Homework Answers

Please do Upvote if you are served. Feel free to reach out in the comments

Cheers!!!

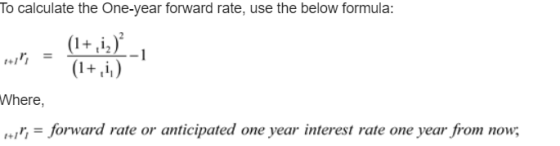

Answer (1):

where i2 = 11% and i1 = 9%

=> i+1rt = (1+0.11)2/(1+0.09) - 1 = 13.04%

Answer (2):

Add Answer to:

1. Assume that as of today we have an annualized two-year interest rate of 11 percent,...

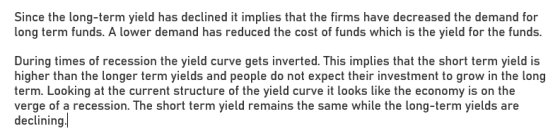

Over the last six months, the long-term yields declined, while short-term yields remained the same. Analysts...

Over the last six months, the long-term yields declined, while short-term yields remained the same. Analysts stated that the shift was due to revised expectations of interest rates. Given the shift in the yield curve, does it appear that firms increased or decreased their demand for long-term funds over the last six months?

Over the last six months, the long-term yields declined, while short-term yields remained the same. Analysts...

Over the last six months, the long-term yields declined, while short-term yields remained the same. Analysts stated that the shift was due to revised expectations of interest rates. Given the shift in the yield curve, does it appear that firms increased or decreased their demand for long-term funds over the last six months? Look up the current yield curve from the US Treasury site and research yield curve implications for recessional or boom market climates. What do you interpret from...

(1.) Consider the following annualized spot yields: Maturity Annualized Spot Rate One Year 5.00% Two Years...

(1.) Consider the following annualized spot yields: Maturity Annualized Spot Rate One Year 5.00% Two Years 5.50% Three Years 6.00% Four Years 6.00% Five Years ? (a.) Assuming the expectations theory of the term structure is correct, calculate the expected one-year interest rate one year from now (i.e. 1f2). (b.) Assuming the expectations theory of the term structure is correct, calculate the expected one-year interest rate three years from now (i.e. 3f4). (c.) Suppose a forecasting service predicts that th...

In your opinion, what does forward interest rate capture? Why do you think it is important...

In your opinion, what does forward interest rate capture? Why do you think it is important to know the forward rate? Assume that as of today we have an annualized two-year interest rate of 11 percent, while the current one-year interest rate is 9 percent. Given this information, estimate the one-year forward rate and describe how you got the answer.

In your opinion, what does forward interest rate capture. Why do you think it is important...

In your opinion, what does forward interest rate capture. Why do you think it is important to know the forward rate? Assume that as of today we have an annualized two-year interest rate of 11 percent, while the current one-year interest rate is 9 percent. Given this information, estimate the one-year forward rate and describe how you got the answer.

Note: Use of approximation for interest rate parity is OK. Assume the four-year annualized interest rate...

Note: Use of approximation for interest rate parity is OK. Assume the four-year annualized interest rate in the US is 9 percent and the four-year annualized interest rate in Singapore is 6 percent. Assume interest rate parity holds for a four-year horizon. Assume the spot rate of the Singapore dollar is $.60. If the forward rate is used to forecast exchange rates, What will be the forecast for the Singapore dollar’s spot rate in four years? Does this forecast imply...

Assume the following information: Interest rate on borrowed euros is 5 percent annualized Interest rate on...

Assume the following information: Interest rate on borrowed euros is 5 percent annualized Interest rate on dollars loaned out is 6 percent annualized Spot rate for 0.8333 per dollar (one = $1.20) Expected spot rate in five days is 0.85 per dollar Alonso Bank can borrow 10 million What is the euro profit to Alonso Bank over the five-day period from shorting euros and going long on dollars? A. 150,311.11 B. 177,111.11 C. 201,555.56 D. 256,323.33

d) Assume that interest rate parity exists. You expect that the one-year nominal interest rate in...

d) Assume that interest rate parity exists. You expect that the one-year nominal interest rate in the U.S. is 1.995%, while the one-year nominal interest rate in Australia is 3.695%. The spot rate of the Australian dollar is USD0.6939. You will need 15 million Australian Dollars in one year. Today, you purchase a one-year forward contract in Australian Dollars. Estimate how many U.S. Dollars (USD) will you need in one year to fulfill your forward contract.

assume annualized interest rates in the U.S. and the Euro area are 1% and 3%, respectively....

assume annualized interest rates in the U.S. and the Euro area are 1% and 3%, respectively. One Euro is worth $1.20 and the one-year forward rate for the Euro is $1.17669. a.) what is the expected exchange rate in one year under no arbitrage? b.) Is covered interest arbitrage profitable? c.) You are a FX trader and forecast the euro to move $1.22 in one year. Would you buy or sell euros forward today? Why? Quantify your expected arbitrage profit....

. Consider the data given below. The one-year rates can be viewed as spot interest rates, and the two-year rates are yie...

. Consider the data given below. The one-year rates can be

viewed as spot interest rates, and the two-year rates are yields to

maturity in annualized percent

.

The spot exchange rate is ¥130.15/£.

What should be the two-year forward rate to prevent

arbitrage?

two-year one-year U.K. 1.870 1.205 Japan 0.435 0.375

. Consider the data given below. The one-year rates can be

viewed as spot interest rates, and the two-year rates are yields to

maturity in annualized percent

.

The spot exchange rate is ¥130.15/£.

What should be the two-year forward rate to prevent

arbitrage?

two-year one-year U.K. 1.870 1.205 Japan 0.435 0.375

. Consider the data given below. The one-year rates can be

viewed as spot interest rates, and the two-year rates are yields to

maturity in annualized percent

.

The spot exchange rate is ¥130.15/£.

What should be the two-year forward rate to prevent

arbitrage?

two-year one-year U.K. 1.870 1.205 Japan 0.435 0.375

. Consider the data given below. The one-year rates can be

viewed as spot interest rates, and the two-year rates are yields to

maturity in annualized percent

.

The spot exchange rate is ¥130.15/£.

What should be the two-year forward rate to prevent

arbitrage?

two-year one-year U.K. 1.870 1.205 Japan 0.435 0.375

Most questions answered within 3 hours.

-

How can we identify what the horizontal force is when looking at

a merry go round?...

asked 12 minutes ago -

While Dime Community Bank is based in Brooklyn; management has

decided to focus its lending activity...

asked 37 minutes ago -

1) Earnings functions, whereby the log of earnings is regressed

on years of education, years of...

asked 10 minutes ago -

Bruno Corporation is involved in the business of injection

molding of plastics. It is considering the...

asked 16 minutes ago -

What would be the vapor pressure of water at 96°C above a

solution made by dissolving...

asked 31 minutes ago -

Hydration of norbornene

Write the reaction. Discuss the intermediate. Explain how the

equilibrium in the reaction...

asked 38 minutes ago -

Suppose that a party wanted to enter an FRA that expires in 42

days and is...

asked 38 minutes ago -

ABC Ltd. estimated that a new store requires an initial

investment of $800,000. This new store...

asked 39 minutes ago -

1. Review the Nike’s marketing strategy. You must include the

company’s target market, possible market segmentation,...

asked 52 minutes ago -

One of the major advantages of ______________ is to enhance

security for private networks by keeping...

asked 58 minutes ago -

Book:

Title: Framework for

Marketing Management, 15th edition

Author/s: Philip T.

Kotler, Kevin Lane Keller

1....

asked 1 hour ago -

Given Uber’s recent corporate turbulence and ongoing

initiatives, provide a holistic situational analysis of the

environment...

asked 1 hour ago