Homework Answers

Add Answer to:

In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad-based fund...

In addition to nsk-free securities, you are currently invested in the Tanglewood Fund, a broad-based fund...

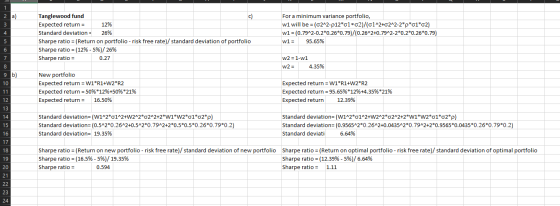

In addition to nsk-free securities, you are currently invested in the Tanglewood Fund, a broad-based fund o stocks and other securities than expected return o 12% and a volatility of 25%. Currently, the nsk-free rate terest is 4%. Your broker suggests that you add a venture capital und to your current portfolio. The venture capital fund has an expected return of 20%, a volatility of 80%, and a correlation of 0.2 with the Tanglewood Fund. Assume you follow your broker's...

In addition to nsk-free securities, you are currently invested in the Tanglewood Fund, a broad-based fund o stocks and other securities than expected return o 12% and a volatility of 25%. Currently, the nsk-free rate terest is 4%. Your broker suggests that you add a venture capital und to your current portfolio. The venture capital fund has an expected return of 20%, a volatility of 80%, and a correlation of 0.2 with the Tanglewood Fund. Assume you follow your broker's...

how to solve this question? I want to know whether my solution is correct. <My solution>...

how to solve this question? I want to know whether my

solution is correct.

<My solution>

the 9.12% is the required return for venture capital

fund in the current portfolio of Tanglewood,

and the expected return of venture capital fund is

20%, so

20% > 9.12% makes it conclude that we should add

more venture capital funds in the portfolio.

11-38. In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad- based fund of stocks...

how to solve this question? I want to know whether my

solution is correct.

<My solution>

the 9.12% is the required return for venture capital

fund in the current portfolio of Tanglewood,

and the expected return of venture capital fund is

20%, so

20% > 9.12% makes it conclude that we should add

more venture capital funds in the portfolio.

11-38. In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad- based fund of stocks...

40. You are currently only invested in the Natasha Fund (aside from risk-free securities). It has...

40. You are currently only invested in the Natasha Fund (aside from risk-free securities). It has an expected return of 14% with a volatility of 20%. Currently, the risk-free rate of interest is 3.8%. Your broker suggests that you add Hannah Corporation to your portfolio. Hannah Corporation has an expected return of 20%, a volatility of 60%, and a correlation of 0 with the Natasha Fund. a. Is your broker right? b. You follow your broker's advice and make a...

40. You are currently only invested in the Natasha Fund (aside from risk-free securities). It has an expected return of 14% with a volatility of 20%. Currently, the risk-free rate of interest is 3.8%. Your broker suggests that you add Hannah Corporation to your portfolio. Hannah Corporation has an expected return of 20%, a volatility of 60%, and a correlation of 0 with the Natasha Fund. a. Is your broker right? b. You follow your broker's advice and make a...

The Bold part is the problem, and the non-Bold part is the solution. Why is the...

The Bold part is the problem, and the non-Bold part is the

solution.

Why is the solution like that? Please explain this solution!

11-38. In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad- based fund of stocks and other securities with an expected return of 12% and a volatility of 25%. Currently, the risk-free rate of interest is 4%. Your broker suggests that you add a venture capital fund to your current portfolio. The...

The Bold part is the problem, and the non-Bold part is the

solution.

Why is the solution like that? Please explain this solution!

11-38. In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad- based fund of stocks and other securities with an expected return of 12% and a volatility of 25%. Currently, the risk-free rate of interest is 4%. Your broker suggests that you add a venture capital fund to your current portfolio. The...

You are presently invested in the Luther Fund, a broad based mutual fund that invests in 7. (10 pts.) stocks and other securities. The Luther Fund has an expected return of 14% and a volatility of 20...

You are presently invested in the Luther Fund, a broad based mutual fund that invests in 7. (10 pts.) stocks and other securities. The Luther Fund has an expected return of 14% and a volatility of 20%. Risk-free Treasury bills are currently offering returns of 4%. You are considering adding a precious metals fund to your current portfolio. The metals fund has an expected return of 10%, a volatility of 30%, and a correlation of-20 with the Luther Fund. Will...

You are presently invested in the Luther Fund, a broad based mutual fund that invests in 7. (10 pts.) stocks and other securities. The Luther Fund has an expected return of 14% and a volatility of 20%. Risk-free Treasury bills are currently offering returns of 4%. You are considering adding a precious metals fund to your current portfolio. The metals fund has an expected return of 10%, a volatility of 30%, and a correlation of-20 with the Luther Fund. Will...

You are currently only invested in the Natasha Fund (aside from risk-free securities). It has an...

You are currently only invested in the Natasha Fund (aside from risk-free securities). It has an expected return of 14% with a volatility of 21%. Currently, the risk-free rate of interest is 3.1%. Your broker suggests that you add Hannah Corporation to your portfolio. Hannah Corporation has an expected return of 19%, a volatility of 58%, and a correlation of 0 (zero) with the Natasha Fund. Hint: Make sure to round all intermediate calculations to at least five decimal places...

(15) You have invested only in the BlueChip Fund, a mutual fund that invests mainly in...

(15) You have invested only in the BlueChip Fund, a mutual fund that invests mainly in stocks. At the moment, the BlueChip Fund has a volatility of 32%. Your broker suggests that you add the GoldAll Fund to your current portfolio. The GoldAll Fund has a volatility of 35% and a correlation of -0.10 with the BlueChip Fund. Risk-free interest rate is equal to 5%. The required return on the GoldAll Fund is closest to: Volatility Comelation ВСЕ 3 .....

(15) You have invested only in the BlueChip Fund, a mutual fund that invests mainly in stocks. At the moment, the BlueChip Fund has a volatility of 32%. Your broker suggests that you add the GoldAll Fund to your current portfolio. The GoldAll Fund has a volatility of 35% and a correlation of -0.10 with the BlueChip Fund. Risk-free interest rate is equal to 5%. The required return on the GoldAll Fund is closest to: Volatility Comelation ВСЕ 3 .....

please help with step no excel :) 5) You have invested only in the BlueChip Fund,...

please help with step no excel :)

5) You have invested only in the BlueChip Fund, a mutual fund that invests mainly in stocks. At the moment, the Blue Chip Fund has a volatility of 32%. Your broker suggests that you add the GoldAll Fund to your current portfolio. The GoldAll Fund has a volatility of 35% and a correlation of -0.10 with the BlueChip Fund. Risk-free interest rate is equal to 5%. The required return on the GoldAll Fund...

please help with step no excel :)

5) You have invested only in the BlueChip Fund, a mutual fund that invests mainly in stocks. At the moment, the Blue Chip Fund has a volatility of 32%. Your broker suggests that you add the GoldAll Fund to your current portfolio. The GoldAll Fund has a volatility of 35% and a correlation of -0.10 with the BlueChip Fund. Risk-free interest rate is equal to 5%. The required return on the GoldAll Fund...

You wish to invest in a portfolio of stocks A and B. The risk free rate...

You wish to invest in a portfolio of stocks A and B. The risk free rate is 4%. A B Expected return (%) 10 20 Volatility (%) 15 22 Correlation between returns 0.3 Complete the following table for each portfolio Which portfolio has the highest reward to risk (with risk measured as volatility)? Portfolio % in A Expected Return Standard Deviation of Return Sharpe Ratio 1 30% 2 40% 3 50%

The risk-free rate is 0%. The market portfolio has an expected return of 20% and a volatility of 20%. You have $100 to invest. You decide to build a portfolio P which invests in both the risk-free investment and the market portfolio.

The risk-free rate is 0%. The market portfolio has an expected return of 20% and a volatility of 20%. You have $100 to invest. You decide to build a portfolio P which invests in both the risk-free investment and the market portfolio.a. How much should you invest in the market portfolio and the risk-free investment if you want portfolio P to have an expected return of 40%?b. How much should you invest in the market portfolio and the risk-free investment...

In addition to nsk-free securities, you are currently invested in the Tanglewood Fund, a broad-based fund o stocks and other securities than expected return o 12% and a volatility of 25%. Currently, the nsk-free rate terest is 4%. Your broker suggests that you add a venture capital und to your current portfolio. The venture capital fund has an expected return of 20%, a volatility of 80%, and a correlation of 0.2 with the Tanglewood Fund. Assume you follow your broker's...

In addition to nsk-free securities, you are currently invested in the Tanglewood Fund, a broad-based fund o stocks and other securities than expected return o 12% and a volatility of 25%. Currently, the nsk-free rate terest is 4%. Your broker suggests that you add a venture capital und to your current portfolio. The venture capital fund has an expected return of 20%, a volatility of 80%, and a correlation of 0.2 with the Tanglewood Fund. Assume you follow your broker's...

how to solve this question? I want to know whether my

solution is correct.

<My solution>

the 9.12% is the required return for venture capital

fund in the current portfolio of Tanglewood,

and the expected return of venture capital fund is

20%, so

20% > 9.12% makes it conclude that we should add

more venture capital funds in the portfolio.

11-38. In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad- based fund of stocks...

how to solve this question? I want to know whether my

solution is correct.

<My solution>

the 9.12% is the required return for venture capital

fund in the current portfolio of Tanglewood,

and the expected return of venture capital fund is

20%, so

20% > 9.12% makes it conclude that we should add

more venture capital funds in the portfolio.

11-38. In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad- based fund of stocks...

40. You are currently only invested in the Natasha Fund (aside from risk-free securities). It has an expected return of 14% with a volatility of 20%. Currently, the risk-free rate of interest is 3.8%. Your broker suggests that you add Hannah Corporation to your portfolio. Hannah Corporation has an expected return of 20%, a volatility of 60%, and a correlation of 0 with the Natasha Fund. a. Is your broker right? b. You follow your broker's advice and make a...

40. You are currently only invested in the Natasha Fund (aside from risk-free securities). It has an expected return of 14% with a volatility of 20%. Currently, the risk-free rate of interest is 3.8%. Your broker suggests that you add Hannah Corporation to your portfolio. Hannah Corporation has an expected return of 20%, a volatility of 60%, and a correlation of 0 with the Natasha Fund. a. Is your broker right? b. You follow your broker's advice and make a...

The Bold part is the problem, and the non-Bold part is the

solution.

Why is the solution like that? Please explain this solution!

11-38. In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad- based fund of stocks and other securities with an expected return of 12% and a volatility of 25%. Currently, the risk-free rate of interest is 4%. Your broker suggests that you add a venture capital fund to your current portfolio. The...

The Bold part is the problem, and the non-Bold part is the

solution.

Why is the solution like that? Please explain this solution!

11-38. In addition to risk-free securities, you are currently invested in the Tanglewood Fund, a broad- based fund of stocks and other securities with an expected return of 12% and a volatility of 25%. Currently, the risk-free rate of interest is 4%. Your broker suggests that you add a venture capital fund to your current portfolio. The...

You are presently invested in the Luther Fund, a broad based mutual fund that invests in 7. (10 pts.) stocks and other securities. The Luther Fund has an expected return of 14% and a volatility of 20%. Risk-free Treasury bills are currently offering returns of 4%. You are considering adding a precious metals fund to your current portfolio. The metals fund has an expected return of 10%, a volatility of 30%, and a correlation of-20 with the Luther Fund. Will...

You are presently invested in the Luther Fund, a broad based mutual fund that invests in 7. (10 pts.) stocks and other securities. The Luther Fund has an expected return of 14% and a volatility of 20%. Risk-free Treasury bills are currently offering returns of 4%. You are considering adding a precious metals fund to your current portfolio. The metals fund has an expected return of 10%, a volatility of 30%, and a correlation of-20 with the Luther Fund. Will...

(15) You have invested only in the BlueChip Fund, a mutual fund that invests mainly in stocks. At the moment, the BlueChip Fund has a volatility of 32%. Your broker suggests that you add the GoldAll Fund to your current portfolio. The GoldAll Fund has a volatility of 35% and a correlation of -0.10 with the BlueChip Fund. Risk-free interest rate is equal to 5%. The required return on the GoldAll Fund is closest to: Volatility Comelation ВСЕ 3 .....

(15) You have invested only in the BlueChip Fund, a mutual fund that invests mainly in stocks. At the moment, the BlueChip Fund has a volatility of 32%. Your broker suggests that you add the GoldAll Fund to your current portfolio. The GoldAll Fund has a volatility of 35% and a correlation of -0.10 with the BlueChip Fund. Risk-free interest rate is equal to 5%. The required return on the GoldAll Fund is closest to: Volatility Comelation ВСЕ 3 .....

please help with step no excel :)

5) You have invested only in the BlueChip Fund, a mutual fund that invests mainly in stocks. At the moment, the Blue Chip Fund has a volatility of 32%. Your broker suggests that you add the GoldAll Fund to your current portfolio. The GoldAll Fund has a volatility of 35% and a correlation of -0.10 with the BlueChip Fund. Risk-free interest rate is equal to 5%. The required return on the GoldAll Fund...

please help with step no excel :)

5) You have invested only in the BlueChip Fund, a mutual fund that invests mainly in stocks. At the moment, the Blue Chip Fund has a volatility of 32%. Your broker suggests that you add the GoldAll Fund to your current portfolio. The GoldAll Fund has a volatility of 35% and a correlation of -0.10 with the BlueChip Fund. Risk-free interest rate is equal to 5%. The required return on the GoldAll Fund...

Most questions answered within 3 hours.

-

Phosphorous + bromine = phosphorous tribromide. If 35.0 g of

bromine are reacted and 27.9 grams...

asked 54 minutes ago -

Derive the long wavelength limit of the Planck energy density

distribution

asked 44 minutes ago -

Calculate the pH of each of the following solutions.

0.50 M HBr

3.1×10−4 M KOH

4.2×10−5...

asked 4 hours ago -

For the year ended December 31, Depot Max’s cost of merchandise

sold was $85,600. Inventory at the...

asked 4 hours ago -

Week 10 - Professional Memo Assignment

Professional Memo Assignment

Your mission for this week, should you...

asked 4 hours ago -

Write a Python program that stores the data for each

player on the team, and it...

asked 4 hours ago -

In

the last 3 months, mike never knows when he is going to get his

allowance...

asked 5 hours ago -

Is Ca(OH)2 a Bronsted base, Lewis base, or both? Why?

asked 4 hours ago -

1A- Why don’t voters complain about U.S. tariffs on imported

sugar?

Because sugar is only a...

asked 5 hours ago -

Cash Payback Period

Primera Banco is evaluating two capital investment proposals for

a drive-up ATM kiosk,...

asked 4 hours ago -

Create a button in Swift (Xcode) that will create a charge,

create a charge using Stripe's...

asked 4 hours ago -

The reaction rate of CO and NO2 in the reaction

CO(g) + NO2(g) → CO2(g) +...

asked 4 hours ago