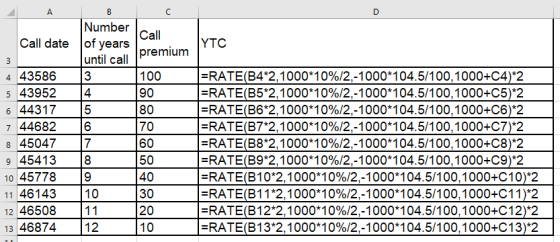

A company has the following bond outstanding. The bond is callable every year on May 1st,...

A company has the following bond outstanding. The bond is callable every year on May 1st, the anniversary date of the bond. The bond has a deferred call with three years left. The call premium on the first call date is one year's interest. The call premium will decline by 10 percent of the original call premium for 10 years. Eleven years from today, the call premium will be zero. Given the following information, what is the yield to worst for this bond?

|

Current date: |

5/1/2016 |

|

|

Maturity date: |

5/1/2036 |

|

|

Price (percent of par): |

104.5 |

|

|

Coupon rate: |

10.00% |

|

|

Par value (percent of par): |

100 |

|

|

Coupons per year: |

2 |

|

|

Call date |

Call premium |

|

|

5/1/2019 |

$ 100.00 |

|

|

5/1/2020 |

$ 90.00 |

|

|

5/1/2021 |

$ 80.00 |

|

|

5/1/2022 |

$ 70.00 |

|

|

5/1/2023 |

$ 60.00 |

|

|

5/1/2024 |

$ 50.00 |

|

|

5/1/2025 |

$ 40.00 |

|

|

5/1/2026 |

$ 30.00 |

|

|

5/1/2027 |

$ 20.00 |

|

|

5/1/2028 |

$ 10.00 |

|

Homework Answers

Yield to worst is the lower of yield to call (YTC) and yield to maturity (YTM).

YTM is calculated using RATE function in Excel with these inputs :

nper = 20*2 (20 years to maturity with 2 semiannual coupon payments each year)

pmt = 1000 * 10% / 2 (semiannual coupon payment = face value * annual coupon rate / 2. This is a positive figure as it is an inflow to the bondholder)

pv = -1000 * 104.5 / 100 (current bond price = face value * price as percent of par / 100. This is a negative figure as it is an outflow to the buyer of the bond)

fv = 1000 (face value of the bond receivable on maturity. This is a positive figure as it is an inflow to the bondholder)

The RATE is calculated to be 4.75%. This is the semiannual YTM. To calculate the annual YTM, we multiply by 2. Annual YTM is 9.49%

YTC for each call date is calculated using RATE function in Excel with these inputs :

nper = __* 2 (__ years to call date with 2 semiannual coupon payments each year)

pmt = 1000 * 10% / 2 (annual coupon payment = face value * annual coupon rate. This is a positive figure as it is an inflow to the bondholder)

pv = -1000 * 104.5 / 100 (current bond price = face value * price as percent of par / 100. This is a negative figure as it is an outflow to the buyer of the bond)

fv = 1000 + __ (call price of the bond receivable on call date = face value + call premium. This is a positive figure as it is an inflow to the bondholder)

The RATE is calculated to be __%. This is the semiannual YTC. To calculate the annual YTC, we multiply by 2. Annual YTC is __%

![Α Number of Call Call date years until premium call 5/1/2019 $100 11.10%l 5/1/2020 $90] 10.46% 5/1/2021) $80] 10.10% 5/1/2022](http://img.homeworklib.com/questions/aeb427c0-7939-11ea-ba3b-e3fc09ccfc12.png?x-oss-process=image/resize,w_560)

The lowest YTC is 9.41%.

The YTM is 9.49%.

Yield to worst is the lower of yield to call (YTC) and yield to maturity (YTM).

The yield to worst is 9.41%

Add Answer to:

A company has the following bond outstanding. The bond is

callable every year on May 1st,...

Chapter 6 - Master it! In an earlier worksheet we discussed the difference between yield to...

Chapter 6 - Master it! In an earlier worksheet we discussed the difference between yield to maturity and yield to call. There is another yield that is commonly quoted, the yield to worst. The yield to worst is the lowest potential yield that can be received on a bond without the issuer actually defaulting. Yield to worst is calculated on all possible call dates. It is assumed that prepayment occurs if the bond has a call provision. The yield to...

Chapter 6 - Master it! In an earlier worksheet we discussed the difference between yield to maturity and yield to call. There is another yield that is commonly quoted, the yield to worst. The yield to worst is the lowest potential yield that can be received on a bond without the issuer actually defaulting. Yield to worst is calculated on all possible call dates. It is assumed that prepayment occurs if the bond has a call provision. The yield to...

Fooling Company has a callable bond outstanding with a coupon of 11.4 percent, 25 years to...

Fooling Company has a callable bond outstanding with a coupon of 11.4 percent, 25 years to maturity, call protection for the next 10 years, and a call premium of $25. What is the yield to call (YTC) for this bond if the current price is 103 percent of par value? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) eBook Yield to call Dit References

Fooling Company has a callable bond outstanding with a coupon of 11.4 percent, 25 years to maturity, call protection for the next 10 years, and a call premium of $25. What is the yield to call (YTC) for this bond if the current price is 103 percent of par value? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) eBook Yield to call Dit References

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 12% and $1,000 par value. The issuer, however, can call the bond starting at the end of 10 years. If the yield to call on this bond is 5% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Callable bond. Corso Books has just sold a callable bond ... . It is a thirty-year...

Callable bond. Corso Books has just sold a callable bond ... . It is a thirty-year monthly bond with an annual coupon rate 12% and $1,000 par value. The issuer, however, can call the bond starting at the end of 12 years. If the yield to call on this bond is 9% and the call requires Corso Books to pay one year of additional interest at the call (12 coupon payments), what is the bond price if priced with the...

Problem 10-22 Yield to Call (LO1, CFA3) Fooling Company has a callable bond outstanding with a coupon of 11.8 percent,...

Problem 10-22 Yield to Call (LO1, CFA3) Fooling Company has a callable bond outstanding with a coupon of 11.8 percent, 25 years to maturity, call protection for the next 10 years, and a call premium of $50. What is the yield to call (YTC) for this bond if the current price is 108 percent of par value? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) Yield to call

Problem 10-22 Yield to Call (LO1, CFA3) Fooling Company has a callable bond outstanding with a coupon of 11.8 percent, 25 years to maturity, call protection for the next 10 years, and a call premium of $50. What is the yield to call (YTC) for this bond if the current price is 108 percent of par value? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) Yield to call

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 9% and $5,000 par value. The issuer, however, can call the bond starting at the end of 6 years. If the yield to call on this bond is 10% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 9% and $5,000 par value. The issuer, however, can call the bond starting at the end of 6 years. If the yield to call on this bond is 10% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 7% and $5,000 par value. The issuer, however, can call the bond starting at the end of 8 years. If the yield to call on this bond is 9% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 7% and $5,000 par value. The issuer, however, can call the bond starting at the end of 8 years. If the yield to call on this bond is 9% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rat...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 9% and $5,000 par value. The issuer, however, can call the bond starting at the end of 12 years. If the yield to call on this bond is 6% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 9% and $5,000 par value. The issuer, however, can call the bond starting at the end of 12 years. If the yield to call on this bond is 6% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Fin 445 ABC Inc. has two callable bonds outstanding on the market, both with 12 years...

Fin 445 ABC Inc. has two callable bonds outstanding on the market, both with 12 years to maturity, call protection for the next 5 years, and a call premium of $100. Bond A has a 9% coupon and is priced at 117% of par. Bond B has a 5% coupon and is priced at 74.60% of par. What is the market yield for these two bonds? 1.

Fin 445 ABC Inc. has two callable bonds outstanding on the market, both with 12 years to maturity, call protection for the next 5 years, and a call premium of $100. Bond A has a 9% coupon and is priced at 117% of par. Bond B has a 5% coupon and is priced at 74.60% of par. What is the market yield for these two bonds? 1.

.. 4 Unanswered A callable bond has 10 years to maturity and 2 years to call....

.. 4 Unanswered A callable bond has 10 years to maturity and 2 years to call. The bond is callable at 105% of par and has a coupon rate of 5%. If the bond is currently priced at $1100, what is the yield to call %? (Convert to a percent, but include only numbers in your response.) Type your response

.. 4 Unanswered A callable bond has 10 years to maturity and 2 years to call. The bond is callable at 105% of par and has a coupon rate of 5%. If the bond is currently priced at $1100, what is the yield to call %? (Convert to a percent, but include only numbers in your response.) Type your response

Chapter 6 - Master it! In an earlier worksheet we discussed the difference between yield to maturity and yield to call. There is another yield that is commonly quoted, the yield to worst. The yield to worst is the lowest potential yield that can be received on a bond without the issuer actually defaulting. Yield to worst is calculated on all possible call dates. It is assumed that prepayment occurs if the bond has a call provision. The yield to...

Chapter 6 - Master it! In an earlier worksheet we discussed the difference between yield to maturity and yield to call. There is another yield that is commonly quoted, the yield to worst. The yield to worst is the lowest potential yield that can be received on a bond without the issuer actually defaulting. Yield to worst is calculated on all possible call dates. It is assumed that prepayment occurs if the bond has a call provision. The yield to...

Fooling Company has a callable bond outstanding with a coupon of 11.4 percent, 25 years to maturity, call protection for the next 10 years, and a call premium of $25. What is the yield to call (YTC) for this bond if the current price is 103 percent of par value? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) eBook Yield to call Dit References

Fooling Company has a callable bond outstanding with a coupon of 11.4 percent, 25 years to maturity, call protection for the next 10 years, and a call premium of $25. What is the yield to call (YTC) for this bond if the current price is 103 percent of par value? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) eBook Yield to call Dit References

Problem 10-22 Yield to Call (LO1, CFA3) Fooling Company has a callable bond outstanding with a coupon of 11.8 percent, 25 years to maturity, call protection for the next 10 years, and a call premium of $50. What is the yield to call (YTC) for this bond if the current price is 108 percent of par value? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) Yield to call

Problem 10-22 Yield to Call (LO1, CFA3) Fooling Company has a callable bond outstanding with a coupon of 11.8 percent, 25 years to maturity, call protection for the next 10 years, and a call premium of $50. What is the yield to call (YTC) for this bond if the current price is 108 percent of par value? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) Yield to call

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 9% and $5,000 par value. The issuer, however, can call the bond starting at the end of 6 years. If the yield to call on this bond is 10% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 9% and $5,000 par value. The issuer, however, can call the bond starting at the end of 6 years. If the yield to call on this bond is 10% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 7% and $5,000 par value. The issuer, however, can call the bond starting at the end of 8 years. If the yield to call on this bond is 9% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 7% and $5,000 par value. The issuer, however, can call the bond starting at the end of 8 years. If the yield to call on this bond is 9% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 9% and $5,000 par value. The issuer, however, can call the bond starting at the end of 12 years. If the yield to call on this bond is 6% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Callable bond. Corso Books has just sold a callable bond. It is a thirty-year semiannual bond with an annual coupon rate of 9% and $5,000 par value. The issuer, however, can call the bond starting at the end of 12 years. If the yield to call on this bond is 6% and the call requires Corso Books to pay one year of additional interest at the call (2 coupon payments), what is the bond price if priced with the assumption...

Fin 445 ABC Inc. has two callable bonds outstanding on the market, both with 12 years to maturity, call protection for the next 5 years, and a call premium of $100. Bond A has a 9% coupon and is priced at 117% of par. Bond B has a 5% coupon and is priced at 74.60% of par. What is the market yield for these two bonds? 1.

Fin 445 ABC Inc. has two callable bonds outstanding on the market, both with 12 years to maturity, call protection for the next 5 years, and a call premium of $100. Bond A has a 9% coupon and is priced at 117% of par. Bond B has a 5% coupon and is priced at 74.60% of par. What is the market yield for these two bonds? 1.

.. 4 Unanswered A callable bond has 10 years to maturity and 2 years to call. The bond is callable at 105% of par and has a coupon rate of 5%. If the bond is currently priced at $1100, what is the yield to call %? (Convert to a percent, but include only numbers in your response.) Type your response

.. 4 Unanswered A callable bond has 10 years to maturity and 2 years to call. The bond is callable at 105% of par and has a coupon rate of 5%. If the bond is currently priced at $1100, what is the yield to call %? (Convert to a percent, but include only numbers in your response.) Type your response

Most questions answered within 3 hours.

-

4CO(g) + 8H2(g) -----> 3CH4(g) +

CO2(g) + 2H2O(l)

Use the following data as needed to...

asked 2 minutes ago -

without using map

1. Write a C++ program to find out the top 10 words in...

asked 16 minutes ago -

1)Calculate the percent ionization of a

0.330 M solution of hypochlorous

acid.

% Ionization = %...

asked 18 minutes ago -

1a) How many grams of K2SO4 are in 250mL

of 0.11 M K2SO4 solution?

_____ g...

asked 9 minutes ago -

The vapor pressure of a solution containing 38.7 g glycerin

(C3H8O3) in 146.2 g ethanol (C2H5OH)...

asked 14 minutes ago -

A physics major is cooking breakfast when he notices that the

frictional force between the steel...

asked 20 minutes ago -

A cyclohexane (c-hex) solution is prepared by fully dissolving

9.11g of a newly synthesized organic compound...

asked 26 minutes ago -

SCHEME :-)

[5 marks] Write a procedure called convert that takes as

arguments: a temperature value...

asked 32 minutes ago -

Are

Acetyl CoA and Pyruvate biological molecules that are used to get

ATP energy in aerobic...

asked 33 minutes ago -

Two waves are traveling on a string, one with a wave function,

y1 = 0.05sin(4x -...

asked 40 minutes ago -

Develop an ideal customer profile for three Dell Customer

groups( a supplier, a global business, and...

asked 43 minutes ago -

Suppose, for any future year, the probability its October rain

is more than 3 inches is...

asked 47 minutes ago