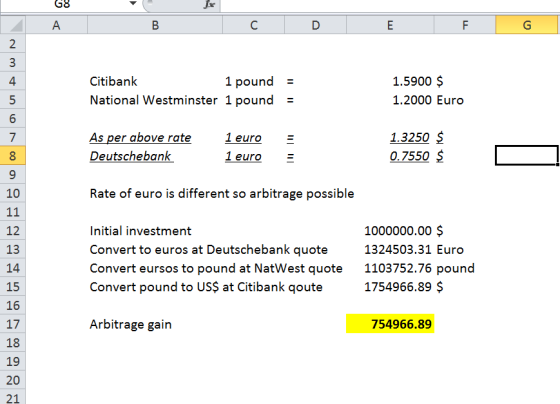

Assuming the following quotes, calculate how a market trader at Citibank with $1,000,000 can make an...

Assuming the following quotes, calculate how a market trader at Citibank with $1,000,000 can make an intermarket arbitrage profit. First establish if there is the possibility of arbitrage profit. Second show that path and amount of profit.

Citibank quotes U.S. dollar per pound: $1.5900/£

National Westminster quotes euros per pound: €1.2000/£

Deutschebank quotes U.S. dollar per euro: $0.7550/€

Homework Answers

Add Answer to:

Assuming the following quotes, calculate how a market trader at

Citibank with $1,000,000 can make an...

4. Triangular Arbitrage. Assume the following quotes: Citibank quotes U.S dollars per pound at $1.5400/£, National...

4. Triangular Arbitrage. Assume the following quotes: Citibank quotes U.S dollars per pound at $1.5400/£, National Westminster quotes euro per pound at €1.6000/£, Deutschebank quotes dollars per euro at $0.9700/€. Calculate how a market trader at Citibank with $1,000,000 can make inter-market arbitrage profit.

1. Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders if he can make an in...

1. Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders if he can make an intermarket arbitrage profit using Libyan dinars (LYD) and Saudi riyals (SAR). He has USD 1,000,000 to work with so he gathers the following quotes: Citibank quotes U.S. dollar per Libyan dinar $1.9619 = LYD 1.00 National Bank of Kuwait quotes Saudi riyal per Libyan dinar SAR 1.9107 = LYD 1.00 Barclays quotes U.S. dollar per Saudi riyal $0.2751 = SAR...

1. Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders if he can make an intermarket arbitrage profit using Libyan dinars (LYD) and Saudi riyals (SAR). He has USD 1,000,000 to work with so he gathers the following quotes: Citibank quotes U.S. dollar per Libyan dinar $1.9619 = LYD 1.00 National Bank of Kuwait quotes Saudi riyal per Libyan dinar SAR 1.9107 = LYD 1.00 Barclays quotes U.S. dollar per Saudi riyal $0.2751 = SAR...

Great Pyramids. Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders...

Great Pyramids. Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders if he can make an intermarket arbitrage profit using Libyan dinars (LYD) and Saudi riyals (SAR). He has USD1,000,000 to work with so he gathers the following quotes. Is there an opportunity for an arbitrage profit? Citibank quotes U.S. dollar per Libyan dinar National Bank of Kuwait quotes Saudi riyal per Libyan dinar Barclay quotes U.S. dollar per Saudi riyal $1.9324 LYD1.00 SAR 1.9405...

Great Pyramids. Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders if he can make an intermarket arbitrage profit using Libyan dinars (LYD) and Saudi riyals (SAR). He has USD1,000,000 to work with so he gathers the following quotes. Is there an opportunity for an arbitrage profit? Citibank quotes U.S. dollar per Libyan dinar National Bank of Kuwait quotes Saudi riyal per Libyan dinar Barclay quotes U.S. dollar per Saudi riyal $1.9324 LYD1.00 SAR 1.9405...

Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders if he...

Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders if he can make an intermarket arbitrage profit using Libyan dinars (LYD) and Saudi riyals (SAR). He has USD 1,000,000 to work with so he gathers the following quotes: Citibank quotes U.S. dollar per Libyan dinar $2.00 = LYD 1.00 National Bank of Kuwait quotes Saudi riyal per Libyan dinar SAR 5.00 = LYD 1.00 Barclays quotes U.S. dollar per Saudi riyal $0.25 = SAR 1.00...

Problem 2 Assume the following quotes: Citibank National Westminster Deutsche Bank Assume that the trader has...

Problem 2 Assume the following quotes: Citibank National Westminster Deutsche Bank Assume that the trader has EUR 10,000,000. What profit can a trader make? NOK/EUR 8 DKK/EUR 7.5 NOK/DKK 1.1

Problem 2 Assume the following quotes: Citibank National Westminster Deutsche Bank Assume that the trader has EUR 10,000,000. What profit can a trader make? NOK/EUR 8 DKK/EUR 7.5 NOK/DKK 1.1

hello can someone tell me how this calculatipn is done? Triangular arbitrage (demo version) • Quoted...

hello can someone tell me how this calculatipn is

done?

Triangular arbitrage (demo version) • Quoted rates Citibank quotes US dollars per euro Barclays Bank quotes U.S. dollars per pound sterling Dresdner Bank quotes euros per pound sterling USD1.3297 = 1 EUR USD1.5585 = 1 GBP EUR1.1722 = 1 GBP • Cross rate based on Citibank and Barclays Bank quotes: GBP/USD 1.5585 EUR/USD 1.1722 = GBP/EUR 1.1721 • This is .0001 less than the Dresdner Bank quote, which results in...

hello can someone tell me how this calculatipn is

done?

Triangular arbitrage (demo version) • Quoted rates Citibank quotes US dollars per euro Barclays Bank quotes U.S. dollars per pound sterling Dresdner Bank quotes euros per pound sterling USD1.3297 = 1 EUR USD1.5585 = 1 GBP EUR1.1722 = 1 GBP • Cross rate based on Citibank and Barclays Bank quotes: GBP/USD 1.5585 EUR/USD 1.1722 = GBP/EUR 1.1721 • This is .0001 less than the Dresdner Bank quote, which results in...

You are a U.S.-based treasurer with $1,000,000 to invest. The dollar-euro exchange rate is quoted as...

You are a U.S.-based treasurer with $1,000,000 to invest. The dollar-euro exchange rate is quoted as $1.60 = €1.00 and the dollar-pound exchange rate is quoted at $2.00 = £1.00. If a bank quotes you a cross rate of £1.00 = €1.20 how much money can an astute trader make? Multiple Choice • No arbitrage is possible 0 $1,160,000 0 $41,667 0 $40,000

You are a U.S.-based treasurer with $1,000,000 to invest. The dollar-euro exchange rate is quoted as $1.60 = €1.00 and the dollar-pound exchange rate is quoted at $2.00 = £1.00. If a bank quotes you a cross rate of £1.00 = €1.20 how much money can an astute trader make? Multiple Choice • No arbitrage is possible 0 $1,160,000 0 $41,667 0 $40,000

You are a U.S.-based treasurer with $1,000,000 to invest. The dollar-euro exchange rate is quoted as...

You are a U.S.-based treasurer with $1,000,000 to invest. The dollar-euro exchange rate is quoted as $1.50 = €1.00 and the dollar-pound exchange rate is quoted at $2.00 = £1.00. If a bank quotes you a cross rate of £1.00 = €1.25, is there an arbitrage opportunity? If so, how much money would you make? Show all workings.

23) Country Switzerland (Franc) CHF Euro € USD equivalent BID ASK 0.7648 0.7652 1.4000 1.4200 What...

23) Country Switzerland (Franc) CHF Euro € USD equivalent BID ASK 0.7648 0.7652 1.4000 1.4200 What is the ASK cross-exchange rate for Swiss Francs priced in euro? Hint: Find the price that a currency dealer will take in euro to sell Swiss francs. A) €0.5386/CHF B) €0.5466/CHF €0.5389/CHF D) €0.5463/CHF 24) 24) Suppose a bank customer with €1,000,000 wishes to trade out of euro and into Japanese yen. The dollar-curo exchange rate is quoted as $1.70 - €1.00 and the...

23) Country Switzerland (Franc) CHF Euro € USD equivalent BID ASK 0.7648 0.7652 1.4000 1.4200 What is the ASK cross-exchange rate for Swiss Francs priced in euro? Hint: Find the price that a currency dealer will take in euro to sell Swiss francs. A) €0.5386/CHF B) €0.5466/CHF €0.5389/CHF D) €0.5463/CHF 24) 24) Suppose a bank customer with €1,000,000 wishes to trade out of euro and into Japanese yen. The dollar-curo exchange rate is quoted as $1.70 - €1.00 and the...

Derek Jones, a foreign exchange trader at Charles Schwab, can invest $1 million, or the foreign...

Derek Jones, a foreign exchange trader at Charles Schwab, can invest $1 million, or the foreign currency equivalent of the bank’s short-term funds, in a covered interest arbitrage with Japan. Using the following quotes, can Derek make a covered interest arbitrage profit? If so, show the steps and calculate the amount of profit in USD. Arbitrage funds available $1,000,000 Spot exchange rate (¥/$) ¥106.00/$ 6-month forward rate (¥/$) ¥103.50/$ US dollar 6-month interest rate 4% Japanese yen 6-month interest rate...

1. Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders if he can make an intermarket arbitrage profit using Libyan dinars (LYD) and Saudi riyals (SAR). He has USD 1,000,000 to work with so he gathers the following quotes: Citibank quotes U.S. dollar per Libyan dinar $1.9619 = LYD 1.00 National Bank of Kuwait quotes Saudi riyal per Libyan dinar SAR 1.9107 = LYD 1.00 Barclays quotes U.S. dollar per Saudi riyal $0.2751 = SAR...

1. Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders if he can make an intermarket arbitrage profit using Libyan dinars (LYD) and Saudi riyals (SAR). He has USD 1,000,000 to work with so he gathers the following quotes: Citibank quotes U.S. dollar per Libyan dinar $1.9619 = LYD 1.00 National Bank of Kuwait quotes Saudi riyal per Libyan dinar SAR 1.9107 = LYD 1.00 Barclays quotes U.S. dollar per Saudi riyal $0.2751 = SAR...

Great Pyramids. Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders if he can make an intermarket arbitrage profit using Libyan dinars (LYD) and Saudi riyals (SAR). He has USD1,000,000 to work with so he gathers the following quotes. Is there an opportunity for an arbitrage profit? Citibank quotes U.S. dollar per Libyan dinar National Bank of Kuwait quotes Saudi riyal per Libyan dinar Barclay quotes U.S. dollar per Saudi riyal $1.9324 LYD1.00 SAR 1.9405...

Great Pyramids. Inspired by his recent trip to the Great Pyramids, Citibank trader Ruminder Dhillon wonders if he can make an intermarket arbitrage profit using Libyan dinars (LYD) and Saudi riyals (SAR). He has USD1,000,000 to work with so he gathers the following quotes. Is there an opportunity for an arbitrage profit? Citibank quotes U.S. dollar per Libyan dinar National Bank of Kuwait quotes Saudi riyal per Libyan dinar Barclay quotes U.S. dollar per Saudi riyal $1.9324 LYD1.00 SAR 1.9405...

Problem 2 Assume the following quotes: Citibank National Westminster Deutsche Bank Assume that the trader has EUR 10,000,000. What profit can a trader make? NOK/EUR 8 DKK/EUR 7.5 NOK/DKK 1.1

Problem 2 Assume the following quotes: Citibank National Westminster Deutsche Bank Assume that the trader has EUR 10,000,000. What profit can a trader make? NOK/EUR 8 DKK/EUR 7.5 NOK/DKK 1.1

hello can someone tell me how this calculatipn is

done?

Triangular arbitrage (demo version) • Quoted rates Citibank quotes US dollars per euro Barclays Bank quotes U.S. dollars per pound sterling Dresdner Bank quotes euros per pound sterling USD1.3297 = 1 EUR USD1.5585 = 1 GBP EUR1.1722 = 1 GBP • Cross rate based on Citibank and Barclays Bank quotes: GBP/USD 1.5585 EUR/USD 1.1722 = GBP/EUR 1.1721 • This is .0001 less than the Dresdner Bank quote, which results in...

hello can someone tell me how this calculatipn is

done?

Triangular arbitrage (demo version) • Quoted rates Citibank quotes US dollars per euro Barclays Bank quotes U.S. dollars per pound sterling Dresdner Bank quotes euros per pound sterling USD1.3297 = 1 EUR USD1.5585 = 1 GBP EUR1.1722 = 1 GBP • Cross rate based on Citibank and Barclays Bank quotes: GBP/USD 1.5585 EUR/USD 1.1722 = GBP/EUR 1.1721 • This is .0001 less than the Dresdner Bank quote, which results in...

You are a U.S.-based treasurer with $1,000,000 to invest. The dollar-euro exchange rate is quoted as $1.60 = €1.00 and the dollar-pound exchange rate is quoted at $2.00 = £1.00. If a bank quotes you a cross rate of £1.00 = €1.20 how much money can an astute trader make? Multiple Choice • No arbitrage is possible 0 $1,160,000 0 $41,667 0 $40,000

You are a U.S.-based treasurer with $1,000,000 to invest. The dollar-euro exchange rate is quoted as $1.60 = €1.00 and the dollar-pound exchange rate is quoted at $2.00 = £1.00. If a bank quotes you a cross rate of £1.00 = €1.20 how much money can an astute trader make? Multiple Choice • No arbitrage is possible 0 $1,160,000 0 $41,667 0 $40,000

23) Country Switzerland (Franc) CHF Euro € USD equivalent BID ASK 0.7648 0.7652 1.4000 1.4200 What is the ASK cross-exchange rate for Swiss Francs priced in euro? Hint: Find the price that a currency dealer will take in euro to sell Swiss francs. A) €0.5386/CHF B) €0.5466/CHF €0.5389/CHF D) €0.5463/CHF 24) 24) Suppose a bank customer with €1,000,000 wishes to trade out of euro and into Japanese yen. The dollar-curo exchange rate is quoted as $1.70 - €1.00 and the...

23) Country Switzerland (Franc) CHF Euro € USD equivalent BID ASK 0.7648 0.7652 1.4000 1.4200 What is the ASK cross-exchange rate for Swiss Francs priced in euro? Hint: Find the price that a currency dealer will take in euro to sell Swiss francs. A) €0.5386/CHF B) €0.5466/CHF €0.5389/CHF D) €0.5463/CHF 24) 24) Suppose a bank customer with €1,000,000 wishes to trade out of euro and into Japanese yen. The dollar-curo exchange rate is quoted as $1.70 - €1.00 and the...

Most questions answered within 3 hours.

-

Beginning Retained Earnings are $ 79 comma 000 $79,000; sales

are $ 31 comma 700 $31,700;...

asked 2 seconds ago -

Please explain/demonstrate how to use NLTK to test unigram,

bigram, and trigram character models on guessing...

asked 6 minutes ago -

what you feel is most important to you and why regarding your

typing skills?

asked 7 minutes ago -

Consider a play of the casino game `Quick Draw'. In this game, a

player pays $11...

asked 16 minutes ago -

How do the mechanical features of bone affect its roles as

repositories of phosphate and calcium,...

asked 20 minutes ago -

P agreed to buy 100 barrels of widget oil, which was stored in a

large tank...

asked 21 minutes ago -

The unstable isotope 40K is used for dating rock samples. Its

half-life is 1.28×109y. How many...

asked 23 minutes ago -

Compare and contrast constructed-response items and

selected-response items.

Identify at least one (1) advantage and one...

asked 25 minutes ago -

A) Find the moment of inertia of a 2 meter long stick with a

mass of...

asked 24 minutes ago -

For the code below write a public static main() method

in class Student that:

- creates...

asked 26 minutes ago -

Please show all steps. Thank you

A 1.0-cm-diameter pipe widens to 2.0 cm, then narrows to...

asked 39 minutes ago -

The equilibrium constant for the following reaction Ag+(aq) +

2NH3(aq) Ag(NH3)2+(aq) is K = 1.7 ×...

asked 48 minutes ago