Homework Answers

Add Answer to:

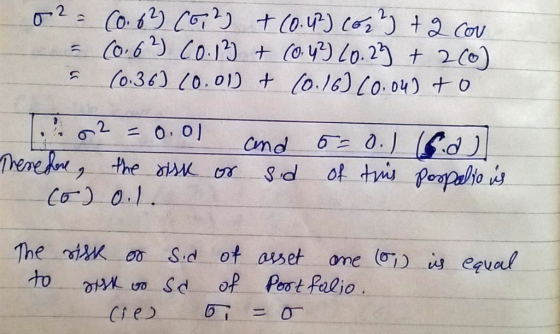

2. (Understanding optimal portfolio choice) Consider two risky assets, the expected return of asset one is...

Question 1 Consider two risky assets A and B with E(rA)= 15%, Sigma_A= 32%, E(rB)= 0.09,...

Question 1 Consider two risky assets A and B with E(rA)= 15%, Sigma_A= 32%, E(rB)= 0.09, Sigma_B= 23%, corrA,B= 0.2. The risk free rate is 5%. The optimal risky portfolio of comprised of the two risky assets is to allocate 64% to A and the rest to B. What is the standard deviation of the optimal risky portfolio ? Select one: a. 20.75% b. 23.61% c. 22.86% d. 23.00% Question 2 Continued with previous question. What is the Sharpe ratio...

Consider a portfolio consisting of the following two risky assets. Asset i Hi, Return on Asset...

Consider a portfolio consisting of the following two risky assets. Asset i Hi, Return on Asset i 7% 7% 0, Risk in Asset i 18% 14% The coefficient of correlation between the returns is p = -100%. (a) State the expected return and associated risk (as measured by the standard deviation) in terms of w if w is the weight allocation of Asset 1 in the portfolio. Hry (w) = 0.07 Or, (w) = sqrt(0.0632w^2-0.C (b) Suppose that the portfolio...

Consider a portfolio consisting of the following two risky assets. Asset i Hi, Return on Asset i 7% 7% 0, Risk in Asset i 18% 14% The coefficient of correlation between the returns is p = -100%. (a) State the expected return and associated risk (as measured by the standard deviation) in terms of w if w is the weight allocation of Asset 1 in the portfolio. Hry (w) = 0.07 Or, (w) = sqrt(0.0632w^2-0.C (b) Suppose that the portfolio...

There are only two risky assets (stocks) A and B in the market. Asset A: Mean...

There are only two risky assets (stocks) A and B in the market. Asset A: Mean = 20% Standard Deviation = 10% Asset B: Mean = 10% Standard Deviation = 5% Returns on Assets have zero correlation. A.Assume that there is no risk-free asset. (i)Plot (sketch) the efficiency frontier (the investment opportunity set). (ii)What is the expected return and the standard deviation of the minimum-variance-portfolio? (iii)An investor would like to construct a portfolio that has a standard deviation of 8%....

2. Consider an economy with 2 risky assets and one risk free asset. Two investors, A...

2. Consider an economy with 2 risky assets and one risk free asset. Two investors, A and B, have mean-variance utility functions (with different risk aversion coef- ficients). Let P denote investor A's optimal portfolio of risky and risk-free assets and let Q denote investor B's optimal portfolio of risky and risk-free assets. P and Q have expected returns and standard deviations given by P Q E[R] St. Dev. 0.2 0.45 0.1 0.25 (a) What is the risk-free interest rate...

2. Consider an economy with 2 risky assets and one risk free asset. Two investors, A and B, have mean-variance utility functions (with different risk aversion coef- ficients). Let P denote investor A's optimal portfolio of risky and risk-free assets and let Q denote investor B's optimal portfolio of risky and risk-free assets. P and Q have expected returns and standard deviations given by P Q E[R] St. Dev. 0.2 0.45 0.1 0.25 (a) What is the risk-free interest rate...

Eric is dividing his portfolio between two assets, a risky asset that has an expected return...

Eric is dividing his portfolio between two assets, a risky asset that has an expected return of 30% and a standard deviation of 10%, and a safe asset that has an expected return of 10% and a standard deviation of 0%. Eric's budget constraint is rx= 2σ?+10. Eric’s utility function is ?(??,σ?)=???(??,30−2σ?). What are his optimal values of ?? and ???

Which of the following is a TRUE statement? A The tangent portfolio is the risky portfolio...

Which of the following is a TRUE statement? A The tangent portfolio is the risky portfolio on the efficient frontier whose tangent line cuts the horizontal axis at the risk-free rate. B The new (or super) efficient frontier represents the portfolios composed of the risk-free rate and the tangent portfolio that offers the highest expected rate of return for any given level or risk. C The separation theorem states that the investment decision, (how to construct the portfolio of risky...

1. Consider a portfolio P comprised of two risky assets (A and B) whose returns have...

1. Consider a portfolio P comprised of two risky assets (A and B) whose returns have a correlation of zero. Risky asset A has an expected return of 10% and standard deviation of 15%. Risky asset B has an expected return of 7% and standard deviation of 11%. Assuming a risk-free rate of 2.5%, what is the standard deviation of returns on the optimal risky portfolio? a) 9.18% b) .918% c) .84% d) 8.42%

Suppose there are three assets: A, B, and C. Asset A’s expected return and standard deviation are 1 percent and 1 percent. Asset B has the same expected return and standard deviation as Asset A. However, the correlation coefficient of Assets A and B is −0

Suppose there are three assets: A, B, and C. Asset A’s expected return and

standard deviation are 1 percent and 1 percent. Asset B has the same expected

return and standard deviation as Asset A. However, the correlation coefficient of

Assets A and B is −0.25. Asset C’s return is independent of the other two assets.

The expected return and standard deviation of Asset C are 0.5 percent and 1

percent.

(a) Find a portfolio of the three assets that...

Suppose there are three assets: A, B, and C. Asset A’s expected return and

standard deviation are 1 percent and 1 percent. Asset B has the same expected

return and standard deviation as Asset A. However, the correlation coefficient of

Assets A and B is −0.25. Asset C’s return is independent of the other two assets.

The expected return and standard deviation of Asset C are 0.5 percent and 1

percent.

(a) Find a portfolio of the three assets that...

There are three assets, A, B and C, where A is the market portfolio and C...

There are three assets, A, B and C, where A is the market portfolio and C is the risk-free asset. The return on the market has a mean of 12% and a standard deviation of 20%. The risk-free asset yields a return of 4%. Asset B is a risky asset whose return has a standard deviation of 40% and a market beta of 1. Assume that the CAPM holds. Compute the expected return of asset B and its covariances with...

Portfolio analvsis (8 points L3 points) Asset A has an expected return of 10% and a...

Portfolio analvsis (8 points L3 points) Asset A has an expected return of 10% and a Sharpe ratio of 0.4. Asset B bas ans expectod retum of 15% and a Sharpe ratio of o3. Asset C has an expected return of 20% and a Sharpe ratio of 0.35. A risk-averse investor would prefer to build a complete portfolio using the risk free asset and a Asset A b. Asset B c Asset C d. No risky asset 2 (3 points)...

Portfolio analvsis (8 points L3 points) Asset A has an expected return of 10% and a Sharpe ratio of 0.4. Asset B bas ans expectod retum of 15% and a Sharpe ratio of o3. Asset C has an expected return of 20% and a Sharpe ratio of 0.35. A risk-averse investor would prefer to build a complete portfolio using the risk free asset and a Asset A b. Asset B c Asset C d. No risky asset 2 (3 points)...

Consider a portfolio consisting of the following two risky assets. Asset i Hi, Return on Asset i 7% 7% 0, Risk in Asset i 18% 14% The coefficient of correlation between the returns is p = -100%. (a) State the expected return and associated risk (as measured by the standard deviation) in terms of w if w is the weight allocation of Asset 1 in the portfolio. Hry (w) = 0.07 Or, (w) = sqrt(0.0632w^2-0.C (b) Suppose that the portfolio...

Consider a portfolio consisting of the following two risky assets. Asset i Hi, Return on Asset i 7% 7% 0, Risk in Asset i 18% 14% The coefficient of correlation between the returns is p = -100%. (a) State the expected return and associated risk (as measured by the standard deviation) in terms of w if w is the weight allocation of Asset 1 in the portfolio. Hry (w) = 0.07 Or, (w) = sqrt(0.0632w^2-0.C (b) Suppose that the portfolio...

2. Consider an economy with 2 risky assets and one risk free asset. Two investors, A and B, have mean-variance utility functions (with different risk aversion coef- ficients). Let P denote investor A's optimal portfolio of risky and risk-free assets and let Q denote investor B's optimal portfolio of risky and risk-free assets. P and Q have expected returns and standard deviations given by P Q E[R] St. Dev. 0.2 0.45 0.1 0.25 (a) What is the risk-free interest rate...

2. Consider an economy with 2 risky assets and one risk free asset. Two investors, A and B, have mean-variance utility functions (with different risk aversion coef- ficients). Let P denote investor A's optimal portfolio of risky and risk-free assets and let Q denote investor B's optimal portfolio of risky and risk-free assets. P and Q have expected returns and standard deviations given by P Q E[R] St. Dev. 0.2 0.45 0.1 0.25 (a) What is the risk-free interest rate...

Portfolio analvsis (8 points L3 points) Asset A has an expected return of 10% and a Sharpe ratio of 0.4. Asset B bas ans expectod retum of 15% and a Sharpe ratio of o3. Asset C has an expected return of 20% and a Sharpe ratio of 0.35. A risk-averse investor would prefer to build a complete portfolio using the risk free asset and a Asset A b. Asset B c Asset C d. No risky asset 2 (3 points)...

Portfolio analvsis (8 points L3 points) Asset A has an expected return of 10% and a Sharpe ratio of 0.4. Asset B bas ans expectod retum of 15% and a Sharpe ratio of o3. Asset C has an expected return of 20% and a Sharpe ratio of 0.35. A risk-averse investor would prefer to build a complete portfolio using the risk free asset and a Asset A b. Asset B c Asset C d. No risky asset 2 (3 points)...

Most questions answered within 3 hours.

-

Suppose a brewery has a filling machine that fills 12-ounce

bottles of beer. It is known...

asked 59 minutes ago -

For this problem, carry at least four digits after the decimal

in your calculations. Answers may...

asked 4 hours ago -

Ask a user for three positive integer numbers. Use an input

validation loop to make sure...

asked 4 hours ago -

The most primitive form of data from data analysis perspective

is a. nominal scale b. ordinal...

asked 4 hours ago -

The number of vacancies in some hypothetical metal increases by

a factor of 5 when the...

asked 4 hours ago -

The fiduciary duty that is predicated on the concept that a

board of directors and officers...

asked 4 hours ago -

Sustainable Growth Rate Last year Umbrellas Unlimited

Corporation had an ROE of 17.3% and a dividend...

asked 4 hours ago -

Write a MATLAB program to do the following:

Receive 5 input values and store them into...

asked 4 hours ago -

Which one of the following aqueous solutions would you expect to

have the largest conductance: (a)...

asked 4 hours ago -

(Intermediate Macroeconomics)

2.The aggregate supply function be ys=2000+P, and the aggregate

demand function be yD=2400-P。Find the...

asked 4 hours ago -

I am having a really difficult time developing a strong thesis

for this question....... To what...

asked 5 hours ago -

There are n street lights in a line. In order to conserve

energy, the city decides...

asked 5 hours ago