Airbus sold an aircraft, A400, to Delta Airlines, a U.S. company, and billed $30 million payable...

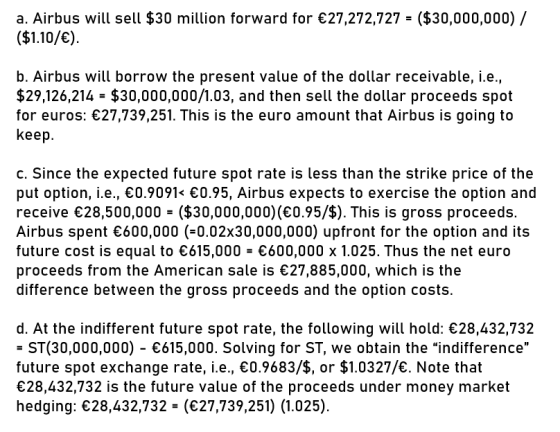

Airbus sold an aircraft, A400, to Delta Airlines, a U.S. company, and billed $30 million payable in six months. Airbus is concerned with the euro proceeds from international sales and would like to control exchange risk. The current spot exchange rate is $1.05/€ and six-month forward exchange rate is $1.10/€ at the moment. Airbus can buy a six-month put option on U.S. dollars with a strike price of €0.95/$ for a premium of €0.02 per U.S. dollar. Currently, six-month interest rate is 2.5% in the euro zone and 3.0% in the U.S.

- Compute the guaranteed euro proceeds from the American sale if Airbus decides to hedge using a forward contract.

b. If Airbus decides to hedge using money market instruments, what action does Airbus need to take? What would be the guaranteed euro proceeds from the American sale in this case?

c. If Airbus decides to hedge using put options on U.S. dollars, what would be the ‘expected’ euro proceeds from the American sale? Assume that Airbus regards the current forward exchange rate as an unbiased predictor of the future spot exchange rate.

d. At what future spot exchange rate do you think Airbus will be indifferent between the option and money market hedge?

Homework Answers

I have answered the question below

Please up vote for the same and thanks!!!

Do reach out in the comments for any queries

Answer:

Add Answer to:

Airbus sold an aircraft, A400, to Delta Airlines, a U.S.

company, and billed $30 million payable...

1. Jennifer Magnussen, a currency trader for Chicago-based Black River Investments, uses the following futures quotes...

1. Jennifer Magnussen, a currency trader for Chicago-based Black River Investments, uses the following futures quotes on the British pound to speculate on the value of the British pound. British Pound Futures, US$/pound (CME) Contract = 62,500 pounds Open Maturity Open High Low Settle Change High Interest March 1.4246 1.4268 1.4214 1.4228 0.0032 1.4700 25,605 June 1.4164 1.4188 1.4146 1.4162 0.0030 1.4550 809 a) If Jennifer buys 3 March pound futures, and the spot rate at maturity is $1.4560/pound, what...

General Electric sold a machine system to a customer in the UK and billed £30 million...

General Electric sold a machine system to a customer in the UK and billed £30 million payable in one year. GE is concerned with the pound proceeds from international sales and would like to control exchange rate risk. The current spot exchange rate is $1.29/£ and one-year forward exchange rate is $1.27/£ at the moment. GE can buy a one-year put option on £30 million with a strike price of $1.32/£ for a premium of $0.02 per pound. It can...

Norton Corp. sold a computer system to a customer in the UK and billed £20 million...

Norton Corp. sold a computer system to a customer in the UK and billed £20 million receivable in one year. Norton would like to control for the exchange rate risk. The current spot exchange rate is $1.30/£ and one-year forward exchange rate is $1.27/£ at the moment. Norton can buy a one-year put option on £20 million with a strike price of $1.32/£ for a premium of $0.02 per pound. It can also buy a one-year call option on £20...

Boeing just signed a contract to sell a Boeing 737 aircraft to British Airways and will...

Boeing just signed a contract to sell a Boeing 737 aircraft to British Airways and will receive £60 million in six months. The current spot exchange rate is $1.3800/£ and the six-month forward rate is $1.4000/£. Boeing can buy a six-month put option on the British pound with an exercise price of $1.3500/£ for a premium of $0.020/£. Currently, the six-month interest rate is 1.880 percent per annum in the United States and 0.700 percent per annum in the UK....

A U.S. company has a ¥750 million payable due in one year to a bank in...

A U.S. company has a ¥750 million payable due in one year to a bank in Japan. The current spot rate S($/¥) = $0.0086/ ¥ and the one - year forward rate F 360 ($/¥)= $0.0092/¥. The annual interest rate is 3 percent in Japan and 6 percent in the United States. a. How to implement a hedge using a forward contract? Compute the guaranteed dollar payment in one year using the forward hedge. b. How to implement a money...

A U.S. company has a ¥50 million payable due in one year to a bank in...

A U.S. company has a ¥50 million payable due in one year to a bank in Japan. The current spot rate S($/¥) = $0.0086/ ¥ and the one-year forward rate F360($/ ¥) = $0.0092/ ¥. The annual interest rate is 3 percent in Japan and 6 percent in the United States. a. How to implement a hedge using a forward contract? Compute the guaranteed dollar payment in one year using the forward hedge. b. How to implement a money market...

A U.S. company has a ¥50 million payable due in one year to a bank in Japan. The current spot rate S($/¥) = $0.0086/ ¥ and the one-year forward rate F360($/ ¥) = $0.0092/ ¥. The annual interest rate is 3 percent in Japan and 6 percent in the United States. a. How to implement a hedge using a forward contract? Compute the guaranteed dollar payment in one year using the forward hedge. b. How to implement a money market...

4 pts Question 2 Boeing just signeda contract to sell a Boeing 737 aircraft to Air...

4 pts Question 2 Boeing just signeda contract to sell a Boeing 737 aircraft to Air France. Air France will be billed €50 million which is payable in one year. Tbe current spot exchange rate is $1.1/€ and the one-year forward rate is $1.20/€. The annual interest rate is 5.0% in the U.S. and 2.0 % in France. Boeing is concerned with the volati le exchange rate between the dollar and the euro and would like to hedge exchange exposure....

4 pts Question 2 Boeing just signeda contract to sell a Boeing 737 aircraft to Air France. Air France will be billed €50 million which is payable in one year. Tbe current spot exchange rate is $1.1/€ and the one-year forward rate is $1.20/€. The annual interest rate is 5.0% in the U.S. and 2.0 % in France. Boeing is concerned with the volati le exchange rate between the dollar and the euro and would like to hedge exchange exposure....

IBM purchased computer chips from NEC, a Japanese electronics concern, and was billed ¥300 million payable...

IBM purchased computer chips from NEC, a Japanese electronics concern, and was billed ¥300 million payable in 6 months. Currently, the spot exchange rate is ¥110/$ and the six-month forward rate is ¥100/$. The six-month money market interest rate is 2 percent per annum in the U.S. and 1.5 percent per annum in Japan. The management of IBM decided to use the money market hedge to deal with this yen account payable. A. Explain the process of a money market...

FML Company in the U.S. has just signed a contract to purchase light rail cars from...

FML Company in the U.S. has just signed a contract to purchase light rail cars from a manufacturer in Germany for euro 2,500,000. The purchase was made in June with payment in euro due six months later in December. Assume that in December, the axchange rate turns out to be as the company anticipated. If so, then the money market hedge turns out to be ____ than the unhedged position by ______. The spot exchange rate is $1.40/euro The six...

1. Plains States Manufacturing has just signed a contract to sell agricultural equipment to Boschin, a...

1. Plains States Manufacturing has just signed a contract to sell agricultural equipment to Boschin, a German firm, for €1,250,000. The sale was made in June with payment due six months later in December. Because this is a sizable contract for the firm and because the contract is in Euros rather than dollars, Plains States is considering several hedging alternatives to reduce the exchange rate risk arising from the sale. To help the firm make a hedging decision you have...

A U.S. company has a ¥50 million payable due in one year to a bank in Japan. The current spot rate S($/¥) = $0.0086/ ¥ and the one-year forward rate F360($/ ¥) = $0.0092/ ¥. The annual interest rate is 3 percent in Japan and 6 percent in the United States. a. How to implement a hedge using a forward contract? Compute the guaranteed dollar payment in one year using the forward hedge. b. How to implement a money market...

A U.S. company has a ¥50 million payable due in one year to a bank in Japan. The current spot rate S($/¥) = $0.0086/ ¥ and the one-year forward rate F360($/ ¥) = $0.0092/ ¥. The annual interest rate is 3 percent in Japan and 6 percent in the United States. a. How to implement a hedge using a forward contract? Compute the guaranteed dollar payment in one year using the forward hedge. b. How to implement a money market...

4 pts Question 2 Boeing just signeda contract to sell a Boeing 737 aircraft to Air France. Air France will be billed €50 million which is payable in one year. Tbe current spot exchange rate is $1.1/€ and the one-year forward rate is $1.20/€. The annual interest rate is 5.0% in the U.S. and 2.0 % in France. Boeing is concerned with the volati le exchange rate between the dollar and the euro and would like to hedge exchange exposure....

4 pts Question 2 Boeing just signeda contract to sell a Boeing 737 aircraft to Air France. Air France will be billed €50 million which is payable in one year. Tbe current spot exchange rate is $1.1/€ and the one-year forward rate is $1.20/€. The annual interest rate is 5.0% in the U.S. and 2.0 % in France. Boeing is concerned with the volati le exchange rate between the dollar and the euro and would like to hedge exchange exposure....

Most questions answered within 3 hours.

-

A man is standing 3.40 m in front of a convex spherical mirror

of radius of...

asked 30 minutes ago -

Match the annual percentage rate to each of these trade credit

terms:

__ 1/5, NET 60...

asked 31 minutes ago -

You are a statistician and wish to estimate, with 90%

confidence, the proportion of adults who...

asked 27 minutes ago -

ORGANIC CHEMISTRY QUESTION 5

PART A--------

Describe a chemical test for the identification of a double...

asked 4 hours ago -

Both Terence and Tong work at a local actuarial consulting firm

in Des Moines.

Terence arrives...

asked 4 hours ago -

QUESTION 11

. THE RESTING POTENTIAL IS CAUSED BY

.

. A.

. the rotation of...

asked 4 hours ago -

Need them in c++

1. Give the code for the

definition of a node for

the linked implementation of

a tree that contains...

asked 4 hours ago -

For sputtering-cleaning and sputter-depositing a metal,

would you use an AC or DC plasma? Explain your...

asked 4 hours ago -

Defend ONE of the following statements:

Prices should reflect the value consumers are willing to

pay....

asked 4 hours ago -

A magnet of mass 0.10 kg is dropped from rest and falls

vertically through a 20.0...

asked 4 hours ago -

A friend approaches you about a nutritional product and ask you

if it is worth it....

asked 4 hours ago -

What is bacterial transformation? What are the differences and

similarities between transforming a bacterial cell with...

asked 4 hours ago