Homework Answers

Add Answer to:

4) Suppose each firm's long run average cost curve, for positive levels of output, is given by AC 0.10.05Q+5/Q. The...

Suppose each firm's long run average cost curve, for positive levels of output, is given by AC = 0.1 + 0.05Q + 5/Q....

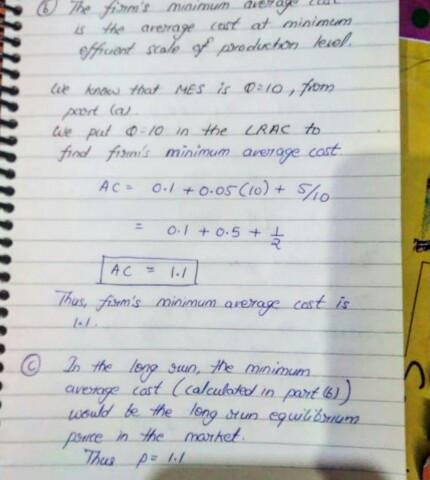

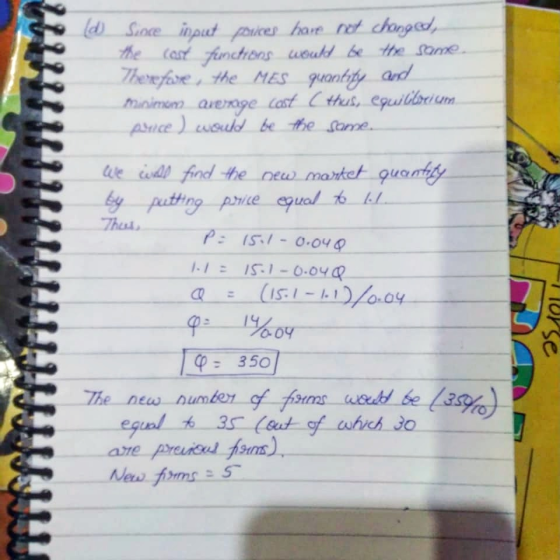

Suppose each firm's long run average cost curve, for positive levels of output, is given by AC = 0.1 + 0.05Q + 5/Q. The marginal cost curve is given by MC = 0.1 + 0.1Q. (a) Find the minimum efficient scale for the above cost function. (b) What is the firm's minimum average cost? (c) Suppose you have many identical firms in a long run competitive equilibrium. Demand is P = 13.1-0.04Q. What is the market quantity? How many firms...

(a) All firms in a perfectly competitive industry face the same long-run average cost curve, AC...

(a) All firms in a perfectly competitive industry face the same long-run average cost curve, AC = 0.05q – 5 + 500/q, and the same long-run marginal cost curve given by MC = 0.1q – 5. The market demand for the product of these firms is QD = 100,000 – 10,000P. i.Calculate the equilibrium price and quantity. ii.Assuming the market is in long-run equilibrium, how many firms will be on the market? (b) Suppose the demand for cotton T-shirts is...

need help with 5 and 6 Suppose a perfectly competitive firm's cost function is C(q)-4q*+16. Marginal cost for the firm...

need help with 5 and 6

Suppose a perfectly competitive firm's cost function is C(q)-4q*+16. Marginal cost for the firm is given by MC=8q. 1) Find equations for variable cost, fixed cost, average total cost, average variable cost and average fixed cost for this firm. Illustrate on a graph the firm's average variable cost curve, average total cost curve, and marginal cost curve. 2) Find the outputs that minimize average total cost, average variable cost and average fixed cost. 3)...

need help with 5 and 6

Suppose a perfectly competitive firm's cost function is C(q)-4q*+16. Marginal cost for the firm is given by MC=8q. 1) Find equations for variable cost, fixed cost, average total cost, average variable cost and average fixed cost for this firm. Illustrate on a graph the firm's average variable cost curve, average total cost curve, and marginal cost curve. 2) Find the outputs that minimize average total cost, average variable cost and average fixed cost. 3)...

Each firm in a perfectly competitive market has long run average cost represented as AC(q) =...

Each firm in a perfectly competitive market has long run average cost represented as AC(q) = 100q- 10+100/q. Long run marginal cost is MC=200q-10. The market demand is Qd = 2150-5P. Find the long run equilibrium output per firm, q*, the long run equilibrium price, P*, and the number of firms in the industry, n*. P = 190; Q = 1200; q =1 , n = 1200

Answer just part b ) All firms in a perfectly competitive industry face the same long-run...

Answer just part b ) All firms in a perfectly competitive industry face the same long-run average cost curve, AC = 0.05q – 5 + 500/q, and the same long-run marginal cost curve given by MC = 0.1q – 5. The market demand for the product of these firms is QD = 100,000 – 10,000P. i. Calculate the equilibrium price and quantity. ii. Assuming the market is in long-run equilibrium, how many firms will be on the market? (b) Suppose...

Suppose in a competitive market, the long-run cost function of a firm is ?(?) = 0.66874?5⁄4...

Suppose in a competitive market, the long-run cost function of a firm is ?(?) = 0.66874?5⁄4 + 1,280 where x is the output. (a) What is the minimum long-run average cost? At what output level is this attained? (b) Suppose all firms are identical, what is the long-run profit of each firm in the competitive market? What is the long-run equilibrium price? (c) Suppose there are 64,000 consumers each with demand function xd(p) = 625/p2 How many firms exist in...

3) Corn is produced under perfectly competitive conditions. Corn farmers have U-shaped, long-run average cost curves...

3) Corn is produced under perfectly competitive conditions. Corn

farmers have U-shaped, long-run average cost curves that reach a

minimum average cost of $3 per bushel when 1000 bushels are

produced. a.(10) If the market demand curve for corn is given

byLaTeX: Q_D=2,600,000-200,000PQ D = 2 , 600 , 000 − 200 , 000 P,

in the long-run equilibrium what will be the price of corn, how

much total corn will be demanded, and how many corn farms will

there...

3) Corn is produced under perfectly competitive conditions. Corn

farmers have U-shaped, long-run average cost curves that reach a

minimum average cost of $3 per bushel when 1000 bushels are

produced. a.(10) If the market demand curve for corn is given

byLaTeX: Q_D=2,600,000-200,000PQ D = 2 , 600 , 000 − 200 , 000 P,

in the long-run equilibrium what will be the price of corn, how

much total corn will be demanded, and how many corn farms will

there...

Assume each firms long-run average cost are given by AC=10+0.002Q where Q is market output, so long-run costs are incre...

Assume each firms long-run average cost are given by AC=10+0.002Q where Q is market output, so long-run costs are increasing in market output. Market demand is given by QD=DP=1,050-50P What is the long-run equilibrium price and market quantity? If market demand increases to QD=DP=1,600-50P find the new long-run equilibrium price and market quantity. Graph these equilibrium outcomes and calculate the change in producer surplus between (a) and (b) If a tax of $5.50 per unit output is introduced find the...

Corn is produced under perfectly competitive conditions. Corn farmers have U-shaped, long-run average cost curves that...

Corn is produced under perfectly competitive conditions. Corn farmers have U-shaped, long-run average cost curves that reach a minimum average cost of $3 per bushel when 1000 bushels are produced. a.(10) If the market demand curve for corn is given byQ D = 2,600,000 − 200,000 P, in the long-run equilibrium what will be the price of corn, how much total corn will be demanded, and how many corn farms will there be? b.(10) Suppose demand increases to Q D =...

Corn is produced under perfectly competitive conditions. Corn farmers have U-shaped, long-run average cost curves that...

Corn is produced under perfectly competitive conditions. Corn farmers have U-shaped, long-run average cost curves that reach a minimum average cost of $3 per bushel when 1000 bushels are produced. a.(10) If the market demand curve for corn is given byQ D = 2 , 600 , 000 − 200 , 000 P, in the long-run equilibrium what will be the price of corn, how much total corn will be demanded, and how many corn farms will there be? b.(10)...

need help with 5 and 6

Suppose a perfectly competitive firm's cost function is C(q)-4q*+16. Marginal cost for the firm is given by MC=8q. 1) Find equations for variable cost, fixed cost, average total cost, average variable cost and average fixed cost for this firm. Illustrate on a graph the firm's average variable cost curve, average total cost curve, and marginal cost curve. 2) Find the outputs that minimize average total cost, average variable cost and average fixed cost. 3)...

need help with 5 and 6

Suppose a perfectly competitive firm's cost function is C(q)-4q*+16. Marginal cost for the firm is given by MC=8q. 1) Find equations for variable cost, fixed cost, average total cost, average variable cost and average fixed cost for this firm. Illustrate on a graph the firm's average variable cost curve, average total cost curve, and marginal cost curve. 2) Find the outputs that minimize average total cost, average variable cost and average fixed cost. 3)...

3) Corn is produced under perfectly competitive conditions. Corn

farmers have U-shaped, long-run average cost curves that reach a

minimum average cost of $3 per bushel when 1000 bushels are

produced. a.(10) If the market demand curve for corn is given

byLaTeX: Q_D=2,600,000-200,000PQ D = 2 , 600 , 000 − 200 , 000 P,

in the long-run equilibrium what will be the price of corn, how

much total corn will be demanded, and how many corn farms will

there...

3) Corn is produced under perfectly competitive conditions. Corn

farmers have U-shaped, long-run average cost curves that reach a

minimum average cost of $3 per bushel when 1000 bushels are

produced. a.(10) If the market demand curve for corn is given

byLaTeX: Q_D=2,600,000-200,000PQ D = 2 , 600 , 000 − 200 , 000 P,

in the long-run equilibrium what will be the price of corn, how

much total corn will be demanded, and how many corn farms will

there...

Most questions answered within 3 hours.

-

You want to accumulate $28,000 in 10 years using annual

payments, the first one in a...

asked 2 minutes ago -

1. Name the 4 products obtained from the reactions of the light phase of photosynthesis.

2....

asked 3 minutes ago -

An electron in an excited hydrogen atom makes two transitions.

First the electron drops from the...

asked 13 minutes ago -

1) I have 50.0 g of ethanol (C2H5OH) at 100 K. I want

gaseous ethanol at 373...

asked 19 minutes ago -

Under which Article of the United States Constitution

can a federal court order a State employee...

asked 19 minutes ago -

You mix 5 moles of H2 at 300 K with 5 moles of He at 360...

asked 24 minutes ago -

In Python,

Write a complete program to input up to a maximum of 25

characters into...

asked 29 minutes ago -

A ship sailing in the sea enters a wide and deep

River. The density of seawater...

asked 32 minutes ago -

Solve it in Python

4. An alternade is a word in which its letters, taken

alternatively...

asked 51 minutes ago -

Assume that the company sells two products, X and Y, with

contribution margins per unit of...

asked 50 minutes ago -

The International Nanny Association (INA) reports that in a

sample of 928 in- home child care...

asked 1 hour ago -

Consider the following data:

x

−6−6

−5−5

−4−4

−3−3

−2−2

P(X=x)P(X=x)

0.20.2

0.20.2

0.20.2

0.20.2

0.20.2...

asked 1 hour ago