Suppose 2 assets are jointly normally distributed with mean asset 1 = m1, mean asset 2...

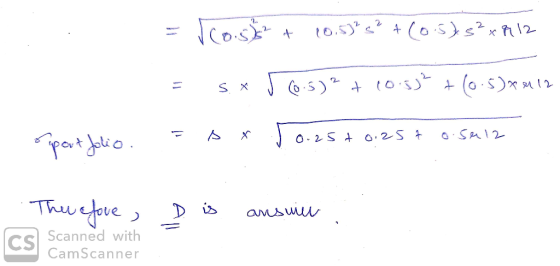

Suppose 2 assets are jointly normally distributed with mean asset 1 = m1, mean asset 2 = m2, standard deviation asset 1 = s, st. dev. asset 2 = s and correlation between asset 1 and 2 = r12. Note that the standard deviations of the two assets are the same. What is the portfolio standard deviation if we invest half of our wealth in asset 1 and half of our wealth in asset 2?

- A. .5*s^2+.5*s^2+2*r12*s^2

- B. .5*s+.5*s+ r12*s^2

- C. (.25+.25+r12)*s^2

- D. s*sqrt(.25+.25+.50*r12)

Homework Answers

Add Answer to:

Suppose 2 assets are jointly normally distributed with mean

asset 1 = m1, mean asset 2...

Consider the following two assets. Returns on asset 1 has a mean of ui and standard...

Consider the following two assets. Returns on asset 1 has a mean of ui and standard deviation of 01. Returns on asset 2 has a mean of j2 and standard deviation of 02. The correlation coefficient p1,2 measures how the two assets' returns are correlated, and it takes on values between -1 and +1. An investor puts W1 fraction of her wealth into stock 1, and W2 =1-W1 fraction of her wealth into stock 2. 1. Using the equation on...

Consider the following two assets. Returns on asset 1 has a mean of ui and standard deviation of 01. Returns on asset 2 has a mean of j2 and standard deviation of 02. The correlation coefficient p1,2 measures how the two assets' returns are correlated, and it takes on values between -1 and +1. An investor puts W1 fraction of her wealth into stock 1, and W2 =1-W1 fraction of her wealth into stock 2. 1. Using the equation on...

#1-4 Exit Suppose that car wash times are normally distributed with a mean of 25 minutes...

#1-4

Exit Suppose that car wash times are normally distributed with a mean of 25 minutes and a standard deviation of 3 minutes. You will be considering a group of 9 randomly selected car wash times. Answer the following questions. D 1. Given the information above, what can we say about the sampling distribution of x-bar. It is also normally distributed, because the original poplation was normally distributed. It is normally distributed because n is bigger than 30. We do...

#1-4

Exit Suppose that car wash times are normally distributed with a mean of 25 minutes and a standard deviation of 3 minutes. You will be considering a group of 9 randomly selected car wash times. Answer the following questions. D 1. Given the information above, what can we say about the sampling distribution of x-bar. It is also normally distributed, because the original poplation was normally distributed. It is normally distributed because n is bigger than 30. We do...

Consider the following two assets. Returns on asset l has a mean of μ i and...

Consider the following two assets. Returns on asset l has a mean of μ i and standard deviation of . Returns on asset 2 has a mean of μ2 and standard deviation of σ2. The correlation coefficient 2 measures how the two assets' returns are correlated, and it takes on values between-1 and +1. An investor puts Wi fraction of her wealth into stock 1, and W2 = 1-WI fraction of her wealth into stock 2. 1. Using the equation...

Consider the following two assets. Returns on asset l has a mean of μ i and standard deviation of . Returns on asset 2 has a mean of μ2 and standard deviation of σ2. The correlation coefficient 2 measures how the two assets' returns are correlated, and it takes on values between-1 and +1. An investor puts Wi fraction of her wealth into stock 1, and W2 = 1-WI fraction of her wealth into stock 2. 1. Using the equation...

10. (5pt) Suppose that X and Y are two normally distributed random variables. X has mean...

10. (5pt) Suppose that X and Y are two normally distributed random variables. X has mean 2 and standard deviation !5 Y has mean 5 and standard deviation 3. Their correlation is 0.6. What is the mean and standard deviation of X + Y? What is the distribution of X+ Y? What if X and Y are jointly normally distributed? What if they are not jointly normally distributed? Explain your answer.

10. (5pt) Suppose that X and Y are two normally distributed random variables. X has mean 2 and standard deviation !5 Y has mean 5 and standard deviation 3. Their correlation is 0.6. What is the mean and standard deviation of X + Y? What is the distribution of X+ Y? What if X and Y are jointly normally distributed? What if they are not jointly normally distributed? Explain your answer.

1. Let's assume you live in a world where there are only 2 risky assets, asset A and asset B. The...

1. Let's assume you live in a world where there are only 2 risky assets, asset A and asset B. There is also a risk free asset. You have the following information about the assets: Asset A 10% 5% Asset B 20% 25% Risk free (F) 5% 09% Expected Return Standard Deviation Let's assume the correlation between the returns of asset A and B is +1. Make a portfolio Pl that invests 50% in A and 50% in B. Calculate...

1. Let's assume you live in a world where there are only 2 risky assets, asset A and asset B. There is also a risk free asset. You have the following information about the assets: Asset A 10% 5% Asset B 20% 25% Risk free (F) 5% 09% Expected Return Standard Deviation Let's assume the correlation between the returns of asset A and B is +1. Make a portfolio Pl that invests 50% in A and 50% in B. Calculate...

There are only two risky assets (stocks) A and B in the market. Asset A: Mean...

There are only two risky assets (stocks) A and B in the market. Asset A: Mean = 20% Standard Deviation = 10% Asset B: Mean = 10% Standard Deviation = 5% Returns on Assets have zero correlation. A.Assume that there is no risk-free asset. (i)Plot (sketch) the efficiency frontier (the investment opportunity set). (ii)What is the expected return and the standard deviation of the minimum-variance-portfolio? (iii)An investor would like to construct a portfolio that has a standard deviation of 8%....

2. Consider an economy with 2 risky assets and one risk free asset. Two investors, A...

2. Consider an economy with 2 risky assets and one risk free asset. Two investors, A and B, have mean-variance utility functions (with different risk aversion coef- ficients). Let P denote investor A's optimal portfolio of risky and risk-free assets and let Q denote investor B's optimal portfolio of risky and risk-free assets. P and Q have expected returns and standard deviations given by P Q E[R] St. Dev. 0.2 0.45 0.1 0.25 (a) What is the risk-free interest rate...

2. Consider an economy with 2 risky assets and one risk free asset. Two investors, A and B, have mean-variance utility functions (with different risk aversion coef- ficients). Let P denote investor A's optimal portfolio of risky and risk-free assets and let Q denote investor B's optimal portfolio of risky and risk-free assets. P and Q have expected returns and standard deviations given by P Q E[R] St. Dev. 0.2 0.45 0.1 0.25 (a) What is the risk-free interest rate...

Consider the following data about the expected returns, standard deviations, and correlation between two assets: Asset...

Consider the following data about the expected returns, standard deviations, and correlation between two assets: Asset 1 Asset 2 Expected return 5.3% 6.8% Standard deviation 4.5% 7.8% Correlation coefficient -0.6 Calculate the expected return and standard deviation of a portfolio consisting of a 20% weight in asset 1 and an 80% weight in asset 2. What happens to the expected return and standard deviation of the portfolio when the weight combination changes to 50% in asset 1 and 50% in...

Question 1: Suppose there are two risky assets, A and B. You collect the following data...

Question 1: Suppose there are two risky assets, A and B. You collect the following data on probabilities of different states happening and the returns of the two risky assets in different states: State Probability Return Asset A Return Asset B State 10.3 7% 14% State 20.4 6% -4% State 30.3 -8% 8% The risk-free rate of return is 2%. (a) Calculate expected returns, variances, standard deviations, covariance, and correlation of returns of the two risky assets. (b) There are...

Question 1: Suppose there are two risky assets, A and B. You collect the following data on probabilities of different states happening and the returns of the two risky assets in different states: State Probability Return Asset A Return Asset B State 10.3 7% 14% State 20.4 6% -4% State 30.3 -8% 8% The risk-free rate of return is 2%. (a) Calculate expected returns, variances, standard deviations, covariance, and correlation of returns of the two risky assets. (b) There are...

Suppose there are three assets: A, B, and C. Asset A’s expected return and standard deviation are 1 percent and 1 percent. Asset B has the same expected return and standard deviation as Asset A. However, the correlation coefficient of Assets A and B is −0

Suppose there are three assets: A, B, and C. Asset A’s expected return and

standard deviation are 1 percent and 1 percent. Asset B has the same expected

return and standard deviation as Asset A. However, the correlation coefficient of

Assets A and B is −0.25. Asset C’s return is independent of the other two assets.

The expected return and standard deviation of Asset C are 0.5 percent and 1

percent.

(a) Find a portfolio of the three assets that...

Suppose there are three assets: A, B, and C. Asset A’s expected return and

standard deviation are 1 percent and 1 percent. Asset B has the same expected

return and standard deviation as Asset A. However, the correlation coefficient of

Assets A and B is −0.25. Asset C’s return is independent of the other two assets.

The expected return and standard deviation of Asset C are 0.5 percent and 1

percent.

(a) Find a portfolio of the three assets that...

Consider the following two assets. Returns on asset 1 has a mean of ui and standard deviation of 01. Returns on asset 2 has a mean of j2 and standard deviation of 02. The correlation coefficient p1,2 measures how the two assets' returns are correlated, and it takes on values between -1 and +1. An investor puts W1 fraction of her wealth into stock 1, and W2 =1-W1 fraction of her wealth into stock 2. 1. Using the equation on...

Consider the following two assets. Returns on asset 1 has a mean of ui and standard deviation of 01. Returns on asset 2 has a mean of j2 and standard deviation of 02. The correlation coefficient p1,2 measures how the two assets' returns are correlated, and it takes on values between -1 and +1. An investor puts W1 fraction of her wealth into stock 1, and W2 =1-W1 fraction of her wealth into stock 2. 1. Using the equation on...

#1-4

Exit Suppose that car wash times are normally distributed with a mean of 25 minutes and a standard deviation of 3 minutes. You will be considering a group of 9 randomly selected car wash times. Answer the following questions. D 1. Given the information above, what can we say about the sampling distribution of x-bar. It is also normally distributed, because the original poplation was normally distributed. It is normally distributed because n is bigger than 30. We do...

#1-4

Exit Suppose that car wash times are normally distributed with a mean of 25 minutes and a standard deviation of 3 minutes. You will be considering a group of 9 randomly selected car wash times. Answer the following questions. D 1. Given the information above, what can we say about the sampling distribution of x-bar. It is also normally distributed, because the original poplation was normally distributed. It is normally distributed because n is bigger than 30. We do...

Consider the following two assets. Returns on asset l has a mean of μ i and standard deviation of . Returns on asset 2 has a mean of μ2 and standard deviation of σ2. The correlation coefficient 2 measures how the two assets' returns are correlated, and it takes on values between-1 and +1. An investor puts Wi fraction of her wealth into stock 1, and W2 = 1-WI fraction of her wealth into stock 2. 1. Using the equation...

Consider the following two assets. Returns on asset l has a mean of μ i and standard deviation of . Returns on asset 2 has a mean of μ2 and standard deviation of σ2. The correlation coefficient 2 measures how the two assets' returns are correlated, and it takes on values between-1 and +1. An investor puts Wi fraction of her wealth into stock 1, and W2 = 1-WI fraction of her wealth into stock 2. 1. Using the equation...

10. (5pt) Suppose that X and Y are two normally distributed random variables. X has mean 2 and standard deviation !5 Y has mean 5 and standard deviation 3. Their correlation is 0.6. What is the mean and standard deviation of X + Y? What is the distribution of X+ Y? What if X and Y are jointly normally distributed? What if they are not jointly normally distributed? Explain your answer.

10. (5pt) Suppose that X and Y are two normally distributed random variables. X has mean 2 and standard deviation !5 Y has mean 5 and standard deviation 3. Their correlation is 0.6. What is the mean and standard deviation of X + Y? What is the distribution of X+ Y? What if X and Y are jointly normally distributed? What if they are not jointly normally distributed? Explain your answer.

1. Let's assume you live in a world where there are only 2 risky assets, asset A and asset B. There is also a risk free asset. You have the following information about the assets: Asset A 10% 5% Asset B 20% 25% Risk free (F) 5% 09% Expected Return Standard Deviation Let's assume the correlation between the returns of asset A and B is +1. Make a portfolio Pl that invests 50% in A and 50% in B. Calculate...

1. Let's assume you live in a world where there are only 2 risky assets, asset A and asset B. There is also a risk free asset. You have the following information about the assets: Asset A 10% 5% Asset B 20% 25% Risk free (F) 5% 09% Expected Return Standard Deviation Let's assume the correlation between the returns of asset A and B is +1. Make a portfolio Pl that invests 50% in A and 50% in B. Calculate...

2. Consider an economy with 2 risky assets and one risk free asset. Two investors, A and B, have mean-variance utility functions (with different risk aversion coef- ficients). Let P denote investor A's optimal portfolio of risky and risk-free assets and let Q denote investor B's optimal portfolio of risky and risk-free assets. P and Q have expected returns and standard deviations given by P Q E[R] St. Dev. 0.2 0.45 0.1 0.25 (a) What is the risk-free interest rate...

2. Consider an economy with 2 risky assets and one risk free asset. Two investors, A and B, have mean-variance utility functions (with different risk aversion coef- ficients). Let P denote investor A's optimal portfolio of risky and risk-free assets and let Q denote investor B's optimal portfolio of risky and risk-free assets. P and Q have expected returns and standard deviations given by P Q E[R] St. Dev. 0.2 0.45 0.1 0.25 (a) What is the risk-free interest rate...

Question 1: Suppose there are two risky assets, A and B. You collect the following data on probabilities of different states happening and the returns of the two risky assets in different states: State Probability Return Asset A Return Asset B State 10.3 7% 14% State 20.4 6% -4% State 30.3 -8% 8% The risk-free rate of return is 2%. (a) Calculate expected returns, variances, standard deviations, covariance, and correlation of returns of the two risky assets. (b) There are...

Question 1: Suppose there are two risky assets, A and B. You collect the following data on probabilities of different states happening and the returns of the two risky assets in different states: State Probability Return Asset A Return Asset B State 10.3 7% 14% State 20.4 6% -4% State 30.3 -8% 8% The risk-free rate of return is 2%. (a) Calculate expected returns, variances, standard deviations, covariance, and correlation of returns of the two risky assets. (b) There are...

Most questions answered within 3 hours.

-

) Raw materials are studied for contamination. Suppose that

the number of particles of contamination per...

asked 6 minutes ago -

After running a regression analysis we calculated an F test and

the significance level was 0.15....

asked 2 minutes ago -

----Can someone please help me solve this one using JAVA

----I thank you in advance

Create...

asked 7 minutes ago -

1. What force primarily attracts the potassium ion to

the nitrate ion?

a. London forces...

asked 8 minutes ago -

What are the negative effects of abruptly stopping the use of

all fossil fuels? Give at...

asked 15 minutes ago -

Given that many conflict are the result of different parties having

different interests, is it possible...

asked 20 minutes ago -

A 750 g block can slide uniformly along the horizontal track

when a string attached to...

asked 23 minutes ago -

In 2017, Juan entered into a contract to write a book. The

publisher advanced Juan $50,000,...

asked 37 minutes ago -

Determine the number of kinds of protons in each molecule (w/

respect to NMR spectroscopy). Drawing...

asked 47 minutes ago -

A jeweler whose near point is 68 cm from his eye uses a

magnifying glass as...

asked 45 minutes ago -

A company wants to determine how many units of each of two

products, A and B,...

asked 49 minutes ago -

The blood pressure of a person changes throughout the day.

Suppose the systolic blood pressure of...

asked 58 minutes ago