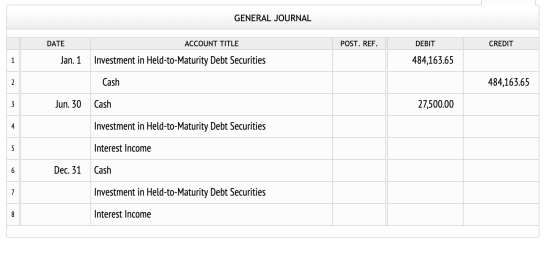

On January 1, 2019, Kelly Corporation acquired bonds with a face value of $500,000 for $484,163.65, a price that yields a 11% effective annual interest rate. The bonds carry a 10% stated rate of interest, pay interest semiannually on June 30 and December 31, are due December 31, 2022, and are being held to maturity.

Required:

| Prepare journal entries to record the purchase of the bonds and the first two interest receipts using the: |

| 1. | straight-line method of amortization |

| 2. |

effective interest method of amortization |

1.

2.

Homework Answers

| Rate | Semi annual Market Interest=(11/2)% | 5.50% | |||||||||

| Nper | Number of Semi annual period | 8 | (4*2) | ||||||||

| Pmt | Semi annual Coupon Payment ($500000*10%)/2 | $25,000 | |||||||||

| FV | Payment at maturity | $500,000 | |||||||||

| PV | Bond Issue Price | $484,163.65 | (Using PV function of excel with Rate=4%, Nper=10, Pmt=-500, Fv=-10000) | ||||||||

| FV-PV | Bond Discount (500000-484164) | $15,836.35 | |||||||||

| Semi-Annual Amortization of discount (Straight Line Method | $1,979.54 | (15836.35/8) | |||||||||

| AMORTIZATION SCHEDULE(STRAIGHT LINE METHOD) | |||||||||||

| (10/2)=5% *500000 | Market rate(11/2)=5.5% *Previous Book value | ||||||||||

| A | B | C=D+B | D | E | F | G=F-E | |||||

| Date | Cash Received | Interest Income | Amortization of Discount | Credit Balance in Bond Discount Account | Debit Balance in Debt SecurityAccount | Book value of the Bond | |||||

| Jan1,2019 | $15,836.35 | $500,000 | $484,163.65 | ||||||||

| June30,2019 | $25,000 | $26,979.54 | $1,979.54 | $13,856.81 | $500,000 | $486,143.19 | |||||

| Dec31,2019 | $25,000 | $26,979.54 | $1,979.54 | $11,877.26 | $500,000 | $488,122.74 | |||||

| JOURNAL ENTRY (STRAIGHT LINE METHOD) | |||||||||||

| DATE | ACCOUNT TITLES | DEBIT | CREDIT | ||||||||

| Jan,1,2019 | Held to Maturity Debt Security | $500,000 | |||||||||

| Bond Discount | $15,836.35 | ||||||||||

| Cash | $484,163.65 | ||||||||||

| June,30,2019 | Cash | $25,000.00 | |||||||||

| Bond Discount | $1,979.54 | ||||||||||

| Interest Income | $26,979.54 | ||||||||||

| Dec,31,2019 | Cash | $25,000.00 | |||||||||

| Bond Discount | $1,979.54 | ||||||||||

| Interest Income | $26,979.54 | ||||||||||

| AMORTIZATION SCHEDULE(EFFECTIVE INTEREST) | |||||||||||

| (10/2)=5% *500000 | Market rate(11/2)=5.5% *Previous Book value | ||||||||||

| A | B | C | D=C-B | E | F | G=F-E | |||||

| Date | Cash | Interest Income | Amortization of Discount | Credit Balance in Bond Discount Account | Debit Balance in Debt Security Account | Book value of the Bond | |||||

| Jan1,2019 | $15,836.35 | $500,000 | $484,163.65 | ||||||||

| June30,2019 | $25,000 | $26,629.00 | $1,629.00 | $14,207.35 | $500,000 | $485,792.65 | |||||

| Dec31,2019 | $25,000 | $26,718.60 | $1,718.60 | $12,488.75 | $500,000 | $487,511.25 | |||||

| JOURNAL ENTRY (EFFECTIVE INTEREST METHOD) | |||||||||||

| ACCOUNT TITLES | DEBIT | CREDIT | |||||||||

| Jan,1,2019 | Held to Maturity Debt Security | $500,000 | |||||||||

| Bond Discount | $15,836.35 | ||||||||||

| Cash | $484,163.65 | ||||||||||

| June,30,2019 | Cash | $25,000.00 | |||||||||

| Bond Discount | $1,629.00 | ||||||||||

| Interest Income | $26,629.00 | ||||||||||

| Dec,31,2019 | Cash | $25,000.00 | |||||||||

| Bond Discount | $1,718.60 | ||||||||||

| Interest Income | $26,718.60 | ||||||||||

Add Answer to:

On January 1, 2019, Kelly Corporation acquired bonds with a face

value of $500,000 for $484,163.65,...

On January 1, 2019, Kelly Corporation acquired bonds with a face value of $500,000 for $484,163.65,...

On January 1, 2019, Kelly Corporation acquired bonds with a face

value of $500,000 for $484,163.65, a price that yields a 11%

effective annual interest rate. The bonds carry a 10% stated rate

of interest, pay interest semiannually on June 30 and December 31,

are due December 31, 2022, and are being held to maturity.

Required:

Prepare journal entries to record the purchase of the bonds and

the first two interest receipts using the:

1.

straight-line method of amortization

2....

On January 1, 2019, Kelly Corporation acquired bonds with a face

value of $500,000 for $484,163.65, a price that yields a 11%

effective annual interest rate. The bonds carry a 10% stated rate

of interest, pay interest semiannually on June 30 and December 31,

are due December 31, 2022, and are being held to maturity.

Required:

Prepare journal entries to record the purchase of the bonds and

the first two interest receipts using the:

1.

straight-line method of amortization

2....

On January 1, 2018, Kelly Corporation acquired bonds with a face value of $400,000 for $387,330.92,...

On January 1, 2018, Kelly Corporation acquired bonds with a face value of $400,000 for $387,330.92, a price that yields a 11% effective annual interest rate. The bonds carry a 10% stated rate of interest, pay interest semiannually on June 30 and December 31, are due December 31, 2021, and are being held to maturity. Required: Prepare journal entries to record the purchase of the bonds and the first two interest receipts using the: 1. straight-line method of amortization 2....

On March 31, 2019, Brodie Corporation acquired bonds with a par value of $600,000 for $628,800....

On March 31, 2019, Brodie Corporation acquired bonds with a par value of $600,000 for $628,800. The bonds are due December 31, 2024, carry a 10% annual interest rate, pay interest on June 30 and December 31, and are being held to maturity. The accrued interest is included in the acquisition price of the bonds. Brodie uses straight-line amortization. Required: 1. Prepare journal entries for Brodie to record the purchase of the bonds and the first two interest receipts. 2....

On November 1, 2017, Reid Corporation acquired bonds with a face value of $500,000 for $481,156.15....

On November 1, 2017, Reid Corporation acquired bonds with a face value of $500,000 for $481,156.15. The bonds carry a stated rate of interest of 10%, were purchased to yield 11%, pay interest semiannually on April 30 and October 31, were purchased to be held to maturity, and are due October 31, 2021. On November 1, 2018, in contemplation of a major acquisition, the bonds were sold for $500,000. Reid is on a fiscal year accounting period ending October 31...

On March 31, 2018, Brodie Corporation acquired bonds with a par value of $300,000 for $313,650....

On March 31, 2018, Brodie Corporation acquired bonds with a par value of $300,000 for $313,650. The bonds are due December 31, 2023, carry a 9% annual interest rate, pay interest on June 30 and December 31, and are being held to maturity. The accrued interest is included in the acquisition price of the bonds. Brodie uses straight-line amortization. Required: 1. Prepare journal entries for Brodie to record the purchase of the bonds and the first two interest receipts. 2....

Glover Corporation purchased bonds with a face value of $300,000 for $307,493.34 on January 1, 2018....

Glover Corporation purchased bonds with a face value of $300,000 for $307,493.34 on January 1, 2018. The bonds carry a face rate of interest of 12%, pay interest semiannually on June 30 and December 31, were purchased to be held to maturity, are due December 31, 2020, and were purchased to yield 11%. On January 1, 2019, in contemplation of a major acquisition, the bonds were sold for $300,000. Glover uses the effective interest method. Required: 1. Prepare journal entries...

(#6) Held-to-Maturity Bond Investment On January 1, 2018, Gatrong Corporation purchased 13%, 5-year Fleming Corporation bonds...

(#6) Held-to-Maturity Bond Investment On January 1, 2018, Gatrong Corporation purchased 13%, 5-year Fleming Corporation bonds with a face value of $200,000. It expects to hold these bonds until maturity. The bonds pay interest semiannually on June 30 and December 31. Gatrong paid $215,075, a price that yields a 11% effective annual interest rate. Required: Prepare the journal entry of Gatrong to record the purchase of the bonds. CHART OF ACCOUNTS Gatrong Corporation General Ledger ASSETS 111 Cash 121 Accounts...

Held-to-Maturity Securities and Amortization of a Discount On January 1, 2019, Kelly Corporation acquired bonds with...

Held-to-Maturity Securities and Amortization of a Discount On January 1, 2019, Kelly Corporation acquired bonds with a face value of $500,000 for $483,841.79, a price that yields a 10% effective annual interest rate. The bonds carry a 9% stated rate of interest, pay interest semiannually on June 30 and December 31, are due December 31, 2022, and are being held to maturity. Required: Prepare journal entries to record the purchase of the bonds and the first two interest receipts using...

On January 1, 2012, Ithaca Corp. purchases Cortland Inc. bonds that have a face value of...

On January 1, 2012, Ithaca Corp. purchases Cortland Inc. bonds that have a face value of $150,000. The Cortland bonds have a stated interest rate of 6%. Interest is paid semiannually on June 30 and December 31, and the bonds mature in 10 years. For bonds of similar risk and maturity, the market yield on particular dates is as follows January 1,2012 June 30, 2012 December 31 , 2012 7.0% 80% 90% Use PV of $1 and PVA of $1...

On January 1, 2012, Ithaca Corp. purchases Cortland Inc. bonds that have a face value of $150,000. The Cortland bonds have a stated interest rate of 6%. Interest is paid semiannually on June 30 and December 31, and the bonds mature in 10 years. For bonds of similar risk and maturity, the market yield on particular dates is as follows January 1,2012 June 30, 2012 December 31 , 2012 7.0% 80% 90% Use PV of $1 and PVA of $1...

(#7) Held-to-Maturity Bond Investment On January 1, 2018, Gatrong Corporation purchased 13%, 5-year Fleming Corporation bonds...

(#7) Held-to-Maturity Bond Investment On January 1, 2018, Gatrong Corporation purchased 13%, 5-year Fleming Corporation bonds with a face value of $100,000. It expects to hold these bonds until maturity. The bonds pay interest semiannually on June 30 and December 31. Gatrong paid $111,583, a price that yields a 10% effective annual interest rate. Required: Prepare the journal entry on June 30 for Gatrong to record the first interest receipt, using the effective interest method. CHART OF ACCOUNTS Gatrong Corporation...

On January 1, 2019, Kelly Corporation acquired bonds with a face

value of $500,000 for $484,163.65, a price that yields a 11%

effective annual interest rate. The bonds carry a 10% stated rate

of interest, pay interest semiannually on June 30 and December 31,

are due December 31, 2022, and are being held to maturity.

Required:

Prepare journal entries to record the purchase of the bonds and

the first two interest receipts using the:

1.

straight-line method of amortization

2....

On January 1, 2019, Kelly Corporation acquired bonds with a face

value of $500,000 for $484,163.65, a price that yields a 11%

effective annual interest rate. The bonds carry a 10% stated rate

of interest, pay interest semiannually on June 30 and December 31,

are due December 31, 2022, and are being held to maturity.

Required:

Prepare journal entries to record the purchase of the bonds and

the first two interest receipts using the:

1.

straight-line method of amortization

2....

On January 1, 2012, Ithaca Corp. purchases Cortland Inc. bonds that have a face value of $150,000. The Cortland bonds have a stated interest rate of 6%. Interest is paid semiannually on June 30 and December 31, and the bonds mature in 10 years. For bonds of similar risk and maturity, the market yield on particular dates is as follows January 1,2012 June 30, 2012 December 31 , 2012 7.0% 80% 90% Use PV of $1 and PVA of $1...

On January 1, 2012, Ithaca Corp. purchases Cortland Inc. bonds that have a face value of $150,000. The Cortland bonds have a stated interest rate of 6%. Interest is paid semiannually on June 30 and December 31, and the bonds mature in 10 years. For bonds of similar risk and maturity, the market yield on particular dates is as follows January 1,2012 June 30, 2012 December 31 , 2012 7.0% 80% 90% Use PV of $1 and PVA of $1...

Most questions answered within 3 hours.

-

Linear programming is an excellent technique yet is not applied

nearly enough in the “real world.”...

asked 8 minutes ago -

What three alkenes yield 3-methylpentane on catalytic

hydrogenation?

asked 8 minutes ago -

In JAVA Create a program with an array with the following

data:

50 12 31 76...

asked 10 minutes ago -

Using a hormone of the hypothalamic-anterior pituitary axis,

describe or diagram how negative feedback loops regulate...

asked 8 minutes ago -

1,1-dimethylcyclorohexane reacts with single bromine atom

asked 31 minutes ago -

The completed Lewis structure of CO2 contains a total

of 0,1,2,3,4,5,6,7,8 covalent bonds

and 0,1,2,3,4,5,6,7,8 lone pairs.

NOTE:...

asked 38 minutes ago -

A 0.0510 M solution of an organic acid has an

[H+] of 7.50×10-4M .

What is...

asked 35 minutes ago -

what is the profit-maximizing output condition that a

monopolistically competitive firm must satisfy? a) price charged...

asked 39 minutes ago -

Consider the set of ordered pairs shown below. Assuming that the

regression equation is y=3.513+0.429x and...

asked 1 hour ago -

1. (A) Write two

structural (constitutional)

isomers of C4H8F2?

Please show all of

the

asked 1 hour ago -

Objective: Practice converting a Boolean logic

expression into it’s truth table and to show the implementation...

asked 1 hour ago -

1) Name the three holes located in the greater wing of the

sphenoid bone in order...

asked 1 hour ago