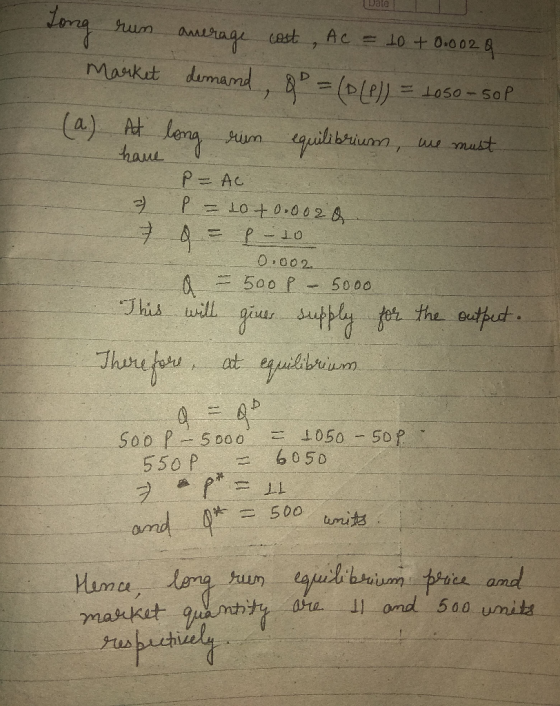

Assume each firms long-run average cost are given by AC=10+0.002Q where Q is market output, so long-run costs are incre...

- Assume each firms long-run average cost are given by

AC=10+0.002Q

where Q is market

output, so long-run costs are increasing in market output. Market

demand is given by

QD=DP=1,050-50P

where Q is market

output, so long-run costs are increasing in market output. Market

demand is given by

QD=DP=1,050-50P

- What is the long-run equilibrium price and market quantity?

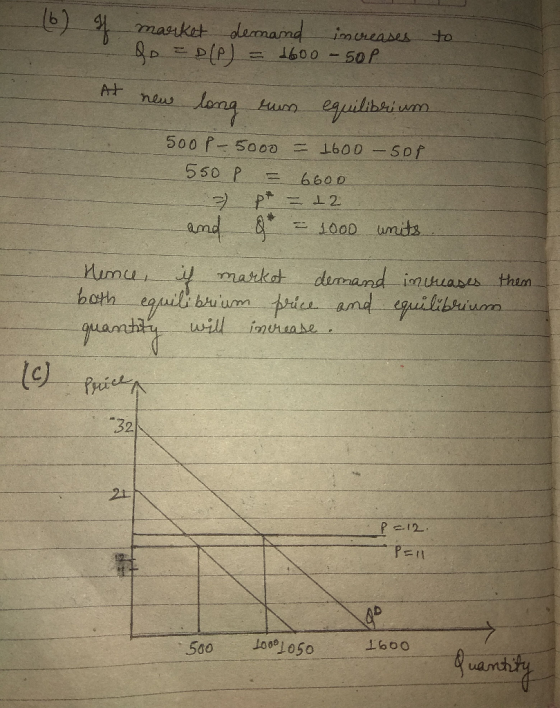

- If market demand increases to

QD=DP=1,600-50P

find the new long-run

equilibrium price and market quantity.

find the new long-run

equilibrium price and market quantity. - Graph these equilibrium outcomes and calculate the change in producer surplus between (a) and (b)

- If a tax of $5.50 per unit output is introduced find the price producers pay, price consumers pay and the new level of market output.

- What is the total tax revenue from the new tax? Assuming the market was in the equilibrium found in part (a) before the tax was introduced, what is the consumer and producers tax burden? What does the relative size of the producer’s and consumer’s tax burden tell you about the relative size of the elasticity of supply and elasticity of demand?

- Calculate the dead weight loss associated with the new tax.

Homework Answers

Add Answer to:

Assume each firms long-run average cost are given by AC=10+0.002Q where Q is market output, so long-run costs are incre...

For a constant cost industry in which all firms the same cost functions, their long-run average...

For a constant cost industry in which all firms the same cost functions, their long-run average cost is minimized at $10 per unit output and 20 units (i.e. q = 20). Market demand is given by QD=DP=1,500-50P. Find the long-run market supply function Find the long-run equilibrium price (P*), market quantity (Q*), firm output (q*), number of firms (n), and each firm’s profit. The short-run total cost function associated with each firm’s long-run costs is SCq=0.5q2-10q+200. Calculate the short-run average...

(a) All firms in a perfectly competitive industry face the same long-run average cost curve, AC...

(a) All firms in a perfectly competitive industry face the same long-run average cost curve, AC = 0.05q – 5 + 500/q, and the same long-run marginal cost curve given by MC = 0.1q – 5. The market demand for the product of these firms is QD = 100,000 – 10,000P. i.Calculate the equilibrium price and quantity. ii.Assuming the market is in long-run equilibrium, how many firms will be on the market? (b) Suppose the demand for cotton T-shirts is...

Each firm in a perfectly competitive market has long run average cost represented as AC(q) =...

Each firm in a perfectly competitive market has long run average cost represented as AC(q) = 100q- 10+100/q. Long run marginal cost is MC=200q-10. The market demand is Qd = 2150-5P. Find the long run equilibrium output per firm, q*, the long run equilibrium price, P*, and the number of firms in the industry, n*. P = 190; Q = 1200; q =1 , n = 1200

Answer just part b ) All firms in a perfectly competitive industry face the same long-run...

Answer just part b ) All firms in a perfectly competitive industry face the same long-run average cost curve, AC = 0.05q – 5 + 500/q, and the same long-run marginal cost curve given by MC = 0.1q – 5. The market demand for the product of these firms is QD = 100,000 – 10,000P. i. Calculate the equilibrium price and quantity. ii. Assuming the market is in long-run equilibrium, how many firms will be on the market? (b) Suppose...

4) Suppose each firm's long run average cost curve, for positive levels of output, is given by AC 0.10.05Q+5/Q. The...

4) Suppose each firm's long run average cost curve, for positive levels of output, is given by AC 0.10.05Q+5/Q. The marginal cost curve is given by MC 0.+0.1Q. (a) Find the minimum efficient scale for the above cost function (b) What is the firm's minimum average cost? (c) Suppose you have many identical firms in a long run competitive equilibrium. Demand is P 13.1-0.040. What is the market quantity? How many firms are there? (d) Suppose demand increases to P...

4) Suppose each firm's long run average cost curve, for positive levels of output, is given by AC 0.10.05Q+5/Q. The marginal cost curve is given by MC 0.+0.1Q. (a) Find the minimum efficient scale for the above cost function (b) What is the firm's minimum average cost? (c) Suppose you have many identical firms in a long run competitive equilibrium. Demand is P 13.1-0.040. What is the market quantity? How many firms are there? (d) Suppose demand increases to P...

Suppose each firm's long run average cost curve, for positive levels of output, is given by AC = 0.1 + 0.05Q + 5/Q....

Suppose each firm's long run average cost curve, for positive levels of output, is given by AC = 0.1 + 0.05Q + 5/Q. The marginal cost curve is given by MC = 0.1 + 0.1Q. (a) Find the minimum efficient scale for the above cost function. (b) What is the firm's minimum average cost? (c) Suppose you have many identical firms in a long run competitive equilibrium. Demand is P = 13.1-0.04Q. What is the market quantity? How many firms...

If a $5 tax on each pack of cigarettes causes the market price of cigarettes to...

If a $5 tax on each pack of cigarettes causes the market price of cigarettes to increase by $2.50 then which of the following statements is true? consumers must be more elastic than producers consumers must be less elastic than producers consumers and producers must be equally elastic Question 42 (1 point) If the elasticity of demand is -1.8 and the elasticity of supply is 1, then consumers are than producers and the relative consumer burden will equal . Hint:...

If a $5 tax on each pack of cigarettes causes the market price of cigarettes to increase by $2.50 then which of the following statements is true? consumers must be more elastic than producers consumers must be less elastic than producers consumers and producers must be equally elastic Question 42 (1 point) If the elasticity of demand is -1.8 and the elasticity of supply is 1, then consumers are than producers and the relative consumer burden will equal . Hint:...

The handmade snuffbox industry is composed of 100 identical firms, each having short-run total costs given by 9.8. STC 0.5104 +5 and short-run marginal costs given by SMC q+10 where q is the output o...

The handmade snuffbox industry is composed of 100 identical firms, each having short-run total costs given by 9.8. STC 0.5104 +5 and short-run marginal costs given by SMC q+10 where q is the output of snuffboxes per day. a. What is the short-run supply curve for each snuff. box maker? What is the short-run supply curve for the market as a whole? b. Suppose the demand for total snuffbox production is given by Q 1,100-50P What is the equilibrium in...

The handmade snuffbox industry is composed of 100 identical firms, each having short-run total costs given by 9.8. STC 0.5104 +5 and short-run marginal costs given by SMC q+10 where q is the output of snuffboxes per day. a. What is the short-run supply curve for each snuff. box maker? What is the short-run supply curve for the market as a whole? b. Suppose the demand for total snuffbox production is given by Q 1,100-50P What is the equilibrium in...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

Suppose market demand for bread is given by the equation QD = 12-P while the market...

Suppose market demand for bread is given by the equation QD = 12-P while the market supply equation is Qs = 2P. a. Calculate the equilibrium price and quantity, consumer surplus, and producer surplus in the market for tires. Graph your results. b. Suppose the government imposes a tax on tire producers of $3 per tire. i. What price will the buyer pay? What is the burden to consumers? What amount per unit will the seller receive? What is the...

Suppose market demand for bread is given by the equation QD = 12-P while the market supply equation is Qs = 2P. a. Calculate the equilibrium price and quantity, consumer surplus, and producer surplus in the market for tires. Graph your results. b. Suppose the government imposes a tax on tire producers of $3 per tire. i. What price will the buyer pay? What is the burden to consumers? What amount per unit will the seller receive? What is the...

4) Suppose each firm's long run average cost curve, for positive levels of output, is given by AC 0.10.05Q+5/Q. The marginal cost curve is given by MC 0.+0.1Q. (a) Find the minimum efficient scale for the above cost function (b) What is the firm's minimum average cost? (c) Suppose you have many identical firms in a long run competitive equilibrium. Demand is P 13.1-0.040. What is the market quantity? How many firms are there? (d) Suppose demand increases to P...

4) Suppose each firm's long run average cost curve, for positive levels of output, is given by AC 0.10.05Q+5/Q. The marginal cost curve is given by MC 0.+0.1Q. (a) Find the minimum efficient scale for the above cost function (b) What is the firm's minimum average cost? (c) Suppose you have many identical firms in a long run competitive equilibrium. Demand is P 13.1-0.040. What is the market quantity? How many firms are there? (d) Suppose demand increases to P...

If a $5 tax on each pack of cigarettes causes the market price of cigarettes to increase by $2.50 then which of the following statements is true? consumers must be more elastic than producers consumers must be less elastic than producers consumers and producers must be equally elastic Question 42 (1 point) If the elasticity of demand is -1.8 and the elasticity of supply is 1, then consumers are than producers and the relative consumer burden will equal . Hint:...

If a $5 tax on each pack of cigarettes causes the market price of cigarettes to increase by $2.50 then which of the following statements is true? consumers must be more elastic than producers consumers must be less elastic than producers consumers and producers must be equally elastic Question 42 (1 point) If the elasticity of demand is -1.8 and the elasticity of supply is 1, then consumers are than producers and the relative consumer burden will equal . Hint:...

The handmade snuffbox industry is composed of 100 identical firms, each having short-run total costs given by 9.8. STC 0.5104 +5 and short-run marginal costs given by SMC q+10 where q is the output of snuffboxes per day. a. What is the short-run supply curve for each snuff. box maker? What is the short-run supply curve for the market as a whole? b. Suppose the demand for total snuffbox production is given by Q 1,100-50P What is the equilibrium in...

The handmade snuffbox industry is composed of 100 identical firms, each having short-run total costs given by 9.8. STC 0.5104 +5 and short-run marginal costs given by SMC q+10 where q is the output of snuffboxes per day. a. What is the short-run supply curve for each snuff. box maker? What is the short-run supply curve for the market as a whole? b. Suppose the demand for total snuffbox production is given by Q 1,100-50P What is the equilibrium in...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

1. (18pts) Suppose there are 100 firms in a perfectly competitive industry. Short run marginal costs for each firm are given by SMC = q + 2 and market demand is given by Qd = 1000-20P (5pts) Calculate the short run equilibrium price and quantity for each firm.. b. (3pts) Suppose each firm has a U-shaped, long-run average cost curve that reaches a minimum of $10. Calculate the long run equilibrium price and the total industry output.. (4pts) What is...

Suppose market demand for bread is given by the equation QD = 12-P while the market supply equation is Qs = 2P. a. Calculate the equilibrium price and quantity, consumer surplus, and producer surplus in the market for tires. Graph your results. b. Suppose the government imposes a tax on tire producers of $3 per tire. i. What price will the buyer pay? What is the burden to consumers? What amount per unit will the seller receive? What is the...

Suppose market demand for bread is given by the equation QD = 12-P while the market supply equation is Qs = 2P. a. Calculate the equilibrium price and quantity, consumer surplus, and producer surplus in the market for tires. Graph your results. b. Suppose the government imposes a tax on tire producers of $3 per tire. i. What price will the buyer pay? What is the burden to consumers? What amount per unit will the seller receive? What is the...

Most questions answered within 3 hours.

-

While rotating the tires on your car you notice a rock [mass =

0.1 Kg] stuck...

asked 1 hour ago -

Using MARS simulator, write MIPS programs according to

the following scenarios: Receive a positive integer number...

asked 2 hours ago -

An object in front of a concave mirror has a real image that is

11.5 cm...

asked 3 hours ago -

Consider the reaction, C3 H8 + O2 --> CO2 + H2O. How many

moles of O2...

asked 4 hours ago -

You and your opponent both roll a fair die. If you both roll the

same number,...

asked 5 hours ago -

In a study of the accuracy of fast food drive-through orders,

Restaurant A had 257 accurate...

asked 5 hours ago -

Identify and describe in detail the four categories of

institutions that could be included in a...

asked 5 hours ago -

In python

class Customer:

def __init__(self, customer_id, last_name, first_name, phone_number, address):

self._customer_id = int(customer_id)

self._last_name =...

asked 5 hours ago -

What is an example of a limitation in implementing a new

ERP system and how it...

asked 5 hours ago -

In a section of 9.7cm of an artery with a radius of 2.6mm there

is a...

asked 5 hours ago -

the two carboxylic acid groups of aspartic acid have different

acidities with pKa values of 2.1...

asked 5 hours ago -

Would CuCO3 aqueous salt combined with calcium chloride

form a solid precipitate? If so, what would...

asked 5 hours ago