Homework Answers

Add Answer to:

I need help. I previously posted this question and the answer

was incorrect. Please if you...

Refer the table below on the average risk premium of the S&P 500 over T-bills and...

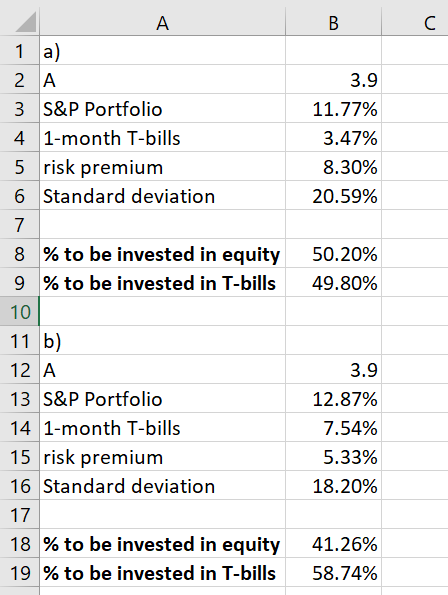

Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium. Suppose that the S&P 500 is your risky portfolio. Period 1926-2015 1992–2015 1970–1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1-Month Portfolio T-Bills 11.77 3.47 10.79 2.66 12.87 7.54 14.14 2.70 9.25 0.91 S&P 500 Portfolio Risk Standard Premium Deviation 8.30 20.59 8.13 18.29 5.33 18.20 11.44 17.67 8.33 27.99 Sharpe Ratio 0.40 0.44 0.29 0.65 0.30...

Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium. Suppose that the S&P 500 is your risky portfolio. Period 1926-2015 1992–2015 1970–1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1-Month Portfolio T-Bills 11.77 3.47 10.79 2.66 12.87 7.54 14.14 2.70 9.25 0.91 S&P 500 Portfolio Risk Standard Premium Deviation 8.30 20.59 8.13 18.29 5.33 18.20 11.44 17.67 8.33 27.99 Sharpe Ratio 0.40 0.44 0.29 0.65 0.30...

Refer the table below on the average risk premium of the S&P 500 over T-bills and...

Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium. Suppose that the S&P 500 is your risky portfolio Period 1926-2015 1992-2015 1970-1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1-Month Portfolio T-Bills 11.77 3.47 10.79 2.66 12.87 7.54 14.14 2.70 9.25 0.91 S&P 500 Portfolio Risk Standard Premium Deviation 8.30 20.59 8.13 18.29 5.33 18.20 11.44 17.67 8.33 27.99 Sharpe Ratio 0.40 0.44 0.29 0.65 0.30...

Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium. Suppose that the S&P 500 is your risky portfolio Period 1926-2015 1992-2015 1970-1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1-Month Portfolio T-Bills 11.77 3.47 10.79 2.66 12.87 7.54 14.14 2.70 9.25 0.91 S&P 500 Portfolio Risk Standard Premium Deviation 8.30 20.59 8.13 18.29 5.33 18.20 11.44 17.67 8.33 27.99 Sharpe Ratio 0.40 0.44 0.29 0.65 0.30...

Problem 6-20 Refer the table below on the average risk premium of the S&P 500 over...

Problem 6-20 Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium Suppose that the S&P 500 is your risky portfolio Sharpe Period 1926-2015 1992-2015 1970-1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1-Month Portfolio T-Bills T 11.77 3.47 110.79 2.66 12.87 14.14 2.70 9.25 8.91 Risk Premium 8.30 8.13 5.33 11.44 S&P 500 Portfolio Standard Deviation 20.59 18.29 18.20 17.67 27.99 0.40 0.44 0.29 0.3e o....

Problem 6-20 Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium Suppose that the S&P 500 is your risky portfolio Sharpe Period 1926-2015 1992-2015 1970-1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1-Month Portfolio T-Bills T 11.77 3.47 110.79 2.66 12.87 14.14 2.70 9.25 8.91 Risk Premium 8.30 8.13 5.33 11.44 S&P 500 Portfolio Standard Deviation 20.59 18.29 18.20 17.67 27.99 0.40 0.44 0.29 0.3e o....

Ch 5 #9: I already posted the question and half of the answer is wrong. Please...

Ch

5 #9: I already posted the question and half of the answer is

wrong. Please help.

You have $390,000 invested in a well-diversified portfolio. You inherit a house that is presently worth $250,000 Consider the summary measures in the following table: 4.16 points Investment Old portfolio House Expected Return 8% 19% Standard Deviation 15x 27% The correlation coeffcient between your portfolio and the house is 0.48 a. What is the expected return and the standard deviation for your portfolio...

Ch

5 #9: I already posted the question and half of the answer is

wrong. Please help.

You have $390,000 invested in a well-diversified portfolio. You inherit a house that is presently worth $250,000 Consider the summary measures in the following table: 4.16 points Investment Old portfolio House Expected Return 8% 19% Standard Deviation 15x 27% The correlation coeffcient between your portfolio and the house is 0.48 a. What is the expected return and the standard deviation for your portfolio...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE STEPS TAKEN TO ARRIVE...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE

STEPS TAKEN TO ARRIVE AT THE ANSWER. THANK YOU!

Check my work Greta, an elderly investor, has a degree of risk aversion of A= 3 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of 3-year strategies. (All rates are annual, continuously compounded.) The S&P 500 risk premium is estimated...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE

STEPS TAKEN TO ARRIVE AT THE ANSWER. THANK YOU!

Check my work Greta, an elderly investor, has a degree of risk aversion of A= 3 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of 3-year strategies. (All rates are annual, continuously compounded.) The S&P 500 risk premium is estimated...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE STEPS TAKEN TO ARRIVE...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE

STEPS TAKEN TO ARRIVE AT THE ANSWER. THANK YOU!

Check my work Greta, an elderly investor, has a degree of risk aversion of A = 3 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of one-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE

STEPS TAKEN TO ARRIVE AT THE ANSWER. THANK YOU!

Check my work Greta, an elderly investor, has a degree of risk aversion of A = 3 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of one-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium...

PLEASE PROVIDE THE STEPS TO SOLVE THE PROBLEM. THANK YOU SO MUCH! Check my work Greta,...

PLEASE PROVIDE THE STEPS TO SOLVE THE PROBLEM. THANK YOU SO

MUCH!

Check my work Greta, an elderly investor, has a degree of risk aversion of A= 5 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of 1-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium is estimated at 6% per year, with a SD of...

PLEASE PROVIDE THE STEPS TO SOLVE THE PROBLEM. THANK YOU SO

MUCH!

Check my work Greta, an elderly investor, has a degree of risk aversion of A= 5 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of 1-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium is estimated at 6% per year, with a SD of...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE STEPS TAKEN TO ARRIVE...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE

STEPS TAKEN TO ARRIVE AT THE ANSWER. THANK YOU!

Check my work Greta, an elderly investor, has a degree of risk aversion of A= 4 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of one-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium is...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE

STEPS TAKEN TO ARRIVE AT THE ANSWER. THANK YOU!

Check my work Greta, an elderly investor, has a degree of risk aversion of A= 4 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of one-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium is...

QUESTION 10 5 points Use the following information to answer the next two questions. Assume the...

QUESTION 10 5 points Use the following information to answer the next two questions. Assume the return on the S&P 500 Index is 20%, while its standard deviation is 15%. Treasury bills yield a 5% rate of retum. You'd like to create a portfolio consisting of the S&P 500 Index and t-bills. You want the standard deviation of your portfolio to be 18%. Find the return of your portfolio according to the CML. Round intermediate steps to four decimals. 25...

QUESTION 10 5 points Use the following information to answer the next two questions. Assume the return on the S&P 500 Index is 20%, while its standard deviation is 15%. Treasury bills yield a 5% rate of retum. You'd like to create a portfolio consisting of the S&P 500 Index and t-bills. You want the standard deviation of your portfolio to be 18%. Find the return of your portfolio according to the CML. Round intermediate steps to four decimals. 25...

Need help with b1 and b2 please explain with details.Thx Consider the following table for a...

Need help with b1 and b2 please explain with details.Thx

Consider the following table for a period of six years: Returns Large- Company Stocks U.S Treasury Bills Year 1 -15.29% 7.41% 2 -26.65 8.05 3 37.35 24.05 5.99 4 5.67 5 7.40 5.51 6 6.69 7.82 a-1. Calculate the arithmetic average returns for large-company stocks and T-bills over this time period. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.)...

Need help with b1 and b2 please explain with details.Thx

Consider the following table for a period of six years: Returns Large- Company Stocks U.S Treasury Bills Year 1 -15.29% 7.41% 2 -26.65 8.05 3 37.35 24.05 5.99 4 5.67 5 7.40 5.51 6 6.69 7.82 a-1. Calculate the arithmetic average returns for large-company stocks and T-bills over this time period. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.)...

Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium. Suppose that the S&P 500 is your risky portfolio. Period 1926-2015 1992–2015 1970–1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1-Month Portfolio T-Bills 11.77 3.47 10.79 2.66 12.87 7.54 14.14 2.70 9.25 0.91 S&P 500 Portfolio Risk Standard Premium Deviation 8.30 20.59 8.13 18.29 5.33 18.20 11.44 17.67 8.33 27.99 Sharpe Ratio 0.40 0.44 0.29 0.65 0.30...

Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium. Suppose that the S&P 500 is your risky portfolio. Period 1926-2015 1992–2015 1970–1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1-Month Portfolio T-Bills 11.77 3.47 10.79 2.66 12.87 7.54 14.14 2.70 9.25 0.91 S&P 500 Portfolio Risk Standard Premium Deviation 8.30 20.59 8.13 18.29 5.33 18.20 11.44 17.67 8.33 27.99 Sharpe Ratio 0.40 0.44 0.29 0.65 0.30...

Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium. Suppose that the S&P 500 is your risky portfolio Period 1926-2015 1992-2015 1970-1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1-Month Portfolio T-Bills 11.77 3.47 10.79 2.66 12.87 7.54 14.14 2.70 9.25 0.91 S&P 500 Portfolio Risk Standard Premium Deviation 8.30 20.59 8.13 18.29 5.33 18.20 11.44 17.67 8.33 27.99 Sharpe Ratio 0.40 0.44 0.29 0.65 0.30...

Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium. Suppose that the S&P 500 is your risky portfolio Period 1926-2015 1992-2015 1970-1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1-Month Portfolio T-Bills 11.77 3.47 10.79 2.66 12.87 7.54 14.14 2.70 9.25 0.91 S&P 500 Portfolio Risk Standard Premium Deviation 8.30 20.59 8.13 18.29 5.33 18.20 11.44 17.67 8.33 27.99 Sharpe Ratio 0.40 0.44 0.29 0.65 0.30...

Problem 6-20 Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium Suppose that the S&P 500 is your risky portfolio Sharpe Period 1926-2015 1992-2015 1970-1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1-Month Portfolio T-Bills T 11.77 3.47 110.79 2.66 12.87 14.14 2.70 9.25 8.91 Risk Premium 8.30 8.13 5.33 11.44 S&P 500 Portfolio Standard Deviation 20.59 18.29 18.20 17.67 27.99 0.40 0.44 0.29 0.3e o....

Problem 6-20 Refer the table below on the average risk premium of the S&P 500 over T-bills and the standard deviation of that risk premium Suppose that the S&P 500 is your risky portfolio Sharpe Period 1926-2015 1992-2015 1970-1991 1948-1969 1926-1947 Average Annual Returns S&P 500 1-Month Portfolio T-Bills T 11.77 3.47 110.79 2.66 12.87 14.14 2.70 9.25 8.91 Risk Premium 8.30 8.13 5.33 11.44 S&P 500 Portfolio Standard Deviation 20.59 18.29 18.20 17.67 27.99 0.40 0.44 0.29 0.3e o....

Ch

5 #9: I already posted the question and half of the answer is

wrong. Please help.

You have $390,000 invested in a well-diversified portfolio. You inherit a house that is presently worth $250,000 Consider the summary measures in the following table: 4.16 points Investment Old portfolio House Expected Return 8% 19% Standard Deviation 15x 27% The correlation coeffcient between your portfolio and the house is 0.48 a. What is the expected return and the standard deviation for your portfolio...

Ch

5 #9: I already posted the question and half of the answer is

wrong. Please help.

You have $390,000 invested in a well-diversified portfolio. You inherit a house that is presently worth $250,000 Consider the summary measures in the following table: 4.16 points Investment Old portfolio House Expected Return 8% 19% Standard Deviation 15x 27% The correlation coeffcient between your portfolio and the house is 0.48 a. What is the expected return and the standard deviation for your portfolio...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE

STEPS TAKEN TO ARRIVE AT THE ANSWER. THANK YOU!

Check my work Greta, an elderly investor, has a degree of risk aversion of A= 3 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of 3-year strategies. (All rates are annual, continuously compounded.) The S&P 500 risk premium is estimated...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE

STEPS TAKEN TO ARRIVE AT THE ANSWER. THANK YOU!

Check my work Greta, an elderly investor, has a degree of risk aversion of A= 3 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of 3-year strategies. (All rates are annual, continuously compounded.) The S&P 500 risk premium is estimated...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE

STEPS TAKEN TO ARRIVE AT THE ANSWER. THANK YOU!

Check my work Greta, an elderly investor, has a degree of risk aversion of A = 3 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of one-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE

STEPS TAKEN TO ARRIVE AT THE ANSWER. THANK YOU!

Check my work Greta, an elderly investor, has a degree of risk aversion of A = 3 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of one-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium...

PLEASE PROVIDE THE STEPS TO SOLVE THE PROBLEM. THANK YOU SO

MUCH!

Check my work Greta, an elderly investor, has a degree of risk aversion of A= 5 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of 1-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium is estimated at 6% per year, with a SD of...

PLEASE PROVIDE THE STEPS TO SOLVE THE PROBLEM. THANK YOU SO

MUCH!

Check my work Greta, an elderly investor, has a degree of risk aversion of A= 5 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of 1-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium is estimated at 6% per year, with a SD of...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE

STEPS TAKEN TO ARRIVE AT THE ANSWER. THANK YOU!

Check my work Greta, an elderly investor, has a degree of risk aversion of A= 4 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of one-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium is...

PLEASE SHOW HOW YOU SOLVE THE EQUATION--I WOULD LIKE TO SEE THE

STEPS TAKEN TO ARRIVE AT THE ANSWER. THANK YOU!

Check my work Greta, an elderly investor, has a degree of risk aversion of A= 4 when applied to return on wealth over a one-year horizon. She is pondering two portfolios, the S&P 500 and a hedge fund, as well as a number of one-year strategies. (All rates are annual and continuously compounded.) The S&P 500 risk premium is...

QUESTION 10 5 points Use the following information to answer the next two questions. Assume the return on the S&P 500 Index is 20%, while its standard deviation is 15%. Treasury bills yield a 5% rate of retum. You'd like to create a portfolio consisting of the S&P 500 Index and t-bills. You want the standard deviation of your portfolio to be 18%. Find the return of your portfolio according to the CML. Round intermediate steps to four decimals. 25...

QUESTION 10 5 points Use the following information to answer the next two questions. Assume the return on the S&P 500 Index is 20%, while its standard deviation is 15%. Treasury bills yield a 5% rate of retum. You'd like to create a portfolio consisting of the S&P 500 Index and t-bills. You want the standard deviation of your portfolio to be 18%. Find the return of your portfolio according to the CML. Round intermediate steps to four decimals. 25...

Need help with b1 and b2 please explain with details.Thx

Consider the following table for a period of six years: Returns Large- Company Stocks U.S Treasury Bills Year 1 -15.29% 7.41% 2 -26.65 8.05 3 37.35 24.05 5.99 4 5.67 5 7.40 5.51 6 6.69 7.82 a-1. Calculate the arithmetic average returns for large-company stocks and T-bills over this time period. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.)...

Need help with b1 and b2 please explain with details.Thx

Consider the following table for a period of six years: Returns Large- Company Stocks U.S Treasury Bills Year 1 -15.29% 7.41% 2 -26.65 8.05 3 37.35 24.05 5.99 4 5.67 5 7.40 5.51 6 6.69 7.82 a-1. Calculate the arithmetic average returns for large-company stocks and T-bills over this time period. (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.)...

Most questions answered within 3 hours.

-

You have a yeast cell culture with a concentration of 5x10^4

cells/ml. If you dilute this...

asked 1 minute from now -

In which direction the Reaction goes? Show detailed process.

SeO3 + 2ClO2. + 2H3O <---> Se...

asked 12 minutes ago -

Unexposed silver halides are removed from photographic film when

they react with sodium thiosulfate

(Na2S2O3, called...

asked 12 minutes ago -

A 0.3054 gram sample of the mineral chalcopyrite (CuFeS2)

yielded 0.6525 gram BaSO4 precipitate. What is...

asked 12 minutes ago -

An short-seller in Tesla is worried the latest management

earnings forecast is too aggressive and the...

asked 59 minutes ago -

Question 3 (1 point)

Fill in the blank. Speed Car Rental company found that the tire...

asked 58 minutes ago -

1. A copper wire is 26.61 cm long and weighs 1.265 g. The

density of copper...

asked 36 minutes ago -

Remember that a concept sketch consists of a sketch (or

series of sketches), labels, and complete...

asked 38 minutes ago -

on a newly discovered planet, the period of a pendulum with a

length of 2 m...

asked 40 minutes ago -

Why [M(CN)6] is not organometallic even it has metal

to carbon bond too

asked 47 minutes ago -

mstar electric has a bond issue outstanding that has a 20 year

life, a $1,000 par...

asked 54 minutes ago -

This is a Business Writing Question:

Common Types of Faulty Sentence Logic:

A. Mixed constructions

B....

asked 55 minutes ago