Homework Answers

Long currency strangle involves taking a long position in a call option of a higher strike, and a long position in a put option of a lower strike.

Payoff of a long call option = Max[S-X, 0] - P

Payoff of a long put option = Max[X-S, 0] - P

S = underlying price at expiry,

X = strike price

P = premium paid or received (long options involve paying premium, and short options receive premium)

A long call will be exercised if the spot price is higher than the strike price

A long put will be exercised if the spot price is lower than the strike price

Add Answer to:

• Long cury strangle Call option premium - 50.03., Put option premium - $0.02 € Call...

• Short currency strangle . Call option premium - $0.03/€, Put option premium - $0.028€ Call...

• Short currency strangle . Call option premium - $0.03/€, Put option premium - $0.028€ Call option strike price = $1.15/€, Put option strike price - $1.05/€ Option contract size = €62,500 Draw graphs of call option, put option, and straddle • Mark BE point and Strike prices • Mark each premium $1.05/€ $1.10/€ $1.15/€ | $1.20/€ $1.25/€ $1.30/€ Spot exchange rate Does holder exercise? Sell call option Holder's net profit per unit Seller's net profit per unit Does holder...

• Short currency strangle . Call option premium - $0.03/€, Put option premium - $0.028€ Call option strike price = $1.15/€, Put option strike price - $1.05/€ Option contract size = €62,500 Draw graphs of call option, put option, and straddle • Mark BE point and Strike prices • Mark each premium $1.05/€ $1.10/€ $1.15/€ | $1.20/€ $1.25/€ $1.30/€ Spot exchange rate Does holder exercise? Sell call option Holder's net profit per unit Seller's net profit per unit Does holder...

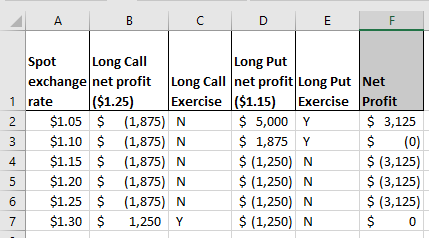

Long currency straddle Call option premium = $0.05/€, Put option premium = $0.05/€ Strike price =...

Long currency straddle Call option premium = $0.05/€, Put option premium = $0.05/€ Strike price = $1.10/€, Option contract size = €62,500 Draw graphs of call option, put option, and straddle Mark BE point and Strike prices Mark each premium Spot exchange rate $1.00/€ $1.05/€ $1.10/€ $1.15/€ $1.20/€ $1.25/€ Long call option Exercise (N/Y) Holder’s net profit per unit Long put option Exercise (N/Y) Holder’s net profit per unit Net profit Net profit per unit (graph) Short currency straddle Call...

Mark buys Call and Put options with different strike prices. Please read the following information. Call...

Mark buys Call and Put options with different strike prices. Please read the following information. Call option premium: $0.02/€ Put option premium: $0.01/€ Call option strike price: $1.15/€ Put option strike price: $1.05/€ Option contract size: €50,000 Break-even points for Mark are _______. a. None of the above b. $1.02/€ and $1.18/€ c. $1.08/€ and $1.12/€ d. $1.06/€ and $1.16/€

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium...

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium of S0.05/£. The strike price is $1.20/£. (a) Graph the profit/loss on the option contract. (b) What is the break-even price? (a) At what range of spot prices does John make profit? 2. Bank of America buys a call option on euros (contract size is €625,000) at a premium of $0.02 per euro. If the exercise price is $0.98 and the spot price of...

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium of S0.05/£. The strike price is $1.20/£. (a) Graph the profit/loss on the option contract. (b) What is the break-even price? (a) At what range of spot prices does John make profit? 2. Bank of America buys a call option on euros (contract size is €625,000) at a premium of $0.02 per euro. If the exercise price is $0.98 and the spot price of...

A trader creates a long strangle with put options with a strike price of $160 per...

A trader creates a long strangle with put options with a strike price of $160 per share, and call options with a strike price of $170 per share by trading a total of 20 option contracts (10 put contracts and 10 call contracts). Each contract is written on 100 shares of stock. The put option is worth $18 per share, and the call option is worth $15 per share. What is the value (payoff) of the strangle at maturity as...

A trader creates a long strangle with put options with a strike price of $160 per...

A trader creates a long strangle with put options with a strike price of $160 per share, and call options with a strike price of $170 per share by trading a total of 20 option contracts (10 put contracts and 10 call contracts). Each contract is written on 100 shares of stock. The put option is worth $18 per share, and the call option is worth $15 per share. What is the value (payoff) of the strangle at maturity as...

Why with 'long strangle', the loss is decreased if price remains unchanged, compared with 'long straddle'? Why the loss sustained by investors would be the double premium ( long strang...

Why with 'long strangle', the loss is decreased if price remains

unchanged, compared with 'long straddle'?

Why the loss sustained by investors would be the double premium

( long strangle) which is same as the loss ( long straddle) equal

to double premium.

Market price of asset Premium- LOSS (c) Long call+ long put Profit Price expectations Market price of asset Net (double premium Loss c) Long put + long call Profit Price expectations ㅡ ㅡ ㅡㅡ Market p of...

Why with 'long strangle', the loss is decreased if price remains

unchanged, compared with 'long straddle'?

Why the loss sustained by investors would be the double premium

( long strangle) which is same as the loss ( long straddle) equal

to double premium.

Market price of asset Premium- LOSS (c) Long call+ long put Profit Price expectations Market price of asset Net (double premium Loss c) Long put + long call Profit Price expectations ㅡ ㅡ ㅡㅡ Market p of...

13. The premium on a pound put option is $.03 per unit. The exercise price is...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

IBM sells a call option on euros (contract size is €600,000) at a premium of $0.02...

IBM sells a call option on euros (contract size is €600,000) at a premium of $0.02 per euro. If the exercise price is $1.44/€ and the spot price of the euro at date of expiration is $1.45/€, A. Will this option be exercised, that is, is in-the-money or out-of-the-money? Why? (2 points) B. What is IBM’s profit (or loss) on the call option? (3 points)

Compute the upper and lower breakeven point for a strangle. The exercise price on call option...

Compute the upper and lower breakeven point for a strangle. The exercise price on call option is $1.72 and the exercise price on put option is $1.55. The premium on put option is $0.014 and premium on call option is $0.01. a. $1.526 and -$1.744 b. $1.744 and $1.526 c. $1.734 and $1.526 d. $1.744 and $1.574

Compute the upper and lower breakeven point for a strangle. The exercise price on call option is $1.72 and the exercise price on put option is $1.55. The premium on put option is $0.014 and premium on call option is $0.01. a. $1.526 and -$1.744 b. $1.744 and $1.526 c. $1.734 and $1.526 d. $1.744 and $1.574

• Short currency strangle . Call option premium - $0.03/€, Put option premium - $0.028€ Call option strike price = $1.15/€, Put option strike price - $1.05/€ Option contract size = €62,500 Draw graphs of call option, put option, and straddle • Mark BE point and Strike prices • Mark each premium $1.05/€ $1.10/€ $1.15/€ | $1.20/€ $1.25/€ $1.30/€ Spot exchange rate Does holder exercise? Sell call option Holder's net profit per unit Seller's net profit per unit Does holder...

• Short currency strangle . Call option premium - $0.03/€, Put option premium - $0.028€ Call option strike price = $1.15/€, Put option strike price - $1.05/€ Option contract size = €62,500 Draw graphs of call option, put option, and straddle • Mark BE point and Strike prices • Mark each premium $1.05/€ $1.10/€ $1.15/€ | $1.20/€ $1.25/€ $1.30/€ Spot exchange rate Does holder exercise? Sell call option Holder's net profit per unit Seller's net profit per unit Does holder...

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium of S0.05/£. The strike price is $1.20/£. (a) Graph the profit/loss on the option contract. (b) What is the break-even price? (a) At what range of spot prices does John make profit? 2. Bank of America buys a call option on euros (contract size is €625,000) at a premium of $0.02 per euro. If the exercise price is $0.98 and the spot price of...

1. Adam buys a put option on British pounds (contract size is £500,000) at a premium of S0.05/£. The strike price is $1.20/£. (a) Graph the profit/loss on the option contract. (b) What is the break-even price? (a) At what range of spot prices does John make profit? 2. Bank of America buys a call option on euros (contract size is €625,000) at a premium of $0.02 per euro. If the exercise price is $0.98 and the spot price of...

Why with 'long strangle', the loss is decreased if price remains

unchanged, compared with 'long straddle'?

Why the loss sustained by investors would be the double premium

( long strangle) which is same as the loss ( long straddle) equal

to double premium.

Market price of asset Premium- LOSS (c) Long call+ long put Profit Price expectations Market price of asset Net (double premium Loss c) Long put + long call Profit Price expectations ㅡ ㅡ ㅡㅡ Market p of...

Why with 'long strangle', the loss is decreased if price remains

unchanged, compared with 'long straddle'?

Why the loss sustained by investors would be the double premium

( long strangle) which is same as the loss ( long straddle) equal

to double premium.

Market price of asset Premium- LOSS (c) Long call+ long put Profit Price expectations Market price of asset Net (double premium Loss c) Long put + long call Profit Price expectations ㅡ ㅡ ㅡㅡ Market p of...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

13. The premium on a pound put option is $.03 per unit. The exercise price is s1.60. The break-even point for the buyer and seller is? (Assume put option are speculators.) zero transactions costs and that the buyer and seller of the 14. You purchase a call option on pounds for a premium of $.03 per unit, with an exercise price of $1.64; the option will not be exercised until the expiration date, if at all. If the spot rate...

Compute the upper and lower breakeven point for a strangle. The exercise price on call option is $1.72 and the exercise price on put option is $1.55. The premium on put option is $0.014 and premium on call option is $0.01. a. $1.526 and -$1.744 b. $1.744 and $1.526 c. $1.734 and $1.526 d. $1.744 and $1.574

Compute the upper and lower breakeven point for a strangle. The exercise price on call option is $1.72 and the exercise price on put option is $1.55. The premium on put option is $0.014 and premium on call option is $0.01. a. $1.526 and -$1.744 b. $1.744 and $1.526 c. $1.734 and $1.526 d. $1.744 and $1.574

Most questions answered within 3 hours.

-

The blues made its way into many kinds of music. Eric Clapton,

The Beatles, and Elvis...

asked 22 minutes ago -

If you’re standing at the bottom of a hill and asked to evaluate

it while being...

asked 1 hour ago -

1. Which region has taken the lead in the world of

e-waste handling?

a) European Union...

asked 1 hour ago -

A 8.15- g bullet from a 9-mm pistol has a velocity of 366.0 m/s.

It strikes...

asked 2 hours ago -

The outstanding bonds of Alpha Extracts have a yield to maturity

of 7.4 percent and a...

asked 2 hours ago -

The Problem: The Case of the Harmonizing Vacations

Your CEO is exploring partnering with a European...

asked 4 hours ago -

A chemical equation is balanced by adding coefficients in front

of some formulas so that the...

asked 4 hours ago -

From the literature (reference your sources): What are the

lattice parameters of calcite and aragonite? Why...

asked 4 hours ago -

Your system is rejecting the question am asking which is

preceded by a case study. It...

asked 4 hours ago -

3. On January 2, 2000, Larry creates a trust with himself as

trustee. Larry as trustee...

asked 4 hours ago -

A member of the volleyball team spikes the ball. During this

process, she changes the velocity...

asked 4 hours ago -

Are adult gamers less likely to use a gaming console (Xbox,

PlayStation, Wii, etc...) than teen...

asked 5 hours ago