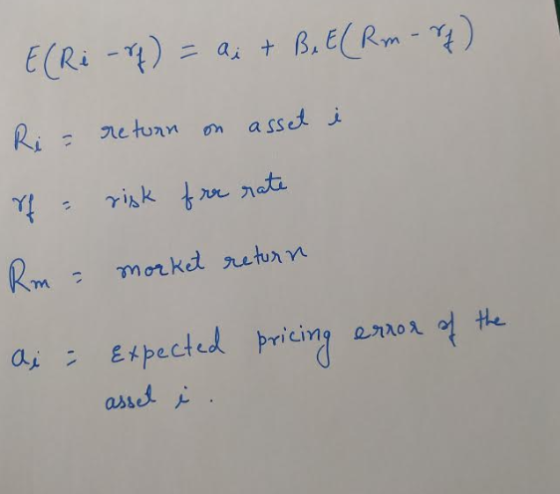

What is the formula for CAPM pricing error?

What is the formula for CAPM pricing error?

Homework Answers

What are the most important assumptions of the Capital Asset Pricing Model (CAPM)? Explain with examples.

What are the most important assumptions of the Capital Asset Pricing Model (CAPM)? Explain with examples.

What are the most important assumptions of the Capital Asset Pricing Model (CAPM)? Explain with examples.

What are the most important assumptions of the Capital Asset Pricing Model (CAPM)? Explain with examples.

In at least 200 words, what is Capital Asset Pricing Model (CAPM), how and why is...

In at least 200 words, what is Capital Asset Pricing Model (CAPM), how and why is it used. and why is it important?

Capital Asset Pricing Model (CAPM) a. What is two-fund portfolio separation and why is it important?...

Capital Asset Pricing Model (CAPM) a. What is two-fund portfolio separation and why is it important? b. Show graphically (in return-standard deviation space) how 2-fund separation works in the context of the CAPM. c. Explain and show how risk averse investors are better off with capital markets. d. What are some of the assumptions that need to hold in order for the CAPM to be applied and why are they important? e. Suppose a stock has a covariance with the...

Capital Asset Pricing Model (CAPM) a. What is two-fund portfolio separation and why is it important? b. Show graphically (in return-standard deviation space) how 2-fund separation works in the context of the CAPM. c. Explain and show how risk averse investors are better off with capital markets. d. What are some of the assumptions that need to hold in order for the CAPM to be applied and why are they important? e. Suppose a stock has a covariance with the...

What is CAPM (Capital Assets Pricing Model) and how do companies make financial decisions based on...

What is CAPM (Capital Assets Pricing Model) and how do companies make financial decisions based on it?

Which of the following are assumptions of the Capital Asset Pricing Model (CAPM)? Check all that...

Which of the following are assumptions of the Capital Asset Pricing Model (CAPM)? Check all that apply. O Asset quantities are given and fixed. There are no transaction costs. Taxes are accounted for. All investors focus on a single holding period. O Consider the equation for the Capital Asset Pricing Model (CAPM): Cov(ri, rm) ři = rre + Cím – PRF) x In this equation, the term Cov(ri, rm) / om represents the Suppose that the market's average excess return...

Which of the following are assumptions of the Capital Asset Pricing Model (CAPM)? Check all that apply. O Asset quantities are given and fixed. There are no transaction costs. Taxes are accounted for. All investors focus on a single holding period. O Consider the equation for the Capital Asset Pricing Model (CAPM): Cov(ri, rm) ři = rre + Cím – PRF) x In this equation, the term Cov(ri, rm) / om represents the Suppose that the market's average excess return...

thanks Describe the Dividend Growth Rate model and the Capital Asset Pricing Model (CAPM) as it...

thanks

Describe the Dividend Growth Rate model and the Capital Asset Pricing Model (CAPM) as it 3) relates to Common Stock Pricing. What are the advantages and disadvantages of Both? (15 points) Y

thanks

Describe the Dividend Growth Rate model and the Capital Asset Pricing Model (CAPM) as it 3) relates to Common Stock Pricing. What are the advantages and disadvantages of Both? (15 points) Y

For AT&T Inc. 2018. Apply the Capital Asset Pricing Model (CAPM) Security Market Line to estimate...

For AT&T Inc. 2018. Apply the Capital Asset Pricing Model (CAPM) Security Market Line to estimate the required return on THE COMPANY stock. Expected Rate of Return = Risk-Free Rate + Beta(Market Return – Risk Free Rate) Use 7.5% for an average expected market rate of return Use 3% as an average risk-free rate (10 year composite rate of T-bill) Find the beta of your company’s stock with other financial data on Yahoo Finance or MarketWatch....

5. Capital Asset Pricing Model (CAPM) a. Explain why it is important to assume that investor's...

5. Capital Asset Pricing Model (CAPM) a. Explain why it is important to assume that investor's already hold the value-weighted "market", or tangency, portfolio in order to apply the Capital Asset Pricing Model (CAPM). b. Does the risk-free asset need to exist in order for us to derive the CAPM? If not, how do investors achieve 2-fund separation? (Hint: Your textbook can help with this.)

5. Capital Asset Pricing Model (CAPM) a. Explain why it is important to assume that investor's already hold the value-weighted "market", or tangency, portfolio in order to apply the Capital Asset Pricing Model (CAPM). b. Does the risk-free asset need to exist in order for us to derive the CAPM? If not, how do investors achieve 2-fund separation? (Hint: Your textbook can help with this.)

According to the capital asset pricing (CAPM) model, what return should you require for a security...

According to the capital asset pricing (CAPM) model, what return should you require for a security with a beta of 1.2, if the risk-free rate is 2.4% and the market return is 12.3%? (Enter your answer as a percentage. For example, enter 8.43% instead of 0.0843.)

According to the capital asset pricing (CAPM) model, what return should you require for a security with a beta of 1.2, if the risk-free rate is 2.4% and the market return is 12.3%? (Enter your answer as a percentage. For example, enter 8.43% instead of 0.0843.)

Capital Asset Pricing Model (CAPM) a. What is two-fund portfolio separation and why is it important? b. Show graphically (in return-standard deviation space) how 2-fund separation works in the context of the CAPM. c. Explain and show how risk averse investors are better off with capital markets. d. What are some of the assumptions that need to hold in order for the CAPM to be applied and why are they important? e. Suppose a stock has a covariance with the...

Capital Asset Pricing Model (CAPM) a. What is two-fund portfolio separation and why is it important? b. Show graphically (in return-standard deviation space) how 2-fund separation works in the context of the CAPM. c. Explain and show how risk averse investors are better off with capital markets. d. What are some of the assumptions that need to hold in order for the CAPM to be applied and why are they important? e. Suppose a stock has a covariance with the...

Which of the following are assumptions of the Capital Asset Pricing Model (CAPM)? Check all that apply. O Asset quantities are given and fixed. There are no transaction costs. Taxes are accounted for. All investors focus on a single holding period. O Consider the equation for the Capital Asset Pricing Model (CAPM): Cov(ri, rm) ři = rre + Cím – PRF) x In this equation, the term Cov(ri, rm) / om represents the Suppose that the market's average excess return...

Which of the following are assumptions of the Capital Asset Pricing Model (CAPM)? Check all that apply. O Asset quantities are given and fixed. There are no transaction costs. Taxes are accounted for. All investors focus on a single holding period. O Consider the equation for the Capital Asset Pricing Model (CAPM): Cov(ri, rm) ři = rre + Cím – PRF) x In this equation, the term Cov(ri, rm) / om represents the Suppose that the market's average excess return...

thanks

Describe the Dividend Growth Rate model and the Capital Asset Pricing Model (CAPM) as it 3) relates to Common Stock Pricing. What are the advantages and disadvantages of Both? (15 points) Y

thanks

Describe the Dividend Growth Rate model and the Capital Asset Pricing Model (CAPM) as it 3) relates to Common Stock Pricing. What are the advantages and disadvantages of Both? (15 points) Y

5. Capital Asset Pricing Model (CAPM) a. Explain why it is important to assume that investor's already hold the value-weighted "market", or tangency, portfolio in order to apply the Capital Asset Pricing Model (CAPM). b. Does the risk-free asset need to exist in order for us to derive the CAPM? If not, how do investors achieve 2-fund separation? (Hint: Your textbook can help with this.)

5. Capital Asset Pricing Model (CAPM) a. Explain why it is important to assume that investor's already hold the value-weighted "market", or tangency, portfolio in order to apply the Capital Asset Pricing Model (CAPM). b. Does the risk-free asset need to exist in order for us to derive the CAPM? If not, how do investors achieve 2-fund separation? (Hint: Your textbook can help with this.)

According to the capital asset pricing (CAPM) model, what return should you require for a security with a beta of 1.2, if the risk-free rate is 2.4% and the market return is 12.3%? (Enter your answer as a percentage. For example, enter 8.43% instead of 0.0843.)

According to the capital asset pricing (CAPM) model, what return should you require for a security with a beta of 1.2, if the risk-free rate is 2.4% and the market return is 12.3%? (Enter your answer as a percentage. For example, enter 8.43% instead of 0.0843.)

Most questions answered within 3 hours.

-

A distribution center for a sporting goods retailer places

orders with manufacturers for a variety of...

asked 3 minutes ago -

Suppose you have a bag of Skittles with 27 blue Skittles, 18

green

Skittles, 32 red...

asked 5 minutes ago -

Sketch the circuit diagram for an inverting amplifier, and give

component values that will produce a...

asked 8 minutes ago -

Develop in C language the function whose prototype is described

below. Please, send the entire code,...

asked 26 minutes ago -

What single payment today would replace a payment stream of

$50,000 that will be paid today,...

asked 20 minutes ago -

please c++ with functions *Modify the Guessing Game Write the

secret number to a file. Then...

asked 20 minutes ago -

Question about ACID/BASE. Equal volumes of 0.230 M weak base (Kb

= 4.0× 10–9) and 0.230...

asked 25 minutes ago -

The charges and coordinates of two charged particles held fixed

in an xy plane are q1...

asked 28 minutes ago -

A particle of mass M = 7.5 kg is at a position r = (-3 i...

asked 27 minutes ago -

Please answer the question below with complete explanation and a

light rays drawing of the concave...

asked 30 minutes ago -

On January 4th, Stevens Manufacturing received an

order for 30 uniforms. The following information pertained to...

asked 39 minutes ago -

what is the present value of a 3 year growing annuity with the

first payment of...

asked 47 minutes ago