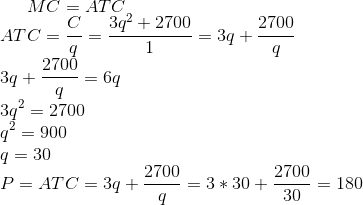

Suppose that every firm in an industry has identical cost curves given by C(q) = 3q2...

Suppose that every firm in an industry has identical cost curves given by

C(q) = 3q2 + 2700

MC(q) = 6q

What is the value of the efficient scale, qE ? Remember, the efficient scale occurs where MC(q) = ATC(q)

Homework Answers

Answer

qE=30 units and P=180

Add Answer to:

Suppose that every firm in an industry has identical cost curves

given by

C(q) = 3q2...

Suppose there is a perfectly competitive industry where all the firms are identical with identical cost...

Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm’s total cost is given by the equation TC = 100 + q2 + q where q is the quantity of output produced by the firm. You also know that the market demand for this product is given by the equation P = 900 - 2Q where Q is the market quantity. In addition, you are told that...

Firm B’s short-run cost function is: C = 12 - 2q + 3q2 + F Find...

Firm B’s short-run cost function is:

C = 12 - 2q + 3q2 + F Find the following: A. AFC B. AVC C. ATC D. MC E. At what output quantity is average total cost (ATC) minimized? Assume F = 63. F. At what output quantity does the MC curve cross the ATC and AVC curves? Assume F = 63 G. Graph the AFC, AVC, ATC and MC curves. Assume F = 63.

Firm B’s short-run cost function is:

C = 12 - 2q + 3q2 + F Find the following: A. AFC B. AVC C. ATC D. MC E. At what output quantity is average total cost (ATC) minimized? Assume F = 63. F. At what output quantity does the MC curve cross the ATC and AVC curves? Assume F = 63 G. Graph the AFC, AVC, ATC and MC curves. Assume F = 63.

Assume that all firms in this industry have identical cost curves, and that the market is...

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive. a) If the short-run supply curve is S1, what quantity does a firm produce? b) In the long-run, what quantity does a firm produce? Entire Market Representative Firm SU MC ATC RAVC Price ($/gallon) Price (s/gallon) W N N ослол оло LLL - - - - - TV - - - - - 0 2 4 6 8 10 12 0 1...

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive. a) If the short-run supply curve is S1, what quantity does a firm produce? b) In the long-run, what quantity does a firm produce? Entire Market Representative Firm SU MC ATC RAVC Price ($/gallon) Price (s/gallon) W N N ослол оло LLL - - - - - TV - - - - - 0 2 4 6 8 10 12 0 1...

Suppose that 3W is a representative firm operating in a perfectly competitive industry. 3W's total cost...

Suppose that 3W is a representative firm operating in a perfectly competitive industry. 3W's total cost of production is given by TC = 100+q+. a. If the output price is $400, what is 3W's short-run profit-maximizing level of output? b. What is 3W's profit at that price? Graph your results from a) and b). (Hint: your graph needs to include the MR, MC, and ATC curves.)

Suppose that 3W is a representative firm operating in a perfectly competitive industry. 3W's total cost of production is given by TC = 100+q+. a. If the output price is $400, what is 3W's short-run profit-maximizing level of output? b. What is 3W's profit at that price? Graph your results from a) and b). (Hint: your graph needs to include the MR, MC, and ATC curves.)

1) (Cost functions) a) Consider total cost function: C(q) = 48 + 3q2 + 2q, derive...

1) (Cost functions) a) Consider total cost function: C(q) = 48 + 3q2 + 2q, derive the average cost function, the marginal cost function, and the minimum efficient scale, and carefully graph the average cost and marginal cost curves. b) Consider total cost function: C(q) = 20 + 5q, derive the average cost function, the marginal cost function. How does the marginal cost compare to the average cost? Graph these two functions. Does the average cost obtain a minimum at...

4. Consider two firms with identical fixed costs, but different variable costs (for example, one firm...

4. Consider two firms with identical fixed costs, but different variable costs (for example, one firm has access to cheaper inputs or is located closer to the point of sale than the other): c. (g) = 625+q and MC,-1 and G (9)-625 + 492 and MC,-89 Find average total, average fixed and average variable cost functions for the two firms a) b) Find the minimum efficient scale of each firm average cost at MES (Hint: Use MC ATC rule). Which...

4. Consider two firms with identical fixed costs, but different variable costs (for example, one firm has access to cheaper inputs or is located closer to the point of sale than the other): c. (g) = 625+q and MC,-1 and G (9)-625 + 492 and MC,-89 Find average total, average fixed and average variable cost functions for the two firms a) b) Find the minimum efficient scale of each firm average cost at MES (Hint: Use MC ATC rule). Which...

4) Suppose each firm's long run average cost curve, for positive levels of output, is given by AC 0.10.05Q+5/Q. The...

4) Suppose each firm's long run average cost curve, for positive levels of output, is given by AC 0.10.05Q+5/Q. The marginal cost curve is given by MC 0.+0.1Q. (a) Find the minimum efficient scale for the above cost function (b) What is the firm's minimum average cost? (c) Suppose you have many identical firms in a long run competitive equilibrium. Demand is P 13.1-0.040. What is the market quantity? How many firms are there? (d) Suppose demand increases to P...

4) Suppose each firm's long run average cost curve, for positive levels of output, is given by AC 0.10.05Q+5/Q. The marginal cost curve is given by MC 0.+0.1Q. (a) Find the minimum efficient scale for the above cost function (b) What is the firm's minimum average cost? (c) Suppose you have many identical firms in a long run competitive equilibrium. Demand is P 13.1-0.040. What is the market quantity? How many firms are there? (d) Suppose demand increases to P...

5. In a competitive industry, all companies have identical long-run total cost curves given by LTC(q)...

5. In a competitive industry, all companies have identical long-run total cost curves given by LTC(q) = q + 36. The demand in this industry is described by D(p) = 2004 - 2p. a. What is the long-run supply function of an individual company in this industry? b. How many companies will operate in this industry in the long-run equilibrium?

5. In a competitive industry, all companies have identical long-run total cost curves given by LTC(q) = q + 36. The demand in this industry is described by D(p) = 2004 - 2p. a. What is the long-run supply function of an individual company in this industry? b. How many companies will operate in this industry in the long-run equilibrium?

Consider the competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the Industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on

6. Short-run supply and long-run equilibrium Consider the competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the Industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. The following diagram shows the market demand for copper. Use the orange points (square symbol) to plot the initial short-run industry supply curve when there are 20 firms in the market. (Hint:...

6. Short-run supply and long-run equilibrium Consider the competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the Industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. The following diagram shows the market demand for copper. Use the orange points (square symbol) to plot the initial short-run industry supply curve when there are 20 firms in the market. (Hint:...

2. Suppose the firm has the one variable production function Q=L?. Assume that the wage rate...

2. Suppose the firm has the one variable production function Q=L?. Assume that the wage rate is w= 20 and that the firm has fixed costs of 10. Finally, assume that the firm is a price taker and the market price is 2. a) Show that this production function exhibits increasing returns to scale. Show that the marginal product of labor is increasing. Illustrate the production function. Is it convex, concave or neither? b) Find the variable and total cost...

2. Suppose the firm has the one variable production function Q=L?. Assume that the wage rate is w= 20 and that the firm has fixed costs of 10. Finally, assume that the firm is a price taker and the market price is 2. a) Show that this production function exhibits increasing returns to scale. Show that the marginal product of labor is increasing. Illustrate the production function. Is it convex, concave or neither? b) Find the variable and total cost...

Firm B’s short-run cost function is:

C = 12 - 2q + 3q2 + F Find the following: A. AFC B. AVC C. ATC D. MC E. At what output quantity is average total cost (ATC) minimized? Assume F = 63. F. At what output quantity does the MC curve cross the ATC and AVC curves? Assume F = 63 G. Graph the AFC, AVC, ATC and MC curves. Assume F = 63.

Firm B’s short-run cost function is:

C = 12 - 2q + 3q2 + F Find the following: A. AFC B. AVC C. ATC D. MC E. At what output quantity is average total cost (ATC) minimized? Assume F = 63. F. At what output quantity does the MC curve cross the ATC and AVC curves? Assume F = 63 G. Graph the AFC, AVC, ATC and MC curves. Assume F = 63.

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive. a) If the short-run supply curve is S1, what quantity does a firm produce? b) In the long-run, what quantity does a firm produce? Entire Market Representative Firm SU MC ATC RAVC Price ($/gallon) Price (s/gallon) W N N ослол оло LLL - - - - - TV - - - - - 0 2 4 6 8 10 12 0 1...

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive. a) If the short-run supply curve is S1, what quantity does a firm produce? b) In the long-run, what quantity does a firm produce? Entire Market Representative Firm SU MC ATC RAVC Price ($/gallon) Price (s/gallon) W N N ослол оло LLL - - - - - TV - - - - - 0 2 4 6 8 10 12 0 1...

Suppose that 3W is a representative firm operating in a perfectly competitive industry. 3W's total cost of production is given by TC = 100+q+. a. If the output price is $400, what is 3W's short-run profit-maximizing level of output? b. What is 3W's profit at that price? Graph your results from a) and b). (Hint: your graph needs to include the MR, MC, and ATC curves.)

Suppose that 3W is a representative firm operating in a perfectly competitive industry. 3W's total cost of production is given by TC = 100+q+. a. If the output price is $400, what is 3W's short-run profit-maximizing level of output? b. What is 3W's profit at that price? Graph your results from a) and b). (Hint: your graph needs to include the MR, MC, and ATC curves.)

4. Consider two firms with identical fixed costs, but different variable costs (for example, one firm has access to cheaper inputs or is located closer to the point of sale than the other): c. (g) = 625+q and MC,-1 and G (9)-625 + 492 and MC,-89 Find average total, average fixed and average variable cost functions for the two firms a) b) Find the minimum efficient scale of each firm average cost at MES (Hint: Use MC ATC rule). Which...

4. Consider two firms with identical fixed costs, but different variable costs (for example, one firm has access to cheaper inputs or is located closer to the point of sale than the other): c. (g) = 625+q and MC,-1 and G (9)-625 + 492 and MC,-89 Find average total, average fixed and average variable cost functions for the two firms a) b) Find the minimum efficient scale of each firm average cost at MES (Hint: Use MC ATC rule). Which...

4) Suppose each firm's long run average cost curve, for positive levels of output, is given by AC 0.10.05Q+5/Q. The marginal cost curve is given by MC 0.+0.1Q. (a) Find the minimum efficient scale for the above cost function (b) What is the firm's minimum average cost? (c) Suppose you have many identical firms in a long run competitive equilibrium. Demand is P 13.1-0.040. What is the market quantity? How many firms are there? (d) Suppose demand increases to P...

4) Suppose each firm's long run average cost curve, for positive levels of output, is given by AC 0.10.05Q+5/Q. The marginal cost curve is given by MC 0.+0.1Q. (a) Find the minimum efficient scale for the above cost function (b) What is the firm's minimum average cost? (c) Suppose you have many identical firms in a long run competitive equilibrium. Demand is P 13.1-0.040. What is the market quantity? How many firms are there? (d) Suppose demand increases to P...

5. In a competitive industry, all companies have identical long-run total cost curves given by LTC(q) = q + 36. The demand in this industry is described by D(p) = 2004 - 2p. a. What is the long-run supply function of an individual company in this industry? b. How many companies will operate in this industry in the long-run equilibrium?

5. In a competitive industry, all companies have identical long-run total cost curves given by LTC(q) = q + 36. The demand in this industry is described by D(p) = 2004 - 2p. a. What is the long-run supply function of an individual company in this industry? b. How many companies will operate in this industry in the long-run equilibrium?

6. Short-run supply and long-run equilibrium Consider the competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the Industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. The following diagram shows the market demand for copper. Use the orange points (square symbol) to plot the initial short-run industry supply curve when there are 20 firms in the market. (Hint:...

6. Short-run supply and long-run equilibrium Consider the competitive market for copper. Assume that, regardless of how many firms are in the industry, every firm in the Industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. The following diagram shows the market demand for copper. Use the orange points (square symbol) to plot the initial short-run industry supply curve when there are 20 firms in the market. (Hint:...

2. Suppose the firm has the one variable production function Q=L?. Assume that the wage rate is w= 20 and that the firm has fixed costs of 10. Finally, assume that the firm is a price taker and the market price is 2. a) Show that this production function exhibits increasing returns to scale. Show that the marginal product of labor is increasing. Illustrate the production function. Is it convex, concave or neither? b) Find the variable and total cost...

2. Suppose the firm has the one variable production function Q=L?. Assume that the wage rate is w= 20 and that the firm has fixed costs of 10. Finally, assume that the firm is a price taker and the market price is 2. a) Show that this production function exhibits increasing returns to scale. Show that the marginal product of labor is increasing. Illustrate the production function. Is it convex, concave or neither? b) Find the variable and total cost...

Most questions answered within 3 hours.

-

Phosphorous + bromine = phosphorous tribromide. If 35.0 g of

bromine are reacted and 27.9 grams...

asked 1 hour ago -

Derive the long wavelength limit of the Planck energy density

distribution

asked 1 hour ago -

Calculate the pH of each of the following solutions.

0.50 M HBr

3.1×10−4 M KOH

4.2×10−5...

asked 4 hours ago -

For the year ended December 31, Depot Max’s cost of merchandise

sold was $85,600. Inventory at the...

asked 4 hours ago -

Week 10 - Professional Memo Assignment

Professional Memo Assignment

Your mission for this week, should you...

asked 4 hours ago -

Write a Python program that stores the data for each

player on the team, and it...

asked 5 hours ago -

In

the last 3 months, mike never knows when he is going to get his

allowance...

asked 5 hours ago -

Is Ca(OH)2 a Bronsted base, Lewis base, or both? Why?

asked 5 hours ago -

1A- Why don’t voters complain about U.S. tariffs on imported

sugar?

Because sugar is only a...

asked 5 hours ago -

Cash Payback Period

Primera Banco is evaluating two capital investment proposals for

a drive-up ATM kiosk,...

asked 5 hours ago -

Create a button in Swift (Xcode) that will create a charge,

create a charge using Stripe's...

asked 5 hours ago -

The reaction rate of CO and NO2 in the reaction

CO(g) + NO2(g) → CO2(g) +...

asked 5 hours ago