Homework Answers

Solution:

Buyers(holders) of the option pay premium to the writers of the option.

Sellers(writers) of the options receive premium from the holders of the option.

Holder(Buyer) of call option exercise a call option only when the spot exchange rate is higher than the strike price.

Holder(Buyer) of put option exercise a put option only when the spot exchange rate is lower than the strike price.

Net profit of buyer of call option = max(0, spot price - strike price) - premium paid

Net profit of seller of call option = min(o, strike price - spot price) + premium received

Net profit of buyer of put option = max(o, strike price - spot price) + premium paid

Net profit of seller of put option = min(0, spot price - strike price) + premium received

| Spot Exchange Rate($/€) | 1.05 | 1.1 | 1.15 | 1.2 | 1.25 | 1.3 | |

| Sell Call Option | Does holder exercise? | no | no | no | yes | yes | yes |

| Holder's net profit per unit | -0.03 | -0.03 | -0.03 | -0.08 | -0.13 | -0.18 | |

| Sellers's net profit per unit | 0.03 | 0.03 | 0.03 | -0.02 | -0.07 | -0.12 | |

| Sell Put Option | Does holder exercise? | no | no | no | no | no | no |

| Holder's net profit per unit | -0.02 | -0.02 | -0.02 | -0.02 | -0.02 | -0.02 | |

| Sellers's net profit per unit | 0.02 | 0.02 | 0.02 | 0.02 | 0.02 | 0.02 | |

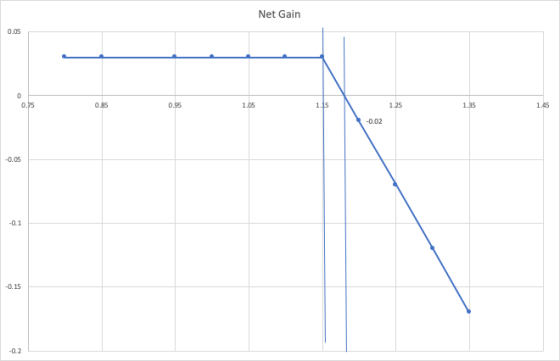

| Net Profit | 0.05 | 0.05 | 0.05 | -4.51E-17 | -0.05 | -0.1 | |

Break-even point for the seller of call option is when the spot price is equal to the strike price + premium received.

Break-even point for the seller of put option is when the spot price is equal to the strike price - premium received.

So in this case break even point on

short call option is 1.15+0.03 = 1.18 dollar/euro.

short put option id 1.05-0.02=1.03 dollar/euro.

There are 2 Break even points for a short strangle.

Lower Strike Price - Sum of premium received = 1.05 - (0.03+0.02) = 1 dollar/euro

Higher Strike Price + Sum of premium received = 1.15 + (0.02+0.03) = 1.2 dollar/euro

Graphs

| Write a Call | Write a Put | ||||||||||

| Spot Price | Holder Exer | Gross Gain | Premium | Net Gain | Holder E/L | Gross Gain | Premium | Net Gain | NET PROFIT | ||

| 0.8 | no | 0 | 0.03 | 0.03 | yes | -0.25 | 0.02 | -0.23 | -0.20 | ||

| 0.85 | no | 0 | 0.03 | 0.03 | yes | -0.2 | 0.02 | -0.18 | -0.15 | ||

| 0.95 | no | 0 | 0.03 | 0.03 | yes | -0.1 | 0.02 | -0.08 | -0.05 | ||

| 1 | no | 0 | 0.03 | 0.03 | yes | -0.05 | 0.02 | -0.03 | 0.00 | ||

| 1.05 | no | 0 | 0.03 | 0.03 | no | 0 | 0.02 | 0.02 | 0.05 | ||

| 1.1 | no | 0 | 0.03 | 0.03 | no | 0 | 0.02 | 0.02 | 0.05 | ||

| 1.15 | no | 0 | 0.03 | 0.03 | no | 0 | 0.02 | 0.02 | 0.05 | ||

| 1.2 | yes | -0.05 | 0.03 | -0.02 | no | 0 | 0.02 | 0.02 | 0.00 | ||

| 1.25 | yes | -0.1 | 0.03 | -0.07 | no | 0 | 0.02 | 0.02 | -0.05 | ||

| 1.3 | yes | -0.15 | 0.03 | -0.12 | no | 0 | 0.02 | 0.02 | -0.10 | ||

| 1.35 | yes | -0.2 | 0.03 | -0.17 | no | 0 | 0.02 | 0.02 | -0.15 | ||

SHORT CALL OPTION

breakeven point in this is 1.18 dollar/euro.

SHORT PUT OPTION

breakeven point for this is 1.03 dollar/euro

SHORT SRANGLE

breakeven points are 1 dollar/euro and 1.2 dollar/euro.

Add Answer to:

• Short currency strangle . Call option premium - $0.03/€, Put option premium - $0.028€ Call...

• Long cury strangle Call option premium - 50.03., Put option premium - $0.02 € Call...

• Long cury strangle Call option premium - 50.03., Put option premium - $0.02 € Call option strike price 1.25/6, Put option strike price $1.15 € Option contract size - €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium 1 S105 S 15E $1.20 € $1.25 € $1.30/E Long call option Spot exchange rate Exercise (NY) Holder's net profit per unit Exercise (NY Holder's net profit per unit Net profit...

• Long cury strangle Call option premium - 50.03., Put option premium - $0.02 € Call option strike price 1.25/6, Put option strike price $1.15 € Option contract size - €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium 1 S105 S 15E $1.20 € $1.25 € $1.30/E Long call option Spot exchange rate Exercise (NY) Holder's net profit per unit Exercise (NY Holder's net profit per unit Net profit...

Long currency straddle Call option premium = $0.05/€, Put option premium = $0.05/€ Strike price =...

Long currency straddle Call option premium = $0.05/€, Put option premium = $0.05/€ Strike price = $1.10/€, Option contract size = €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium Spot exchange rate $1.00/€ $1.05/€ $1.10/€ $1.15/€ $1.20/€ $1.25/€ Long call option Exercise (N/Y) Holder’s net profit per unit Long put option Exercise (N/Y) Holder’s net profit per unit Net profit Net profit per unit (graph) Short currency straddle Call...

Mark buys Call and Put options with different strike prices. Please read the following information. Call...

Mark buys Call and Put options with different strike prices. Please read the following information. Call option premium: $0.02/€ Put option premium: $0.01/€ Call option strike price: $1.15/€ Put option strike price: $1.05/€ Option contract size: €50,000 Break-even points for Mark are _______. a. None of the above b. $1.02/€ and $1.18/€ c. $1.08/€ and $1.12/€ d. $1.06/€ and $1.16/€

Q1: If Jasim purchase a put option on Canadian dollar from Sara for a premium of...

Q1: If Jasim purchase a put option on Canadian dollar from Sara for a premium of € 0.03, with an exercise price of € 0.42. The option will not be exercised until the expiration date, if at all. If the spot rate on the expiration date is € 0.37. a) What is the net profit for Jasim and Sara per unit? (1 mark) SZERE- ---ODDELEEEEEEEEEE -OOOOOOOOOOOOOOOOOOOOOOOOO SEBEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE b) If you know that one option contract represents 20000 units, what is...

Q1: If Jasim purchase a put option on Canadian dollar from Sara for a premium of € 0.03, with an exercise price of € 0.42. The option will not be exercised until the expiration date, if at all. If the spot rate on the expiration date is € 0.37. a) What is the net profit for Jasim and Sara per unit? (1 mark) SZERE- ---ODDELEEEEEEEEEE -OOOOOOOOOOOOOOOOOOOOOOOOO SEBEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE b) If you know that one option contract represents 20000 units, what is...

13. The premium on a pound put option is $.03 per unit. The exercise price is...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

(10 pts) I buy one CALL option on AMD with a strike price of $20.50.The option premium...

(10 pts) I buy one CALL option on AMD with a strike price of $20.50.The option premium is $100. Suppose the price of AMD is $35.00 a share and I choose to exercise the option. What are my total gains or losses? (10 pts) Using the information in question 6, what would my profit or loss be if I exercise the option when AMD has a market price of $21.00 per share? (10 pts) I buy one PUT option on Walmart...

Which one is the correct answer The premium on a pound put option is $0.03 per...

Which one is the correct answer

The premium on a pound put option is $0.03 per unit. The exercise price is $1.60. The break-even point is_for the buyer of the put, and__for the seller of the put. (Assume zero transaction costs and that the buyer and seller of the put option are speculators). a. $1.63; $1.57 b. $1.57; $1.57 C. $1.63; $1.63 d. $1.63; $1.60 9:38 PM

Which one is the correct answer

The premium on a pound put option is $0.03 per unit. The exercise price is $1.60. The break-even point is_for the buyer of the put, and__for the seller of the put. (Assume zero transaction costs and that the buyer and seller of the put option are speculators). a. $1.63; $1.57 b. $1.57; $1.57 C. $1.63; $1.63 d. $1.63; $1.60 9:38 PM

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium...

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium of S0.05/£. The strike price is $1.20/£. (a) Graph the profit/loss on the option contract. (b) What is the break-even price? (a) At what range of spot prices does John make profit? 2. Bank of America buys a call option on euros (contract size is €625,000) at a premium of $0.02 per euro. If the exercise price is $0.98 and the spot price of...

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium of S0.05/£. The strike price is $1.20/£. (a) Graph the profit/loss on the option contract. (b) What is the break-even price? (a) At what range of spot prices does John make profit? 2. Bank of America buys a call option on euros (contract size is €625,000) at a premium of $0.02 per euro. If the exercise price is $0.98 and the spot price of...

Suppose you construct the following European option trades on Apple stock: write a put option with exercise price $32 and premium $2.86, and write a call option with exercise price $32 and premium $3....

Suppose you construct the following European option trades on Apple stock: write a put option with exercise price $32 and premium $2.86, and write a call option with exercise price $32 and premium $3.51. What is your maximum dollar net profit, per share?

You sell a put option on one share of stock. The put has a premium of...

You sell a put option on one share of stock. The put has a premium of $4 and a strike/exercise price of $98. The stock currently has a price of $101.20 per share. On the day that the option expires, the stock is selling for $94. What ends up being your net payoff on this position?

• Long cury strangle Call option premium - 50.03., Put option premium - $0.02 € Call option strike price 1.25/6, Put option strike price $1.15 € Option contract size - €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium 1 S105 S 15E $1.20 € $1.25 € $1.30/E Long call option Spot exchange rate Exercise (NY) Holder's net profit per unit Exercise (NY Holder's net profit per unit Net profit...

• Long cury strangle Call option premium - 50.03., Put option premium - $0.02 € Call option strike price 1.25/6, Put option strike price $1.15 € Option contract size - €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium 1 S105 S 15E $1.20 € $1.25 € $1.30/E Long call option Spot exchange rate Exercise (NY) Holder's net profit per unit Exercise (NY Holder's net profit per unit Net profit...

Q1: If Jasim purchase a put option on Canadian dollar from Sara for a premium of € 0.03, with an exercise price of € 0.42. The option will not be exercised until the expiration date, if at all. If the spot rate on the expiration date is € 0.37. a) What is the net profit for Jasim and Sara per unit? (1 mark) SZERE- ---ODDELEEEEEEEEEE -OOOOOOOOOOOOOOOOOOOOOOOOO SEBEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE b) If you know that one option contract represents 20000 units, what is...

Q1: If Jasim purchase a put option on Canadian dollar from Sara for a premium of € 0.03, with an exercise price of € 0.42. The option will not be exercised until the expiration date, if at all. If the spot rate on the expiration date is € 0.37. a) What is the net profit for Jasim and Sara per unit? (1 mark) SZERE- ---ODDELEEEEEEEEEE -OOOOOOOOOOOOOOOOOOOOOOOOO SEBEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEEE b) If you know that one option contract represents 20000 units, what is...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

Which one is the correct answer

The premium on a pound put option is $0.03 per unit. The exercise price is $1.60. The break-even point is_for the buyer of the put, and__for the seller of the put. (Assume zero transaction costs and that the buyer and seller of the put option are speculators). a. $1.63; $1.57 b. $1.57; $1.57 C. $1.63; $1.63 d. $1.63; $1.60 9:38 PM

Which one is the correct answer

The premium on a pound put option is $0.03 per unit. The exercise price is $1.60. The break-even point is_for the buyer of the put, and__for the seller of the put. (Assume zero transaction costs and that the buyer and seller of the put option are speculators). a. $1.63; $1.57 b. $1.57; $1.57 C. $1.63; $1.63 d. $1.63; $1.60 9:38 PM

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium of S0.05/£. The strike price is $1.20/£. (a) Graph the profit/loss on the option contract. (b) What is the break-even price? (a) At what range of spot prices does John make profit? 2. Bank of America buys a call option on euros (contract size is €625,000) at a premium of $0.02 per euro. If the exercise price is $0.98 and the spot price of...

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium of S0.05/£. The strike price is $1.20/£. (a) Graph the profit/loss on the option contract. (b) What is the break-even price? (a) At what range of spot prices does John make profit? 2. Bank of America buys a call option on euros (contract size is €625,000) at a premium of $0.02 per euro. If the exercise price is $0.98 and the spot price of...

Most questions answered within 3 hours.

-

Write a program to score the paper-rock-scissor game. Each of

two users types in either P,R...

asked 5 minutes ago -

Calculate the equillibrium constent K for a redox reaction that

has E°cell = -.98 V at...

asked 17 minutes ago -

A concave spherical mirror has a radius of curvature of

magnitude 19.6 cm.

(a) Find the...

asked 18 minutes ago -

3. draw a diagram of the magnetic field:

a. around a long straight wire with a...

asked 17 minutes ago -

If you titrated 30.0 mL of 0.1 M HCl with 0.1 M NaOH, indicate

the approximate...

asked 25 minutes ago -

NADH passes electrons into the electron transport chain. List

the carriers that would receive the electrons,...

asked 34 minutes ago -

A cylindrical cable with a resistivity of 1.6x10-8 Ω·m and cross

sectional area of 3x10-5 m^2...

asked 34 minutes ago -

True or False.

A consumer with convex preferences who is indifferent between

the bundles (5,2) and...

asked 37 minutes ago -

A diamond's index of refraction for red light, 656 nm, is 2.410,

while that for blue...

asked 50 minutes ago -

Compare HPLC, SPE, and GC. Identify the differences, the

advantages, and the weaknesses of each method.

asked 51 minutes ago -

Characteristic x-rays emitted by potassium have a wavelength of

0.374 nm. What is the energy of...

asked 54 minutes ago -

there is a function to create two random numbers between 1 and

25 and a function...

asked 1 hour ago