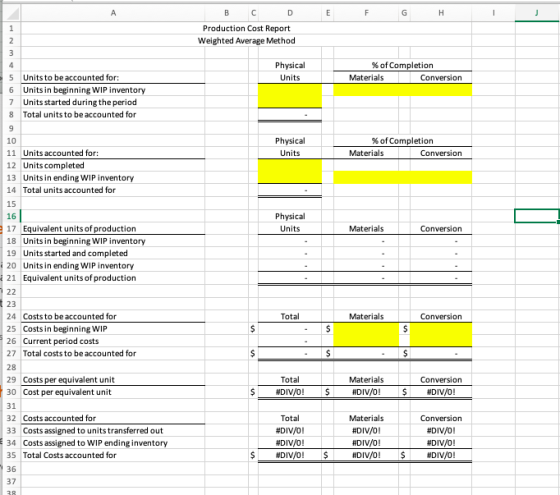

Bisson Furniture uses a process cost system to account for its

chair factory. Beginning inventory consisted of 5,000 units (100%

complete as to material, 55% complete as to labor) with a cost of

$124,800 materials and $104,500 conversion. 58,000 units were

started into production during the month with material costs of

$1,537,000 and $2,124,375 of conversion costs. The ending inventory

of 6,000 chairs was 100% complete as to materials and 40% complete

as to labor.

Required: HINT: Use the excel

template found on blackboard “Equivalent Units of Production” to

help you.

Part 1: Using the weighted average costing method:

**WHAT GOES WHERE IT IS YELLOW??

Homework Answers

| Production Cost Report | |||||

| Weighted Average Method | |||||

| Physical | % of Completion | ||||

| Units (a) | % (b) | Materials (a*b) | % (c ) | Conversion (a*c) | |

| Beginning inventory | 5,000 | 100% | 5,000 | 55% | 2,750 |

| Add: Units started into the production | 58,000 | ||||

| Total units accounted for | 63,000 | ||||

| Less: Ending inventory | 6,000 | ||||

| Units completed and transferred out | 57,000 | ||||

| Physical | % of Completion | ||||

| Units accounted for: | Units (a) | % (b) | Materials (a*b) | % (c ) | Conversion (a*c) |

| Units completed and transferred out | 57,000 | 100% | 57,000 | 100% | 57,000 |

| Ending Inventory | 6,000 | 100% | 6,000 | 40% | 2,400 |

| Total units accounted for | 63,000 | ||||

| Physical | % of Completion | ||||

| Equivalent units of production: | Units (a) | % (b) | Materials (a*b) | % (c ) | Conversion (a*c) |

| Units in beginning inventory | 5,000 | 100% | 5,000 | 55% | 2,750 |

| Units started and completed | 57,000 | 100% | 57,000 | 100% | 57,000 |

| Units in ending WIP inventory | 6,000 | 100% | 6,000 | 40% | 2,400 |

| Equivalent units of production (a) | 68,000 | 68,000 | 62,150 | ||

| Costs to be accounted for: | Total | Materials | Conversion | ||

| Costs in beginning WIP ($124,800 + $104,500) | $229,300 | $124,800 | $104,500 | ||

| Current period costs ($1,537,000 + $2,124,375) | $3,661,375 | $1,537,000 | $2,124,375 | ||

| Total costs to be accounted for (b) | $3,890,675 | $1,661,800 | $2,228,875 | ||

| Cost per equivalent unit: | |||||

| Cost per equivalent unit (b / a) | $57.22 | $24.44 | $35.86 | ||

| Costs accounted for: | Total | Materials | Conversion | ||

| Costs assigned to units transferred out ($57.22 * 57,000 units); ($24.44 * 57,000 units); ($35.86 * 57,000 units) | $3,261,301 | $1,392,979 | $2,044,181 | ||

| Costs assigned to WIP ending inventory ($57.22 * 6,000 units); ($24.44 * 6,000 units); ($35.86 * 2,400 units) | $343,295 | $146,629 | $86,071 | ||

| Total costs accounted for | $3,604,596 | $1,539,609 | $2,130,252 | ||

Add Answer to:

Bisson Furniture uses a process cost system to account for its

chair factory. Beginning inventory consisted...

Bisson Furniture uses a process cost system to account for its chair factory. Beginning inventory consisted...

Bisson Furniture uses a process cost system to account for its chair factory. Beginning inventory consisted of 5,000 units (100% complete as to material, 55% complete as to labor) with a cost of $124,800 materials and $104,500 conversion. 58,000 units were started into production during the month with material costs of $1,537,000 and $2,124,375 of conversion costs. The ending inventory of 6,000 chairs was 100% complete as to materials and 40% complete as to labor. Required: HINT: Use the excel...

Kansas Supplies is a manufacturer of plastic parts that uses the weighted-average process costing method to...

Kansas Supplies is a manufacturer of plastic parts that uses the

weighted-average process costing method to account for costs of

production. It produces parts in three separate departments:

Molding, Assembling, and Packaging. The following information was

obtained for the Assembling Department for the month of April.

Work in process on April 1 had 103,000 units made up of the

following.

Amount

Degree of Completion

Prior department costs transferred in from the Molding

Department

$

135,960

100

%

Costs added by...

Kansas Supplies is a manufacturer of plastic parts that uses the

weighted-average process costing method to account for costs of

production. It produces parts in three separate departments:

Molding, Assembling, and Packaging. The following information was

obtained for the Assembling Department for the month of April.

Work in process on April 1 had 103,000 units made up of the

following.

Amount

Degree of Completion

Prior department costs transferred in from the Molding

Department

$

135,960

100

%

Costs added by...

Chapter 4: Applying Excel Data Beginning work in process inventory: Units in process 200 Completion with...

Chapter 4: Applying Excel Data Beginning work in process inventory: Units in process 200 Completion with respect to materials 100% Completion with respect to conversion 40% Costs in the beginning work in process inventory: Materials cost $2,000 Conversion cost $800 Units started into production during the period 1,800 Costs added to production during the period: Materials cost $18,400 Conversion cost $38,765 Ending work in process inventory: Units in process 100 Completion with respect to materials 100% Completion with respect to...

Company uses the weighted average method in its process-costing system. Operating data for the first processing...

Company uses the weighted average method in its process-costing system. Operating data for the first processing department for the last month appear below pertaining to the physical flow of units, direct materials (DM), and conversion costs (CC) 9 of % of completion completion: Units DM CC Beginning WIP inventory 1.100806 50% Started into production during the month 9,800 Ending WIP inventory 2,100 90% ? 3 How many units were transferred out of the first department during the month? 13,000 9,800...

Company uses the weighted average method in its process-costing system. Operating data for the first processing department for the last month appear below pertaining to the physical flow of units, direct materials (DM), and conversion costs (CC) 9 of % of completion completion: Units DM CC Beginning WIP inventory 1.100806 50% Started into production during the month 9,800 Ending WIP inventory 2,100 90% ? 3 How many units were transferred out of the first department during the month? 13,000 9,800...

Kansas Supplies is a manufacturer of plastic parts that uses the weighted-average process costing method to...

Kansas Supplies is a manufacturer of plastic parts that uses the

weighted-average process costing method to account for costs of

production. It produces parts in three separate departments:

Molding, Assembling, and Packaging. The following information was

obtained for the Assembling Department for the month of April.

Work in process on April 1 had 75,000 units made up of the

following.

Amount

Degree of Completion

Prior department costs transferred in from the Molding

Department

$

192,000

100

%

Costs added by...

Kansas Supplies is a manufacturer of plastic parts that uses the

weighted-average process costing method to account for costs of

production. It produces parts in three separate departments:

Molding, Assembling, and Packaging. The following information was

obtained for the Assembling Department for the month of April.

Work in process on April 1 had 75,000 units made up of the

following.

Amount

Degree of Completion

Prior department costs transferred in from the Molding

Department

$

192,000

100

%

Costs added by...

Adams Company uses the weighted average method in its process-costing system. Operating department for the last mon...

Adams Company uses the weighted average method in its process-costing system. Operating department for the last month appear below pertaining to the physi conversion costs (CC) h appear below pertaining to the physical flow of units, direct materials (DM), and og in its process-costing system. Operating data for the first processing % of completion DM 8 0% of completion: CC 50% Beginning WIP inventory Started into production during the month Ending WIP inventory Units 1.100 9.800 2.100 90% 3 How...

Adams Company uses the weighted average method in its process-costing system. Operating department for the last month appear below pertaining to the physi conversion costs (CC) h appear below pertaining to the physical flow of units, direct materials (DM), and og in its process-costing system. Operating data for the first processing % of completion DM 8 0% of completion: CC 50% Beginning WIP inventory Started into production during the month Ending WIP inventory Units 1.100 9.800 2.100 90% 3 How...

all one question Saline Solutions usos process costing to account for production of its unique compound...

all one question

Saline Solutions usos process costing to account for production of its unique compound BG at its River Plant The River Plant has two departments Rand S Raw materials are added at two points in the production of BG. First, rubber pellets are added at the beginning of production in Department R Next, aliquid thinner is added in Department R when the product is 60 percent complete with respect to conversion costs. Once the basic compound is completed...

all one question

Saline Solutions usos process costing to account for production of its unique compound BG at its River Plant The River Plant has two departments Rand S Raw materials are added at two points in the production of BG. First, rubber pellets are added at the beginning of production in Department R Next, aliquid thinner is added in Department R when the product is 60 percent complete with respect to conversion costs. Once the basic compound is completed...

MANAGERIAL ACCOUNTING DISCUSSION PROBLEM 7 PROCESS COSTING-SINGLE DEPARTMENT Van Buren Company manufactures a product that uses...

MANAGERIAL ACCOUNTING DISCUSSION PROBLEM 7 PROCESS COSTING-SINGLE DEPARTMENT Van Buren Company manufactures a product that uses a process cost system to accumulate its costs of production. The following information is available for the month of February regarding costs of production for this product. VAN BUREN COMPANY COSTS OF PRODUCTION FOR PROCESS COSTING ANALYSIS FOR MONTH OF FEBRUARY Beginning WIP: Direct Materials 40,000 Conversion Costs 90,000 Current Period: Direct Materials 375,900 Conversion Costs 575,250 The company had 5,000 units in beginning...

MANAGERIAL ACCOUNTING DISCUSSION PROBLEM 7 PROCESS COSTING-SINGLE DEPARTMENT Van Buren Company manufactures a product that uses a process cost system to accumulate its costs of production. The following information is available for the month of February regarding costs of production for this product. VAN BUREN COMPANY COSTS OF PRODUCTION FOR PROCESS COSTING ANALYSIS FOR MONTH OF FEBRUARY Beginning WIP: Direct Materials 40,000 Conversion Costs 90,000 Current Period: Direct Materials 375,900 Conversion Costs 575,250 The company had 5,000 units in beginning...

sells the products at cost. The direct materials costs are zero, but the tracks the processing...

sells the products at cost. The direct materials costs are zero, but the tracks the processing volume and costs incurred in each period. At the start ot In its Department R, Recyclers, Inc., processes donated scrap cloth into towels for sale in local thrift shops. operation requires the use OT alrect labor and oveliead..e company ses a proces ng During the month, costs of $22,000 were incurred, 4,400 towels were started, and 125 towels were still in process at the...

sells the products at cost. The direct materials costs are zero, but the tracks the processing volume and costs incurred in each period. At the start ot In its Department R, Recyclers, Inc., processes donated scrap cloth into towels for sale in local thrift shops. operation requires the use OT alrect labor and oveliead..e company ses a proces ng During the month, costs of $22,000 were incurred, 4,400 towels were started, and 125 towels were still in process at the...

Victory Company uses weighted-average process costing to account for its production costs. Conversion cost is added...

Victory Company uses weighted-average process costing to

account for its production costs. Conversion cost is added evenly

throughout the process. Direct materials are added at the beginning

of the process. During November, the company transferred 700,000

units of product to finished goods. At the end of November, the

work in process inventory consists of 180,000 units that are 30%

complete with respect to conversion. Beginning inventory had

$420,000 of direct materials and $139,000 of conversion cost. The

direct material cost...

Victory Company uses weighted-average process costing to

account for its production costs. Conversion cost is added evenly

throughout the process. Direct materials are added at the beginning

of the process. During November, the company transferred 700,000

units of product to finished goods. At the end of November, the

work in process inventory consists of 180,000 units that are 30%

complete with respect to conversion. Beginning inventory had

$420,000 of direct materials and $139,000 of conversion cost. The

direct material cost...

Kansas Supplies is a manufacturer of plastic parts that uses the

weighted-average process costing method to account for costs of

production. It produces parts in three separate departments:

Molding, Assembling, and Packaging. The following information was

obtained for the Assembling Department for the month of April.

Work in process on April 1 had 103,000 units made up of the

following.

Amount

Degree of Completion

Prior department costs transferred in from the Molding

Department

$

135,960

100

%

Costs added by...

Kansas Supplies is a manufacturer of plastic parts that uses the

weighted-average process costing method to account for costs of

production. It produces parts in three separate departments:

Molding, Assembling, and Packaging. The following information was

obtained for the Assembling Department for the month of April.

Work in process on April 1 had 103,000 units made up of the

following.

Amount

Degree of Completion

Prior department costs transferred in from the Molding

Department

$

135,960

100

%

Costs added by...

Company uses the weighted average method in its process-costing system. Operating data for the first processing department for the last month appear below pertaining to the physical flow of units, direct materials (DM), and conversion costs (CC) 9 of % of completion completion: Units DM CC Beginning WIP inventory 1.100806 50% Started into production during the month 9,800 Ending WIP inventory 2,100 90% ? 3 How many units were transferred out of the first department during the month? 13,000 9,800...

Company uses the weighted average method in its process-costing system. Operating data for the first processing department for the last month appear below pertaining to the physical flow of units, direct materials (DM), and conversion costs (CC) 9 of % of completion completion: Units DM CC Beginning WIP inventory 1.100806 50% Started into production during the month 9,800 Ending WIP inventory 2,100 90% ? 3 How many units were transferred out of the first department during the month? 13,000 9,800...

Kansas Supplies is a manufacturer of plastic parts that uses the

weighted-average process costing method to account for costs of

production. It produces parts in three separate departments:

Molding, Assembling, and Packaging. The following information was

obtained for the Assembling Department for the month of April.

Work in process on April 1 had 75,000 units made up of the

following.

Amount

Degree of Completion

Prior department costs transferred in from the Molding

Department

$

192,000

100

%

Costs added by...

Kansas Supplies is a manufacturer of plastic parts that uses the

weighted-average process costing method to account for costs of

production. It produces parts in three separate departments:

Molding, Assembling, and Packaging. The following information was

obtained for the Assembling Department for the month of April.

Work in process on April 1 had 75,000 units made up of the

following.

Amount

Degree of Completion

Prior department costs transferred in from the Molding

Department

$

192,000

100

%

Costs added by...

Adams Company uses the weighted average method in its process-costing system. Operating department for the last month appear below pertaining to the physi conversion costs (CC) h appear below pertaining to the physical flow of units, direct materials (DM), and og in its process-costing system. Operating data for the first processing % of completion DM 8 0% of completion: CC 50% Beginning WIP inventory Started into production during the month Ending WIP inventory Units 1.100 9.800 2.100 90% 3 How...

Adams Company uses the weighted average method in its process-costing system. Operating department for the last month appear below pertaining to the physi conversion costs (CC) h appear below pertaining to the physical flow of units, direct materials (DM), and og in its process-costing system. Operating data for the first processing % of completion DM 8 0% of completion: CC 50% Beginning WIP inventory Started into production during the month Ending WIP inventory Units 1.100 9.800 2.100 90% 3 How...

all one question

Saline Solutions usos process costing to account for production of its unique compound BG at its River Plant The River Plant has two departments Rand S Raw materials are added at two points in the production of BG. First, rubber pellets are added at the beginning of production in Department R Next, aliquid thinner is added in Department R when the product is 60 percent complete with respect to conversion costs. Once the basic compound is completed...

all one question

Saline Solutions usos process costing to account for production of its unique compound BG at its River Plant The River Plant has two departments Rand S Raw materials are added at two points in the production of BG. First, rubber pellets are added at the beginning of production in Department R Next, aliquid thinner is added in Department R when the product is 60 percent complete with respect to conversion costs. Once the basic compound is completed...

MANAGERIAL ACCOUNTING DISCUSSION PROBLEM 7 PROCESS COSTING-SINGLE DEPARTMENT Van Buren Company manufactures a product that uses a process cost system to accumulate its costs of production. The following information is available for the month of February regarding costs of production for this product. VAN BUREN COMPANY COSTS OF PRODUCTION FOR PROCESS COSTING ANALYSIS FOR MONTH OF FEBRUARY Beginning WIP: Direct Materials 40,000 Conversion Costs 90,000 Current Period: Direct Materials 375,900 Conversion Costs 575,250 The company had 5,000 units in beginning...

MANAGERIAL ACCOUNTING DISCUSSION PROBLEM 7 PROCESS COSTING-SINGLE DEPARTMENT Van Buren Company manufactures a product that uses a process cost system to accumulate its costs of production. The following information is available for the month of February regarding costs of production for this product. VAN BUREN COMPANY COSTS OF PRODUCTION FOR PROCESS COSTING ANALYSIS FOR MONTH OF FEBRUARY Beginning WIP: Direct Materials 40,000 Conversion Costs 90,000 Current Period: Direct Materials 375,900 Conversion Costs 575,250 The company had 5,000 units in beginning...

sells the products at cost. The direct materials costs are zero, but the tracks the processing volume and costs incurred in each period. At the start ot In its Department R, Recyclers, Inc., processes donated scrap cloth into towels for sale in local thrift shops. operation requires the use OT alrect labor and oveliead..e company ses a proces ng During the month, costs of $22,000 were incurred, 4,400 towels were started, and 125 towels were still in process at the...

sells the products at cost. The direct materials costs are zero, but the tracks the processing volume and costs incurred in each period. At the start ot In its Department R, Recyclers, Inc., processes donated scrap cloth into towels for sale in local thrift shops. operation requires the use OT alrect labor and oveliead..e company ses a proces ng During the month, costs of $22,000 were incurred, 4,400 towels were started, and 125 towels were still in process at the...

Victory Company uses weighted-average process costing to

account for its production costs. Conversion cost is added evenly

throughout the process. Direct materials are added at the beginning

of the process. During November, the company transferred 700,000

units of product to finished goods. At the end of November, the

work in process inventory consists of 180,000 units that are 30%

complete with respect to conversion. Beginning inventory had

$420,000 of direct materials and $139,000 of conversion cost. The

direct material cost...

Victory Company uses weighted-average process costing to

account for its production costs. Conversion cost is added evenly

throughout the process. Direct materials are added at the beginning

of the process. During November, the company transferred 700,000

units of product to finished goods. At the end of November, the

work in process inventory consists of 180,000 units that are 30%

complete with respect to conversion. Beginning inventory had

$420,000 of direct materials and $139,000 of conversion cost. The

direct material cost...

Most questions answered within 3 hours.

-

Consider the quantum number sets listed below.

What is the name of the smallest element for...

asked 45 minutes ago -

In python,write a function nameSet(first, last) that takes a

person's first and last names as input,...

asked 3 hours ago -

How do you think we should value management? Specifically how

might we try to determine MRPL...

asked 2 hours ago -

Suppose the Central Bank of Turkey starts to pay

interest on reserves. Under what circumstances this...

asked 3 hours ago -

For Bergson the concept of Being contains less reality than does

the concept of Becoming. True...

asked 4 hours ago -

What is the hydroxide ion concentration, [OH-], in a solution

with a hydronium ion concentration, [H3O+]...

asked 4 hours ago -

What species is the reducing agent in the following

equation?

Mg(s) + 2HCl (aq) --> MgCl2(aq)...

asked 4 hours ago -

A 50g ice cube is taken out of a freezer at 0 degrees Celsius

and put...

asked 6 hours ago -

How do ratios help you determine trends? What specific

information do managers look at? Is there...

asked 6 hours ago -

A wavelength of 514 nm is used to find an unknown diffraction

grating. If the separation...

asked 6 hours ago -

Use the central limit theorem to find the mean and standard

error of the mean of...

asked 6 hours ago -

You will be given a file that will contain averages for classes

which are divided into...

asked 6 hours ago