2) (20 points) Lynn has a utility function U(W) = W1/2, where W is the amount...

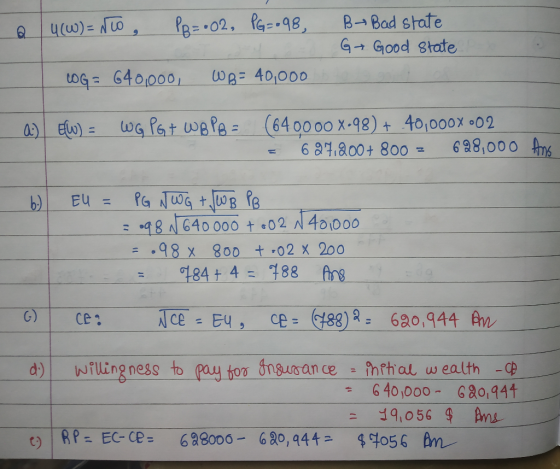

2) (20 points) Lynn has a utility function U(W) = W1/2, where W is the amount of wealth that she has. Lynn has two assets. She has $40,000 in a bank account, and she has a house worth $600,000, so her total wealth is initially $640,000. There is a 2% chance that her house is destroyed by a fire.

a) (4 points) Considering the probability that there is a fire, what is Lynn’s Expected Wealth, E(W)?

E(W) = ____________________________

b) (4 points) What is Lynn’s Expected Utility, E(U)?

E(U) = ______________________________

c) (4 points) What is Lynn’s Certainty Equivalent?

CE = ______________________________

d) (4 points) How much would Lynn be willing to pay for fire insurance?

WTP = _______________________________

e) (4 points) What is Lynn’s Risk Premium?

Risk Premium = _____________________________

Homework Answers

Add Answer to:

2) (20 points) Lynn has a utility function U(W) = W1/2, where W

is the amount...

My von Neumann Morgenstern utility function is U (W) = 32 + (9/5)w1/2 for wealth w....

My von Neumann Morgenstern utility function is U (W) = 32 + (9/5)w1/2 for wealth w. I face a gamble that pays 1 with probability %, and 4 with probability %. Calculate my certainty equivalent for this gamble: CE=_ . Calculate my risk premium p for this gamble p=

My von Neumann Morgenstern utility function is U (W) = 32 + (9/5)w1/2 for wealth w. I face a gamble that pays 1 with probability %, and 4 with probability %. Calculate my certainty equivalent for this gamble: CE=_ . Calculate my risk premium p for this gamble p=

Cindy is an expected utility maximizing consumer who has an initial wealth of $160,000 and is...

Cindy is an expected utility maximizing consumer who has an initial wealth of $160,000 and is subject to fire risk. There is a 5% chance of a major fire with a loss of $70,000 and a 5% chance of a disastrous fire with a loss of $120,000. Her utility function is U = W1/2. Cindy is offered an insurance policy costing $12,000 with a deductible provision, which requires that she pay the first $7,620 on any fire loss (that is,...

i) Suppose that Mary’s utility function is where W is wealth. Is she risk averse? Suppose...

i) Suppose that Mary’s utility function is where W is wealth. Is she risk averse? Suppose that Mary has initial wealth of $125,000. How much of a risk premium would she require to participate in a gamble that has a 50% probability of raising her wealth to $160,000 and a 50% probability of lowering her wealth to $90,000? ii) Suppose that Irma’s utility function with respect to wealth is U(W) = 100 + 80W − W2. Find her Arrow-Pratt risk...

Terry’s utility of wealth is given by: u(w) = ln(w). Suppose Terry has $1 million in...

Terry’s utility of wealth is given by: u(w) = ln(w). Suppose Terry has $1 million in his bank account and a beach house worth $2 million. With probability 1/3, his beach house will get destroyed by a hurricane. (a) Is Terry risk-averse, risk-neutral, or risk-loving? Verify your answer using calculus. (b) Determine the actuarially fair premium for an insurance plan that will compensate him $2 million if his beach house gets destroyed by a hurricane. (c) Write out the two...

Consider the utility function of an individual given by u(x) - ln(x - 10, 000). His...

Consider the utility function of an individual given by u(x) - ln(x - 10, 000). His total wealth is $270,000 of which S170,000 is the worth of his house. There is 10% probability that his house may be destroyed by fire. (a) What is the risk attitude of this person? (10%) (b) Calculate the insurance premium. fair premium and risk premium. (1596) (c) What is the relationship between the insurance premium, fair premium, and 2.

Consider the utility function of an individual given by u(x) - ln(x - 10, 000). His total wealth is $270,000 of which S170,000 is the worth of his house. There is 10% probability that his house may be destroyed by fire. (a) What is the risk attitude of this person? (10%) (b) Calculate the insurance premium. fair premium and risk premium. (1596) (c) What is the relationship between the insurance premium, fair premium, and 2.

Consider the utility function u(x) = ax + b e^cx where a, b, c are positive...

Consider the utility function u(x) = ax + b e^cx where a, b, c are positive scalars. (a) Compute the coefficient of absolute risk aversion. (b) Describe the risk attitude represented by u(x) and how it changes as x increases. (c) Write down the equations to determine the certainty equivalent and the risk premium of a gamble X for an individual with initial wealth w > 0. (d) What is the sign of the risk premium? How does the risk...

Ann is risk-averse with a Bernoulli utility function u(w) = 100 + w^1/2 where w is...

Ann is risk-averse with a Bernoulli utility function u(w) = 100 + w^1/2 where w is her wealth in dollars. Ann’s current wealth is one million dollars, including her small boat valued at $180, 000. She estimates that with 10% probability the boat will sink and lose its full value; with 15% probability there will be damages and the boat will lose half its value, and with 25% probability the boat will lose a quarter of its value; otherwise, the...

A risk agent, whose utility is given by U(w) = 150+w and initial wealth is $10,000...

A risk agent, whose utility is given by U(w) = 150+w and initial wealth is $10,000 is faced with a potential loss of $3,500 with a probability of p= 0.20. Find Expected value(EV). Find Expected Utility(EW). What is the maximum premium they would be willing to pay to protect themselves against this loss?

Question 1 (20 marks) (a) A consumer maximizes utility and has Bernoulli utility function u(w)/2. The...

Question 1 (20 marks) (a) A consumer maximizes utility and has Bernoulli utility function u(w)/2. The consumer has initial wealth w 1000 and faces two potential losses. With probability 0.1, the consumer loses S100, and with probability 0.2, the consumer loses $50. Assume that both losses cannot occur at the same time. What is the most this consumer would be willing to pay for full insurance against these losses? (10 marks) (b) A consumer has utility function u(z, y) In(x)...

Question 1 (20 marks) (a) A consumer maximizes utility and has Bernoulli utility function u(w)/2. The consumer has initial wealth w 1000 and faces two potential losses. With probability 0.1, the consumer loses S100, and with probability 0.2, the consumer loses $50. Assume that both losses cannot occur at the same time. What is the most this consumer would be willing to pay for full insurance against these losses? (10 marks) (b) A consumer has utility function u(z, y) In(x)...

1*. Maria’s house is worth 1 000 000 SEK. Her utility function is given by U...

1*. Maria’s house is worth 1 000 000 SEK. Her utility function is given by U = m0,5, where m represents her wealth (the value of the house). The probability of the house burning down is 0,2. A fire would reduce the house value to 300 000 SEK. a) Calculate the expected value of Maria’s wealth. b) Calculate the utility of the expected wealth, given that Maria gets it for sure. c) Calculate Maria´s expected utility of Maria’s uncertain situation....

My von Neumann Morgenstern utility function is U (W) = 32 + (9/5)w1/2 for wealth w. I face a gamble that pays 1 with probability %, and 4 with probability %. Calculate my certainty equivalent for this gamble: CE=_ . Calculate my risk premium p for this gamble p=

My von Neumann Morgenstern utility function is U (W) = 32 + (9/5)w1/2 for wealth w. I face a gamble that pays 1 with probability %, and 4 with probability %. Calculate my certainty equivalent for this gamble: CE=_ . Calculate my risk premium p for this gamble p=

Consider the utility function of an individual given by u(x) - ln(x - 10, 000). His total wealth is $270,000 of which S170,000 is the worth of his house. There is 10% probability that his house may be destroyed by fire. (a) What is the risk attitude of this person? (10%) (b) Calculate the insurance premium. fair premium and risk premium. (1596) (c) What is the relationship between the insurance premium, fair premium, and 2.

Consider the utility function of an individual given by u(x) - ln(x - 10, 000). His total wealth is $270,000 of which S170,000 is the worth of his house. There is 10% probability that his house may be destroyed by fire. (a) What is the risk attitude of this person? (10%) (b) Calculate the insurance premium. fair premium and risk premium. (1596) (c) What is the relationship between the insurance premium, fair premium, and 2.

Question 1 (20 marks) (a) A consumer maximizes utility and has Bernoulli utility function u(w)/2. The consumer has initial wealth w 1000 and faces two potential losses. With probability 0.1, the consumer loses S100, and with probability 0.2, the consumer loses $50. Assume that both losses cannot occur at the same time. What is the most this consumer would be willing to pay for full insurance against these losses? (10 marks) (b) A consumer has utility function u(z, y) In(x)...

Question 1 (20 marks) (a) A consumer maximizes utility and has Bernoulli utility function u(w)/2. The consumer has initial wealth w 1000 and faces two potential losses. With probability 0.1, the consumer loses S100, and with probability 0.2, the consumer loses $50. Assume that both losses cannot occur at the same time. What is the most this consumer would be willing to pay for full insurance against these losses? (10 marks) (b) A consumer has utility function u(z, y) In(x)...

Most questions answered within 3 hours.

-

According to a recent national Gallup Poll of U.S. smartphone

user, 35% upgrade their cell phone...

asked 28 seconds ago -

Suppose researchers perform a large-sample test of a population

proportion where the null hypothesis is that...

asked 38 seconds from now -

Jessica is single and has taxable income of $305,000 of which

$130,000 is attributable to her...

asked 3 minutes ago -

Can someone help me fill in the first part of this c++ code:

I need it...

asked 6 minutes ago -

A reaction vessel at 27 ∘C contains a mixture of SO2(P=3.10 atm

) and O2(P=1.00 atm...

asked 25 minutes ago -

A scientist randomly mutates the DNA of a bacterium. She then

sequences the bacterium’s daughter cells,...

asked 36 minutes ago -

2. Content theories attempt to explain work behaviors based on

__________.

a. the relationship between values...

asked 29 minutes ago -

Discuss the impact of technology on Medieval society and culture

and the impact of society and...

asked 26 minutes ago -

Assignment 3: Introduction & Environmental Analysis,

SWOT, Marketing Objectives (Goals) Marketing 4100

Directions

Total Point Value:...

asked 18 minutes ago -

Forecasts and actual sales of MP3 players at Just Say

Music are as follows:

Month

Forecast...

asked 19 minutes ago -

function predictKNN which computes the KNN prediction for given

input xi, K and train data.

A...

asked 30 minutes ago -

A 3.15-g bullet embeds itself in a 1.17-kg block, which is

attached to a spring of...

asked 45 minutes ago