-

Problem 3-15 Journal Entries; T-Accounts; Financial Statements

[LO3-1, LO3-2, LO3-3, LO3-4]

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements

[LO3-1, LO3-2, LO3-3, LO3-4]

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing...

-

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] points Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours....

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] points Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours....

-

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

-

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

-

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

-

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

-

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $351,500 of manufacturing overhead for an estimated allocation base of 950 direct labor-hours. The following...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $351,500 of manufacturing overhead for an estimated allocation base of 950 direct labor-hours. The following...

-

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oll fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $329,000 of manufacturing overhead for an estimated allocation base of 940 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oll fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $329,000 of manufacturing overhead for an estimated allocation base of 940 direct labor-hours. The...

-

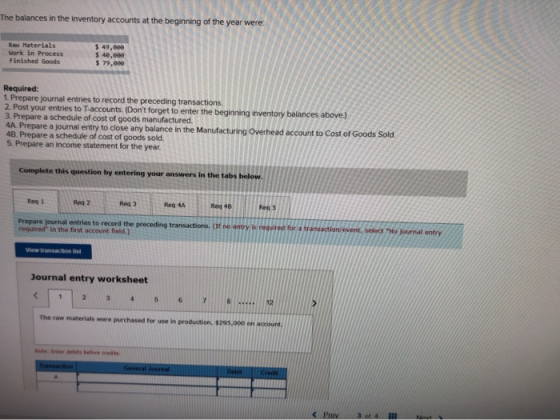

1. Prepare journal entries to record the preceding

transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the

beginning inventory balances above.)

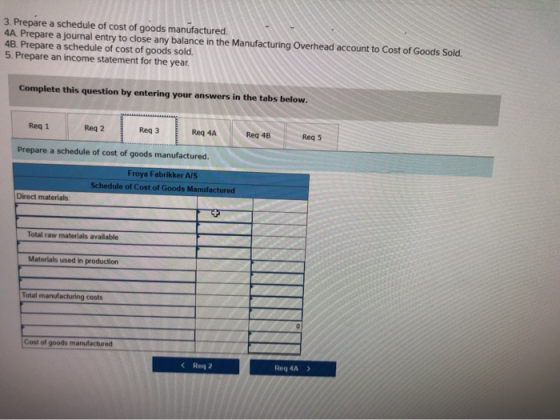

3. Prepare a schedule of cost of goods manufactured.

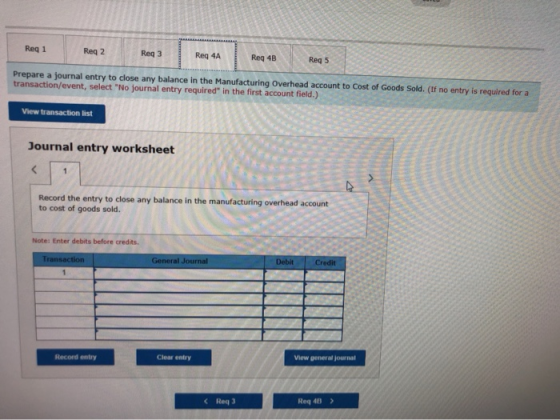

4A. Prepare a journal entry to close any balance in the

Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Froya Fabrikker A/S of Bergen, Norway, is a small company that...

1. Prepare journal entries to record the preceding

transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the

beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the

Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Froya Fabrikker A/S of Bergen, Norway, is a small company that...

-

LOOR I S A Merchandiser That Provided The Che Luxtor map Prescot AL Graded Homework saved Help Save Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a...

LOOR I S A Merchandiser That Provided The Che Luxtor map Prescot AL Graded Homework saved Help Save Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a...

![Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, No](http://img.homeworklib.com/questions/652659e0-798f-11ea-9556-6bf0a0f7d1a4.png?x-oss-process=image/resize,w_560)

Problem 3-15 Journal Entries; T-Accounts; Financial Statements

[LO3-1, LO3-2, LO3-3, LO3-4]

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements

[LO3-1, LO3-2, LO3-3, LO3-4]

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $350,000 of manufacturing...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] points Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours....

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] points Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours....

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $349,800 of manufacturing overhead for an estimated allocation base of 1,060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $399,000 of manufacturing overhead for an estimated allocation base of 1,050 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $395,600 of manufacturing overhead for an estimated allocation base of 920 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a cost formula that estimated $349.800 of manufacturing overhead for an estimated allocation base of 1.060 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $351,500 of manufacturing overhead for an estimated allocation base of 950 direct labor-hours. The following...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4] Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor-hours. Its predetermined overhead rate was based on a cost formula that estimated $351,500 of manufacturing overhead for an estimated allocation base of 950 direct labor-hours. The following...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oll fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $329,000 of manufacturing overhead for an estimated allocation base of 940 direct labor-hours. The...

Problem 3-15 Journal Entries; T-Accounts; Financial Statements (LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oll fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor- hours. Its predetermined overhead rate was based on a cost formula that estimated $329,000 of manufacturing overhead for an estimated allocation base of 940 direct labor-hours. The...

1. Prepare journal entries to record the preceding

transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the

beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the

Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Froya Fabrikker A/S of Bergen, Norway, is a small company that...

1. Prepare journal entries to record the preceding

transactions.

2. Post your entries to T-accounts. (Don’t forget to enter the

beginning inventory balances above.)

3. Prepare a schedule of cost of goods manufactured.

4A. Prepare a journal entry to close any balance in the

Manufacturing Overhead account to Cost of Goods Sold.

4B. Prepare a schedule of cost of goods sold.

5. Prepare an income statement for the year.

Froya Fabrikker A/S of Bergen, Norway, is a small company that...

LOOR I S A Merchandiser That Provided The Che Luxtor map Prescot AL Graded Homework saved Help Save Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a...

LOOR I S A Merchandiser That Provided The Che Luxtor map Prescot AL Graded Homework saved Help Save Problem 3-15 Journal Entries; T-Accounts; Financial Statements [LO3-1, LO3-2, LO3-3, LO3-4) Froya Fabrikker A/S of Bergen, Norway, is a small company that manufactures specialty heavy equipment for use in North Sea oil fields. The company uses a job-order costing system that applies manufacturing overhead cost to jobs on the basis of direct labor hours. Its predetermined overhead rate was based on a...