Homework Answers

Add Answer to:

3) Assume you had two stocks, Stock A had an expected return of 20% and a...

Question 3 (total of 20 marks): An investor holds a portfolio comprising three assets (or stocks)...

Question 3 (total of 20 marks): An investor holds a portfolio comprising three assets (or stocks) A, B and C. Refer to the below tables to answer the questions that follow. Assume that returns are effective annual rates: Variables Stock A Stock B Stock C 33% 40% 25% Stock return standard deviation 0.25 $ 55,000.00 0.33 35,000.00 0.22 10,000.00 Investment $ $ Assume the following information holds: Correlation coefficient of the returns between A & B 0.10 Correlation coefficient of...

Question 3 (total of 20 marks): An investor holds a portfolio comprising three assets (or stocks) A, B and C. Refer to the below tables to answer the questions that follow. Assume that returns are effective annual rates: Variables Stock A Stock B Stock C 33% 40% 25% Stock return standard deviation 0.25 $ 55,000.00 0.33 35,000.00 0.22 10,000.00 Investment $ $ Assume the following information holds: Correlation coefficient of the returns between A & B 0.10 Correlation coefficient of...

s presented with the two following stocks 17. The investor Stock A Stock B Expected Return...

s presented with the two following stocks 17. The investor Stock A Stock B Expected Return Standard Deviation 30% 40% 60% 50% the portfolio that the expected return Assume that the correlation coefficient between the stocks is zero. What stock A invests 30% i A.20% B.37% 07a 18. The investor is presented with the two following stocks: Stock A Stock B Expected Return Standard Deviation 0% 40% 50% 60% Assume that the correlation coefficient between the stocks is zero. What...

s presented with the two following stocks 17. The investor Stock A Stock B Expected Return Standard Deviation 30% 40% 60% 50% the portfolio that the expected return Assume that the correlation coefficient between the stocks is zero. What stock A invests 30% i A.20% B.37% 07a 18. The investor is presented with the two following stocks: Stock A Stock B Expected Return Standard Deviation 0% 40% 50% 60% Assume that the correlation coefficient between the stocks is zero. What...

Considering the following information of three stocks Stock Expected rate of return Standard deviation ABC 13%...

Considering the following information of three stocks Stock Expected rate of return Standard deviation ABC 13% 20% XYZ 14% 20% MNO 15% 20% The correlation between ABC and XYZ is 0.36 The correlation between ABC and MNO is 0.52 The correlation between XYZ and MNO is 0.68 You decide to invest only in two stocks out of these three stocks. You want to choose a combination of two stocks that will create lower standard deviation. Half of your money will...

Considering the following information of three stocks Stock Expected rate of return Standard deviation ABC 13% 20% XYZ 14% 20% MNO 15% 20% The correlation between ABC and XYZ is 0.36 The correlation between ABC and MNO is 0.52 The correlation between XYZ and MNO is 0.68 You decide to invest only in two stocks out of these three stocks. You want to choose a combination of two stocks that will create lower standard deviation. Half of your money will...

Suppose the expected returns and standards deviations of two stocks were stock A: E (R) =9%,...

Suppose the expected returns and standards deviations of two stocks were stock A: E (R) =9%, STANDARD DEVIATION = 36% STOCK B: E (R) = 15%, STANDARD DEVIATION = 62% A. calculate the expected return of a portfolio that is composed of 35% of stock A and 65% of stock B. b. calculate the standard deviation of this portfolio when the correlation coefficient between the returns is 0.5 c. calculate the standard deviation of this portfolio (same weights in each...

Consider two stocks, Stock D, with an expected return of 20 percent and a standard deviation...

Consider two stocks, Stock D, with an expected return of 20 percent and a standard deviation of 36 percent, and Stock I, an international company, with an expected return of 6 percent and a standard deviation of 16 percent. The correlation between the two stocks is –0.01. What are the expected return and standard deviation of the minimum variance portfolio? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) Expected Return? Standard deviation?

6. Consider the following information for Stocks 1 and 2: Expected Standard Stock Return Deviation 1...

6. Consider the following information for Stocks 1 and 2: Expected Standard Stock Return Deviation 1 20% 40% 2 12% 20% NE a. The correlation between the returns of these two stocks is 0.3. How will you divide your money between Stocks 1 and 2 if your aim is to achieve a portfolio with an expected return of 18% p.a.? That is, what are the weights assigned to each stock? Also take note of the risk (i.e., standard deviation) of...

6. Consider the following information for Stocks 1 and 2: Expected Standard Stock Return Deviation 1 20% 40% 2 12% 20% NE a. The correlation between the returns of these two stocks is 0.3. How will you divide your money between Stocks 1 and 2 if your aim is to achieve a portfolio with an expected return of 18% p.a.? That is, what are the weights assigned to each stock? Also take note of the risk (i.e., standard deviation) of...

Consider a portfolio that contains two stocks. Stock "A" has an expected return of 10% and...

Consider a portfolio that contains two stocks. Stock "A" has an expected return of 10% and a standard deviation of 20%. Stock "B" has an expected return of -10% and a standard deviation of 25%. The proportion of your wealth invested in stock "A" is 60%. The correlation between the two stocks is 0. What is the expected return of the portfolio? Enter your answer as a percentage. Do not include the percentage sign in your answer. Enter your response...

8-3a Expected Portfolio Returns Calculate the expected return of the portfolio based on the following individual...

8-3a Expected Portfolio Returns Calculate the expected return of the portfolio based on the following individual investments and its percentage of the total portfolio. Expected Return Weight -5.4% 10% 3% 23% 3.9% 20% 10% 0% 50% 20% B. 8-3b Portfolio Risk Based on the expected portfolio retums below, te expected return for the portfolio is 5.8% (you can check this). Calculate the standard deviation of the following portfolio: Expected Return Probability 10% 1% 8-3e Beta-Part 1 Returns on technology stocks...

8-3a Expected Portfolio Returns Calculate the expected return of the portfolio based on the following individual investments and its percentage of the total portfolio. Expected Return Weight -5.4% 10% 3% 23% 3.9% 20% 10% 0% 50% 20% B. 8-3b Portfolio Risk Based on the expected portfolio retums below, te expected return for the portfolio is 5.8% (you can check this). Calculate the standard deviation of the following portfolio: Expected Return Probability 10% 1% 8-3e Beta-Part 1 Returns on technology stocks...

Question 3 (total of 20 marks): Refer to the below table to answer the questions that follow. Assume that returns are e...

Question 3 (total of 20 marks): Refer to the below table to answer the questions that follow. Assume that returns are effective annual rates Year Return on Stock A Return on Market 2007 35% 15% 2008 -35% -25% 2009 15% 40% Question 3a (1 marks): What is stock A's expected return? Question 3b (1 marks): What is the market's expected return? Question 3c (4 marks): What is the sample standard deviation of stock A's returns? buestion 3d (4 marks): What...

Question 3 (total of 20 marks): Refer to the below table to answer the questions that follow. Assume that returns are effective annual rates Year Return on Stock A Return on Market 2007 35% 15% 2008 -35% -25% 2009 15% 40% Question 3a (1 marks): What is stock A's expected return? Question 3b (1 marks): What is the market's expected return? Question 3c (4 marks): What is the sample standard deviation of stock A's returns? buestion 3d (4 marks): What...

You have a three-stock portfolio. Stock A has an expected return of 14 percent and a...

You have a three-stock portfolio. Stock A has an expected return of 14 percent and a standard deviation of 35 percent, Stock B has an expected return of 18 percent and a standard deviation of 53 percent, and Stock C has an expected return of 17 percent and a standard deviation of 35 percent. The correlation between Stocks A and B is .07. between Stocks A and C is 20, and between Stocks B and C is 19. Your portfolio...

You have a three-stock portfolio. Stock A has an expected return of 14 percent and a standard deviation of 35 percent, Stock B has an expected return of 18 percent and a standard deviation of 53 percent, and Stock C has an expected return of 17 percent and a standard deviation of 35 percent. The correlation between Stocks A and B is .07. between Stocks A and C is 20, and between Stocks B and C is 19. Your portfolio...

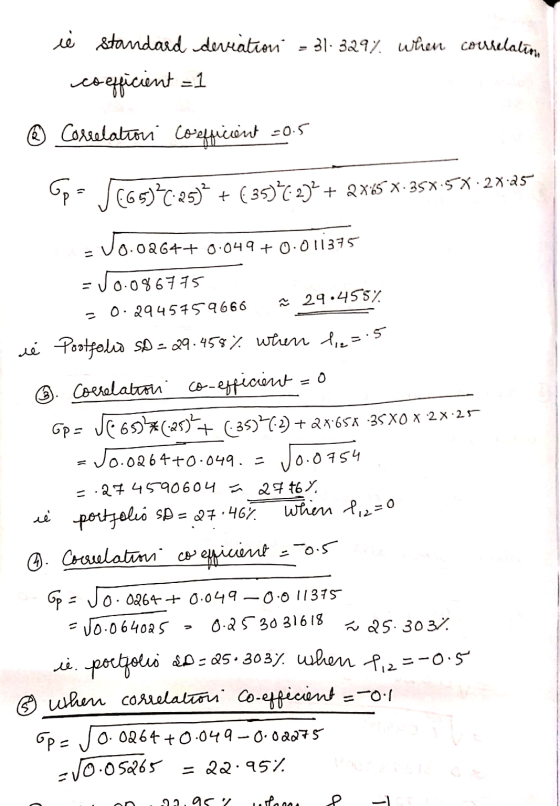

Question 3 (total of 20 marks): An investor holds a portfolio comprising three assets (or stocks) A, B and C. Refer to the below tables to answer the questions that follow. Assume that returns are effective annual rates: Variables Stock A Stock B Stock C 33% 40% 25% Stock return standard deviation 0.25 $ 55,000.00 0.33 35,000.00 0.22 10,000.00 Investment $ $ Assume the following information holds: Correlation coefficient of the returns between A & B 0.10 Correlation coefficient of...

Question 3 (total of 20 marks): An investor holds a portfolio comprising three assets (or stocks) A, B and C. Refer to the below tables to answer the questions that follow. Assume that returns are effective annual rates: Variables Stock A Stock B Stock C 33% 40% 25% Stock return standard deviation 0.25 $ 55,000.00 0.33 35,000.00 0.22 10,000.00 Investment $ $ Assume the following information holds: Correlation coefficient of the returns between A & B 0.10 Correlation coefficient of...

s presented with the two following stocks 17. The investor Stock A Stock B Expected Return Standard Deviation 30% 40% 60% 50% the portfolio that the expected return Assume that the correlation coefficient between the stocks is zero. What stock A invests 30% i A.20% B.37% 07a 18. The investor is presented with the two following stocks: Stock A Stock B Expected Return Standard Deviation 0% 40% 50% 60% Assume that the correlation coefficient between the stocks is zero. What...

s presented with the two following stocks 17. The investor Stock A Stock B Expected Return Standard Deviation 30% 40% 60% 50% the portfolio that the expected return Assume that the correlation coefficient between the stocks is zero. What stock A invests 30% i A.20% B.37% 07a 18. The investor is presented with the two following stocks: Stock A Stock B Expected Return Standard Deviation 0% 40% 50% 60% Assume that the correlation coefficient between the stocks is zero. What...

Considering the following information of three stocks Stock Expected rate of return Standard deviation ABC 13% 20% XYZ 14% 20% MNO 15% 20% The correlation between ABC and XYZ is 0.36 The correlation between ABC and MNO is 0.52 The correlation between XYZ and MNO is 0.68 You decide to invest only in two stocks out of these three stocks. You want to choose a combination of two stocks that will create lower standard deviation. Half of your money will...

Considering the following information of three stocks Stock Expected rate of return Standard deviation ABC 13% 20% XYZ 14% 20% MNO 15% 20% The correlation between ABC and XYZ is 0.36 The correlation between ABC and MNO is 0.52 The correlation between XYZ and MNO is 0.68 You decide to invest only in two stocks out of these three stocks. You want to choose a combination of two stocks that will create lower standard deviation. Half of your money will...

6. Consider the following information for Stocks 1 and 2: Expected Standard Stock Return Deviation 1 20% 40% 2 12% 20% NE a. The correlation between the returns of these two stocks is 0.3. How will you divide your money between Stocks 1 and 2 if your aim is to achieve a portfolio with an expected return of 18% p.a.? That is, what are the weights assigned to each stock? Also take note of the risk (i.e., standard deviation) of...

6. Consider the following information for Stocks 1 and 2: Expected Standard Stock Return Deviation 1 20% 40% 2 12% 20% NE a. The correlation between the returns of these two stocks is 0.3. How will you divide your money between Stocks 1 and 2 if your aim is to achieve a portfolio with an expected return of 18% p.a.? That is, what are the weights assigned to each stock? Also take note of the risk (i.e., standard deviation) of...

8-3a Expected Portfolio Returns Calculate the expected return of the portfolio based on the following individual investments and its percentage of the total portfolio. Expected Return Weight -5.4% 10% 3% 23% 3.9% 20% 10% 0% 50% 20% B. 8-3b Portfolio Risk Based on the expected portfolio retums below, te expected return for the portfolio is 5.8% (you can check this). Calculate the standard deviation of the following portfolio: Expected Return Probability 10% 1% 8-3e Beta-Part 1 Returns on technology stocks...

8-3a Expected Portfolio Returns Calculate the expected return of the portfolio based on the following individual investments and its percentage of the total portfolio. Expected Return Weight -5.4% 10% 3% 23% 3.9% 20% 10% 0% 50% 20% B. 8-3b Portfolio Risk Based on the expected portfolio retums below, te expected return for the portfolio is 5.8% (you can check this). Calculate the standard deviation of the following portfolio: Expected Return Probability 10% 1% 8-3e Beta-Part 1 Returns on technology stocks...

Question 3 (total of 20 marks): Refer to the below table to answer the questions that follow. Assume that returns are effective annual rates Year Return on Stock A Return on Market 2007 35% 15% 2008 -35% -25% 2009 15% 40% Question 3a (1 marks): What is stock A's expected return? Question 3b (1 marks): What is the market's expected return? Question 3c (4 marks): What is the sample standard deviation of stock A's returns? buestion 3d (4 marks): What...

Question 3 (total of 20 marks): Refer to the below table to answer the questions that follow. Assume that returns are effective annual rates Year Return on Stock A Return on Market 2007 35% 15% 2008 -35% -25% 2009 15% 40% Question 3a (1 marks): What is stock A's expected return? Question 3b (1 marks): What is the market's expected return? Question 3c (4 marks): What is the sample standard deviation of stock A's returns? buestion 3d (4 marks): What...

You have a three-stock portfolio. Stock A has an expected return of 14 percent and a standard deviation of 35 percent, Stock B has an expected return of 18 percent and a standard deviation of 53 percent, and Stock C has an expected return of 17 percent and a standard deviation of 35 percent. The correlation between Stocks A and B is .07. between Stocks A and C is 20, and between Stocks B and C is 19. Your portfolio...

You have a three-stock portfolio. Stock A has an expected return of 14 percent and a standard deviation of 35 percent, Stock B has an expected return of 18 percent and a standard deviation of 53 percent, and Stock C has an expected return of 17 percent and a standard deviation of 35 percent. The correlation between Stocks A and B is .07. between Stocks A and C is 20, and between Stocks B and C is 19. Your portfolio...

Most questions answered within 3 hours.

-

3. Gains from trade

Consider two neighbouring island countries called Euphoria and

Contente. They each have...

asked 55 minutes ago -

A business executive has the option to invest money in two

plans: Plan A guarantees that...

asked 3 hours ago -

Hello, can someone please help me answer this question?

How much heat is absorbed by a...

asked 3 hours ago -

. A marketing researcher conducted a survey of 25 shoppers

randomly selected at the local mall...

asked 3 hours ago -

Create an comprehensive response to the

following:

Antimicrobial agents work on a multitude of microbes (bacteria,...

asked 3 hours ago -

6.13 LAB: Step counter. Section 6.3.

A pedometer treats walking 2,000 steps as walking 1 mile....

asked 3 hours ago -

(14.2) A block of mass m = 10 kg riding on a frictionless

horizontal plane is...

asked 3 hours ago -

Use any search engine to search for articles about Starbucks

partnership with Tata Companies in India...

asked 3 hours ago -

Let’s say that for some reason Bank Excess Reserves suddenly

increase sharply. What effect would this...

asked 3 hours ago -

Given:

Curent Assets: $600,000

Total Assets: $2,600,000

Current Liabilities: $500,000

Total Liabilities: $1,700,000

What is the...

asked 3 hours ago -

1. What is a “Bankster”? What is insider trading? Why is it

illegal?

2. What is...

asked 3 hours ago -

A transverse wave on a cord is given by

D(x,t)=0.18sin(2.7x−61.0t), where Dand x are in m...

asked 3 hours ago