Expected Return 24% 12 Standard Deviation 30% 19 Stock fund (S) Bond fund (B) eBook The correlation between the fund returns is 0.13. What is the Sharpe ratio...

Need a help please. Thank you. A pension fund manager is considering three mutual funds. The first is a stock fun...

Need a help please. Thank you.

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.7%. The probability distributions of the risky funds are: Expected Return Stock fund (S) Bond fund (B) Standard Deviation 37% 31% 17% 8% The correlation between the fund returns is 0.1065. What is the...

Need a help please. Thank you.

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.7%. The probability distributions of the risky funds are: Expected Return Stock fund (S) Bond fund (B) Standard Deviation 37% 31% 17% 8% The correlation between the fund returns is 0.1065. What is the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

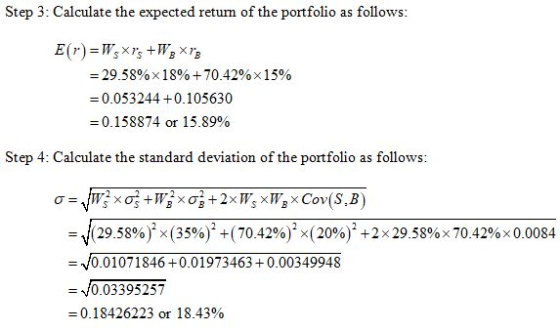

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 7%. The probability distribution of the risky funds is as follows: Expected Return Standard Deviation Stock fund (S) 18 % 35 % Bond fund (B) 15 20 The correlation between the fund returns is 0.12. What is the Sharpe ratio of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 6%. The probability distribution of the risky funds is as follows: Expected Return Standard Deviation Stock fund (S) 17 % 38 % Bond fund (B) 12 17 The correlation between the fund returns is 0.13. What is the Sharpe ratio of...

A pension fund manager is considering three mutual funds. The first is a stock fund, the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 5%. The probability distribution of the risky funds is as follows: Expected Return 19% 12 Standard Deviation 32% 15 Stock fund (5) Bond fund (B) The correlation between the fund returns is 0.11. What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 5%. The probability distribution of the risky funds is as follows: Expected Return 19% 12 Standard Deviation 32% 15 Stock fund (5) Bond fund (B) The correlation between the fund returns is 0.11. What is the Sharpe ratio of the best...

Week 3.CH7 6 Saved Help Save&Exit Check my Problem 7-7 25 points A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 8% The probability distribution of the risky funds is as follows: Expected standard Deviation Return Stock fund (s Bond fund (8) 14 The correlation between the fund returns is...

Week 3.CH7 6 Saved Help Save&Exit Check my Problem 7-7 25 points A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 8% The probability distribution of the risky funds is as follows: Expected standard Deviation Return Stock fund (s Bond fund (8) 14 The correlation between the fund returns is...

24 Help Save& Exit Submit New Side You received no credit for this in the s a long-term government and corporate bond fund HW-2 and the third is a T-bill money market fund thot yields a rate of 4% The A pension fund manager is considering three mutual funds. The first is a stock fund, the band fund, and the third is a T-bill money market fund that yields a rate of 6%. The nt and corporate funds is 23...

24 Help Save& Exit Submit New Side You received no credit for this in the s a long-term government and corporate bond fund HW-2 and the third is a T-bill money market fund thot yields a rate of 4% The A pension fund manager is considering three mutual funds. The first is a stock fund, the band fund, and the third is a T-bill money market fund that yields a rate of 6%. The nt and corporate funds is 23...

Problem 7-8 A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: Expected Return 24% 12 Standard Deviation 30% Stock fund (5) Bond fund (B) 19 The correlation between the fund returns is 0.13. What is the Sharpe ratio of...

Problem 7-8 A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: Expected Return 24% 12 Standard Deviation 30% Stock fund (5) Bond fund (B) 19 The correlation between the fund returns is 0.13. What is the Sharpe ratio of...

Help Save & Exit Submit Check my work A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.3%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Stock fund (S) Expected Return 1 Standard Deviation 3 :48 The correlation between the fund returns is...

Help Save & Exit Submit Check my work A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.3%. The probability distributions of the risky funds are: Stock fund (S) Bond fund (B) Stock fund (S) Expected Return 1 Standard Deviation 3 :48 The correlation between the fund returns is...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4% The probability distribution of the risky funds is as follows: Expected Return 23% Standard Deviation 29% Stock fund (S) Bond fund (8) 14 17 The correlation between the fund returns is 0.12 What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4% The probability distribution of the risky funds is as follows: Expected Return 23% Standard Deviation 29% Stock fund (S) Bond fund (8) 14 17 The correlation between the fund returns is 0.12 What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: 10 points Expected Return 24% 12 Standard Deviation 30% 19 Stock fund (S) Bond fund (B) eBook The correlation between the fund returns is 0.13. What is the Sharpe ratio...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 4%. The probability distribution of the risky funds is as follows: 10 points Expected Return 24% 12 Standard Deviation 30% 19 Stock fund (S) Bond fund (B) eBook The correlation between the fund returns is 0.13. What is the Sharpe ratio...

Need a help please. Thank you.

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.7%. The probability distributions of the risky funds are: Expected Return Stock fund (S) Bond fund (B) Standard Deviation 37% 31% 17% 8% The correlation between the fund returns is 0.1065. What is the...

Need a help please. Thank you.

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a sure rate of 4.7%. The probability distributions of the risky funds are: Expected Return Stock fund (S) Bond fund (B) Standard Deviation 37% 31% 17% 8% The correlation between the fund returns is 0.1065. What is the...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 5%. The probability distribution of the risky funds is as follows: Expected Return 19% 12 Standard Deviation 32% 15 Stock fund (5) Bond fund (B) The correlation between the fund returns is 0.11. What is the Sharpe ratio of the best...

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 5%. The probability distribution of the risky funds is as follows: Expected Return 19% 12 Standard Deviation 32% 15 Stock fund (5) Bond fund (B) The correlation between the fund returns is 0.11. What is the Sharpe ratio of the best...

Most questions answered within 3 hours.

-

The average length of time between arrivals at a turnpike

toll-booth is 26 seconds. What is...

asked 1 hour ago -

(a) A piston at 6.1 atm contains a gas that occupies a volume of

3.5 L....

asked 2 hours ago -

Please answer true or false. Words

cannot be changed or added in to make it true...

asked 2 hours ago -

An empty test tube weighs 15.923 grams. Then,

MgCl2•6H2O is added into the test tube. After...

asked 2 hours ago -

Assume memory access is 10 units of time and disk access is

10000 units of time....

asked 2 hours ago -

1. Are all good samples random?

2. Magazines often report surveys giving statistics such as “63%...

asked 3 hours ago -

Under all the various types of market structures, firms

must eventually earn some economic profits for...

asked 2 hours ago -

Consider the following fitness regime for a single locus trait

with two co-dominant alleles: w11 =...

asked 3 hours ago -

A large cable company reports the following.

80% of its customers subscribe to its cable TV...

asked 3 hours ago -

Please answer the question in brief.

Discuss the role of ERP in organizations. Are ERP tools...

asked 3 hours ago -

Discuss the pros and cons of collaborative software such

as SameTime. Does it increase productivity? What...

asked 3 hours ago -

Buying your in-laws a gift because it’s expected is

due to the ____________ motive of gift-giving....

asked 3 hours ago